This week, our In Focus section highlights HMA Medicaid Market Solutions (MMS) which is supporting state flexibility in designing and implementing initiatives, including Section 1115 Demonstration Waivers, promoting member engagement, and personal responsibility. Over the coming weeks, HMA MMS will present a series of articles providing an in-depth look at the facets of these new Medicaid models.

A foundational principal when implementing Medicaid expansion programs emphasizing personal responsibility is that the adults eligible for the Medicaid expansion are unique from those traditionally covered by Medicaid. Traditional Medicaid populations would include the aged, disabled, children, and pregnant women, these individuals may have specific medical needs including long term care that states currently address through the Medicaid benefit package. The adult population covered by Medicaid expansions includes adults aged 19-64 that have income up to 133% of the poverty level, who do not qualify for other Medicaid programs. A portion of this group, those with income between 100% and 133% FPL, are eligible for the commercial essential health benefits available in the Marketplace in the absence of a Medicaid expansion or may have access to employer sponsored insurance. This fundamental difference the availability of commercial coverage and the fact that individuals in this group do not qualify for Medicaid on other basis based medical need may lead a state to provide those eligible for the Medicaid expansion with benefits that differ from the standard Medicaid State Plan and instead align with the commercial essential health benefits options. The benefits offered to the expansion population are required to be provided through an Alternative Benefit Plan (ABP). States may make these benefits the same as Medicaid State Plan benefits or may choose to base them on a different set of benefits. ABPs were an option for states prior to the Affordable Care Act and were updated following its passage to reference the Essential Health Benefits (EHB) options that are available to states in the commercial market while maintaining the exemption for the medically frail. [1]

To date, 34 states, including D.C., have elected to offer Medicaid to childless adults with income under 138% of the poverty level.[2] Among these states, 14 have implemented or are in the process of implementing the option to base the benefits for the expansion population on a package other than the Medicaid State Plan.[3] When one or more ABPs that differ from the Medicaid State Plan is implemented, Medicaid officials must develop a process to determine who meets the criteria of medically frail. The medically frail must be provided with the appropriate enrollment options as this group may enroll in the ABP but must also have the choice of the State Plan benefit package.

Unlike other personal responsibility initiatives targeted at the expansion population, ABPs can be leveraged without the implementation of a Section 1115 waiver. Therefore, states have the option to develop a separate benefit package or packages targeted to the adult expansion population without taking on the additional requirements of a waiver. In addition, the recently finalized (April 17, 2018) Notice of Benefit and Payment Parameters for 2019[4] should allow states additional flexibility in selecting EHB benchmarks beginning in 2020. This flexibility should carry over to ABPs, providing more options on which states can base their Medicaid expansion coverage.

Current ABP Options

States developing benefit packages targeted to Medicaid expansion adults have the option to develop a benchmark or benchmark equivalent coverage ABP. A benchmark plan is a benefit design that is indexed to the benefits offered on a reference plan, and a benchmark equivalent plan is a benefit design that provides benefits of equivalent value to a reference plan. Many of the requirements for ABPs are linked to the commercial market definition of EHB. Benchmark coverage must offer benefits in the ten EHB categories[5] and offer benefits of equal value to those in the benchmark plan. “Equal to” does not indicate that the same benefits must be offered, as benefits may be removed or substituted within an EHB category following the methodology for benefit substitution leveraged in the commercial market. Plans that can serve as the base-benchmark include all of those plans available to serve as commercial market EHBs.[6]

The benchmarking process for ABPs contains more flexibility than allowed for the definition of a state’s EHB in the commercial market. Within the ten required benefit categories, benefits may be removed, replaced, modified, and substituted, provided that the entire actuarial value of the category does not fall below the original value in the reference plan. For example, if a benchmark plan offers a benefit not available in a Medicaid State Plan, this benefit can be removed, and an additional benefit may be augmented with a benefit of equal or greater value and the plan can still serve as the reference plan for the ABP. Any EHB category may be duplicated from the Medicaid State Plan, provided it is of at least the same value, while continuing to base the remaining EHB categories based on the selected benchmark plan. In addition, benefits may be added to the ABP that are not included in the benchmark option, without the requirements that the cost of the benefit be defrayed as exists in the commercial market.

States may also leverage benchmark equivalent coverage when targeting benefits that require more flexibility than allowed under the benchmark process. Benchmark equivalent coverage requires the same coverage of the ten EHB categories but allows for a package that is on aggregate of equal value to one of the benchmark options instead of equal value in every category. Prescription drugs, mental health, vision and hearing services must be provided at least at 75 percent of the actuarial value of the benchmark plan. However, provided the total value of the plan is at least equal to the reference plan, there are no such restrictions on variation in the other categories under the benchmark equivalent option.

Today there exists between these two options substantial ability for states to tailor a benefit package specific to the expansion population. In addition, while the expansion population is the only eligibility group mandated to enroll in an ABP, the ability to be flexible in benefit designs and target other optional populations remains an option to serve state goals of offering unique or innovative benefit designs. Further, leveraging ABPs via managed care can alleviate the burden of operating multiple benefit packages via fee-for-service. Where distinct benefit designs may benefit targeted populations, ABPs continue to exist as a powerful policy tool.

Future ABP Options

The Notice of Benefit and Payment Parameters for 2019 adds benchmark options for states to leverage from the commercial market in 2020. As the ABP benchmark plan options are based on those plans available in the commercial market, this should allow for additional flexibility for states in defining benefit packages via ABPs beginning in 2020. The requirement to offer all 10 EHB benefit categories and the existing benchmark options remain. Additional benchmark plan options include:

- The EHB benchmark plan for 2017 from any state

- Any of the existing benchmarks, with any EHB category replaced by a benchmark plan from another state

- Otherwise selecting or developing a benchmark, provided it is equivalent to a typical employer plan.[7]

This increased flexibility will allow for further targeting and development of innovative benefit designs in Medicaid.

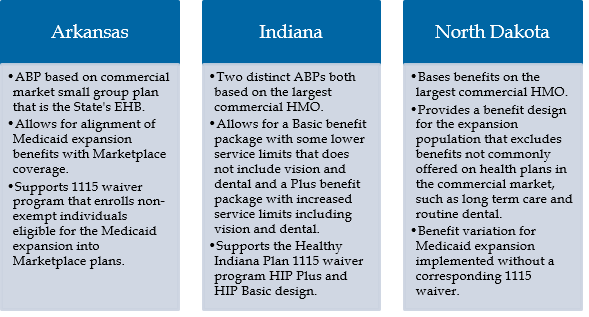

State Examples of Benefit Variation via ABPs

Identifying and Enrolling the Medically Frail

States leveraging ABPs to offer the Medicaid Expansion population a benefit package distinct from the Medicaid State Plan must also identify the medically frail and offer these individuals the opportunity to select the Medicaid State Plan instead of the ABP offered to the remaining expansion population.[8] The opt-out process is not required where, as is the case of Indiana, the Medicaid State Plan offers coverage equal to or greater than the ABP option in every benefit. However, even in these instances, identifying the medically frail and enrolling these individuals into an ABP equal to the Medicaid State Plan benefits remains a requirement. In states where the ABP is the state plan, the medically frail identification and opt-out process is not required; however, recently medically frail has been distinguished as a distinct population exempt from community engagement requirements, requiring these states to develop identification processes for community engagement even where there is not a benefit difference.

The federal definition of medically frail as applicable to the Medicaid Expansion population includes:

- individuals with disabling mental disorders

- individuals with chronic substance use disorders

- individuals with serious and complex medical conditions;

- individuals with a physical, intellectual or developmental disability that significantly impairs their ability to perform one or more activities of daily living, and

- individuals with a disability determination based on Social Security criteria or in states that apply more restrictive criteria than the Supplemental Security Income program, the state plan criteria.

Within these criteria states have substantial flexibility in how they define the medically frail and what process they leverage to identify them. Conditions or circumstances in addition to the requirements in federal rule may be added to the state definition, for example, individuals that are chronically homeless will be considered medically frail in Kentucky. The state specific definition of medically frail and the process to identify these individuals must be documented in the ABP.

State definitions of medically frail may be based on diagnosis codes, past health care utilization, or general member medical need. Once medically frail is defined, the state must develop a method to identify medically frail individuals. This may include member screening tools or surveys, provider attestations and/or documentation, or tools that perform claims analysis to identify individuals that meet the state’s criteria.

For individuals determined to be medically frail, these individuals may be enrolled by default into the Medicaid State Plan option and then provided, if required, the opportunity to change to the ABP option. Providing the opportunity to change coverage options requires that the state inform the enrollee of the difference in benefits between the two options.

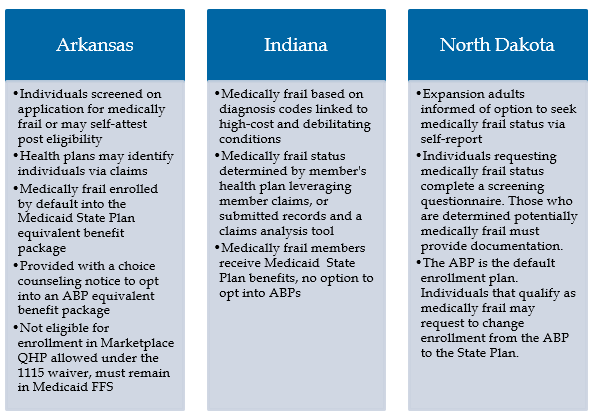

Example of State Variations in Medically Frail Processes

Outlook for ABPs

Leveraging the options to target benefit design, specifically to the Medicaid expansion population, provides the ability to develop benefits appropriate to the needs of the target population. Analyzing the benchmark plan options to select the most appropriate benefit starting point, and developing medically frail definitions and methodology are key considerations when implementing targeted benefits for the Medicaid expansion. In addition, where benefits vary between populations, ensuring transparency for members, providers and other stakeholders regarding what benefits are covered is a critical factor to success.

[1] 42 CFR 440.315(f)

[2] Virginia has a state approved Medicaid Expansion as of 5-30-2018 but has not yet implemented.

[3] State Differences in Application of Medically Fragility Under the Affordable Care Act. https://escholarship.umassmed.edu/cgi/viewcontent.cgi?article=1028&context=commed_pubs & Medicaid Expansion: Comparing State Choices in Alternative Benefit Plan Design. State Health Access Data Center. http://www.shadac.org/sites/default/files/Old_files/shadac/publications/Planalp_SHRP_IG_2015.pdf

[4] 2019 Notice of Benefit and Payment Parameters. https://www.gpo.gov/fdsys/pkg/FR-2018-04-17/pdf/2018-07355.pdf

[5] Includes: ambulatory patient services (outpatient services), emergency services, hospitalization (inpatient), maternity and newborn care, mental health and substance use disorder services, including behavioral health treatment, prescription drugs, rehabilitative and habilitative services (those that help patients acquire, maintain, or improve skills necessary for daily functioning) and devices, laboratory services, preventive and wellness services and chronic disease management, pediatric services, including oral and vision care. Note: For the purposes of offering benefits to the adult population in Medicaid, Early Periodic Screening Diagnostic, and Treatment services do not apply as these are a required pediatric benefit.

[6] Includes: Federal Employee Coverage (Blue Cross Blue Shield PPO), State Employee Coverage, Largest Commercial Non-Medicaid HMO by enrollment in the State, Secretary Approved Coverage (Medicaid State Plan AND All of the options available in the state for the commercial market EHB. Encompassing the three small group insurance plans by enrollment in the state).

[7] Defined as equal to one of the existing benchmark options, one of the five largest benchmarks by enrollment for large group health insurer plans.

[8] Since enrollment of the newly eligible adult or Medicaid expansion population is required to be into ABPs, CMS refers to the Medicaid State Plan option as ‘the ABP that is the state plan’ for medically frail individuals.