This week, our In Focus section reviews highlights and shares key takeaways from the 22nd annual Medicaid Budget Survey conducted by The Kaiser Family Foundation (KFF) and Health Management Associates (HMA). Survey results were released on October 25, 2022, in two new reports: How the Pandemic Continues to Shape Medicaid Priorities: Results from an Annual Medicaid Budget Survey for State Fiscal Years 2022 and 2023 and Medicaid Enrollment & Spending Growth: FY 2022 & 2023. The report was prepared by Elizabeth Hinton, Madeline Guth, Jada Raphael, Sweta Haldar, and Robin Rudowitz from the Kaiser Family Foundation and by Kathleen Gifford, Aimee Lashbrook, and Matt Wimmer from HMA; and Mike Nardone. The survey was conducted in collaboration with the National Association of Medicaid Directors (NAMD).

This survey reports on policies in place or planned for FY 2022 and FY 2023, including state experiences with policies adopted in response to the COVID-19 pandemic. The conclusions are based on information provided by the nation’s state Medicaid Directors.

Key Report Highlights

In the following sections, we highlight a few of the major findings from the reports. This is a fraction of what is covered in the 50-state survey reports, which include significant detail and findings on policy changes and initiatives related to delivery systems, health equity, benefits, telehealth, provider rates and taxes, and pharmacy. The reports also look at the opportunities, challenges, and priorities facing Medicaid programs.

Medicaid Enrollment and Spending Growth

The COVID-19 pandemic created significant implications for Medicaid. During this time, Medicaid enrollment has reached record highs due to the Families First Coronavirus Response Act (FFCRA), enacted in March 2020, which authorized a 6.2 percentage point increase in the federal match rate, or Federal Medical Assistance Percentage (FMAP), retroactive to January 1, 2020, and until the Public Health Emergency (PHE) ends. The increase was available to states that meet certain “maintenance of eligibility” (MOE) requirements. Since the survey, the PHE was extended to mid-January 2023, somewhat delaying the anticipated effects described in survey.

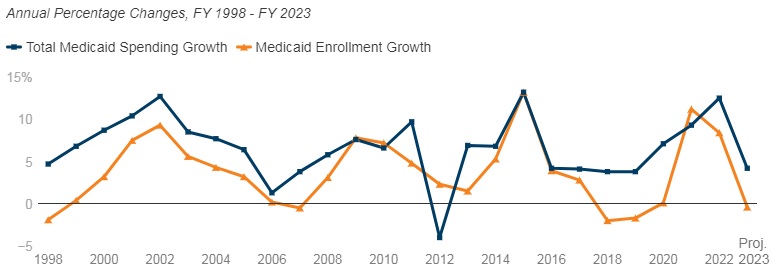

Medicaid enrollment growth slowed to 8.4 percent in FY 2022, after a sharp increase in FY 2021 (11.2 percent). Almost all responding states reported that the MOE continuous enrollment requirement was the most significant factor driving FY 2022 enrollment growth. Responding states expect Medicaid enrollment growth to decline (-0.4 percent) in FY 2023, based largely on the assumption that the PHE and the related MOE requirements would end by mid-FY 2023. States anticipate larger declines as Medicaid redeterminations and renewals resume.

In FY 2022, total Medicaid spending is expected to reach a peak growth of 12.5 percent, with enrollment growth as the primary driver. For FY 2023, total spending growth is expected to slow to 4.2 percent, assuming slower enrollment growth after the unwinding of the PHE. State Medicaid spending grew by 9.9 percent in FY 2022 and is projected to increase by 16.3 percent in FY 2023 once enhanced federal fiscal relief expires. If the PHE is extended, state spending increases and enrollment decreases that states anticipated for FY 2023 could occur later.

Figure 1 – Percent Change in Medicaid Spending and Enrollment, FY 1998-23

SOURCE: FY 2022-2023 spending data and FY 2023 enrollment data are derived from the KFF survey of Medicaid officials in 50 states and DC conducted by Health Management Associates, October 2022. 49 states submitted survey responses by Oct. 2022; state response rates varied across questions. Historic data reflects growth across all 50 states and DC and comes from various sources.

Delivery Systems

- Capitated managed care remains the predominant delivery system for Medicaid in most states. Forty-six states operated some form of Medicaid managed care (managed care organizations (MCOs) and/or primary care case management (PCCM)). Forty-one states contracted with risk-based MCOs. Of these, only Colorado and Nevada did not offer MCOs statewide. Only five states – Alaska, Connecticut, Maine, Vermont, and Wyoming – lacked a comprehensive Medicaid managed care model.

- Thirty-four states, including Distrct of Columbia, operate MCOs only, five states operate PCCM programs only, and seven states operate both MCOs and a PCCM program.

- Twenty-seven states contracted with one or more PHPs to provide Medicaid benefits, including behavioral health care, dental care, vision care, non-emergency medical transportation (NEMT), and long-term services and supports (LTSS).

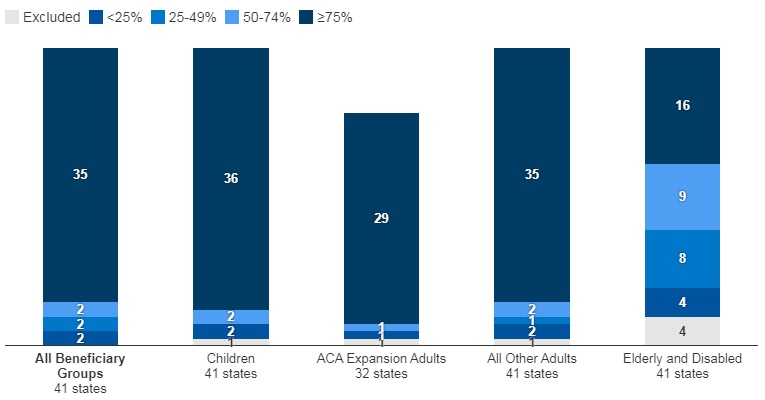

- Of the forty-one states that contracted with MCOs, 35 reported that 75 percent or more of their Medicaid beneficiaries were enrolled in MCOs as of July 1, 2022.

Figure 2 – MCO Managed Care Penetration Rates for Select Groups of Medicaid Beneficiaries as of July 1, 2022

SOURCE: KFF survey of Medicaid officials in 50 states and DC conducted by HMA, October 2022.

Medicaid Managed Care and Delivery System Changes

- California, Missouri, Nevada, New Jersey, and New York reported expanding mandatory MCO enrollment for targeted populations.

- Missouri and Ohio reported introducing specialized managed care programs for children with complex needs.

- California, Nevada, and Tennessee indicated that they were carving in certain long-term services and supports (LTSS) into their managed care programs.

- California and Ohio reported carving out pharmacy services in FY 2022 or FY 2023, respectively. The District of Columbia carved out emergency medical transportation from its MCO contracts in FY 2022.

- Maine, North Carolina, Oregon, and Washington reported changes to their PCCM programs.

- Virginia plans to implement Cardinal Care in FY 2023, merging the state’s two existing managed care programs: Medallion 4.0 (serving children, pregnant individuals, and adults) and Commonwealth Coordinated Care Plus (CCC Plus) (serving seniors, children and adults with disabilities, and individuals who require LTSS).

- Forty-one states reported at least one specified delivery system and payment reform initiative (e.g. Patient-Centered Medical Home (PCMH), ACA Health Homes, Accountable Care Organization (ACO), Episode of Care Initiatives, All-Payer Claims Database (APCD)).

Health Equity

- Twenty-five states reported using at least one specified strategy to improve race, ethnicity, and language (REL) data completeness. Of the 45 responding states, 16 states reported requiring MCOs and other applicable contractors to collect REL data, 12 states reported that eligibility, renewal materials, and/or applications explain how REL data will be used and/or why reporting these data are important, nine states reported linking Medicaid enrollment data with public health department vital records data, and eight states reported partnering with one or more health information exchanges (HIEs) to obtain additional REL data for Medicaid enrollees.

- Twelve of 44 responding states reported at least one financial incentive tied to health equity in place in FY 2022. The vast majority of these incentives were in place in managed care arrangements (11 of 13). Within managed care arrangements, states most commonly reported linking or planning to link capitation withholds, pay for performance incentives, and/or state-directed provider payments to health equity-related quality measures. Only two states (Connecticut and Minnesota), reported a FFS financial incentive in FY 2022. Five additional states report plans to implement financial incentives linked to health equity in FY 2023.

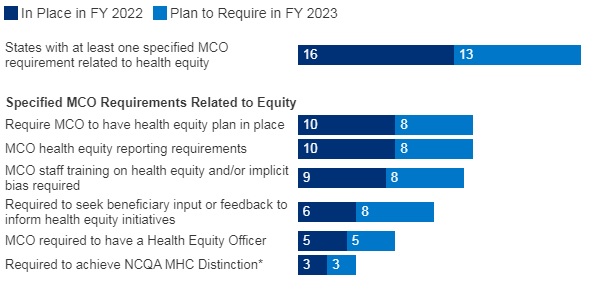

- Sixteen of 37 responding MCO states reported at least one specified health equity MCO requirement in place in FY 2022. The number of MCO states with at least one specified health equity MCO requirement in place is expected to grow significantly in FY 2023, from 16 to 25 states. Examples of MCO requirements to address health equity include having a health equity plan, designating a Health Equity Officer, and staff training on health equity and/or implicit bias.

Figure 3 – MCO Requirements to Address Health Equity, FYs 2022-23

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; n=37 states.

Benefits

- Thirty-three states reported new or enhanced benefits in FY 2022 and 34 states are adding or enhancing benefits in FY 2023. Two states reported benefit cuts or limitations in FY 2022 and no states reported cuts or limitations in FY 2023.

Figure 4 – Select Categories of Benefit Enhancements or Additions, FYs 2022-23

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; Arkansas and Georgia did not respond.

- Behavioral Health Services. States reported service expansions across the behavioral health care continuum, including institutional, intensive, outpatient, home and community-based, and crisis services. States reported addressing SUD outcomes, including coverage of opioid treatment programs, peer supports, and enhanced care management. At least ten states are expanding coverage of crisis services, which aim to connect Medicaid enrollees experiencing behavioral health crises to appropriate community-based care, including mobile crisis response services and crisis stabilization centers.

- Pregnancy and Postpartum Services. In April 2022, a temporary option under ARPA to extend Medicaid postpartum coverage from 60 days to 12 months took effect. In addition to the states that took advantage of this eligibility change, some states are enhancing coverage of pregnancy and post-partum services. Nine states (California, District of Columbia, Illinois, Maryland, Michigan, New Mexico, Nevada, Rhode Island, and Virginia) are adding coverage of services provided by doulas and seven states (Alabama, Delaware, Illinois, Maryland, Ohio, Oregon, and Vermont) are investing in the implementation or expansion of home visiting programs.

- Preventive Services. Sixteen states reported expansions of preventive care in FY 2022 or FY 2023. For example, seven states are expanding services to prevent and/or manage diabetes, such as continuous glucose monitoring. Other reported preventive benefit enhancements relate to asthma services, vaccinations, and genetic testing and/or counseling.

- Services Targeting Social Determinants of Health. Many states reported new and expanded benefits targeting social determinants of health. Twelve states reported new or expanded housing-related supports, as well as other services and programs tailored for individuals experiencing homelessness or at risk of being homeless.

- Dental Services. Nine states are adding comprehensive adult dental coverage, while additional states report expanding specific dental services for adults.

Telehealth

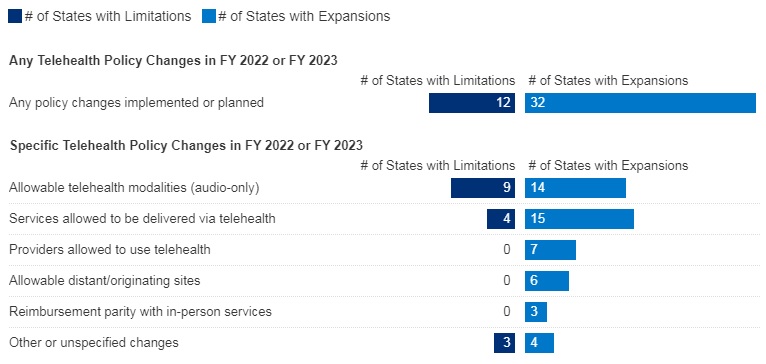

- Most states have or plan to adopt permanent Medicaid FFS telehealth expansions that will remain in place even after the pandemic, though some are considering guardrails on such policies. Nearly all responding states that contract MCOs reported that changes to FFS telehealth policies would also apply to MCOs.

Figure 5 – Changes to FFS Medicaid Telehealth Policy, FY 2022 or FY 2023

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; n=48 states.

- Nearly all responding states added or expanded audio-only telehealth coverage in Medicaid in response to the COVID-19 pandemic. Twenty-eight states reported that they newly added audio-only coverage while 19 states expanded existing coverage. Nearly all states reported audio-only coverage of mental health and substance use disorder (SUD) services. States least frequently reported audio-only coverage of home and community-based services (HCBS) and dental services. Two states (Mississippi and Wyoming) reported no coverage of audio-only telehealth for the services in question.

- Telehealth utilization by Medicaid enrollees has been high during the pandemic but has decreased and/or leveled off more recently. States noted that telehealth utilization trends over time correspond to COVID-19 outbreaks, with higher utilization during COVID-19 surges and lower utilization when case counts are lower. In general, states reported that telehealth utilization was projected to continue at higher levels than before the pandemic, at least for some service categories.

- Thirty-seven states (out of 47 responding) reported that behavioral health services were among those with the highest utilization. Additionally, a majority of states reported high utilization of evaluation and management (E/M) services and/or other physician/qualified health care professional office/outpatient services, including primary care.

- States reported ACA expansion adults as one of the groups most likely to use telehealth (about one-third of responding states), followed by children and individuals with disabilities (each identified by about one-sixth of responding states).

- Concerns regarding services delivered via telehealth included the quality of diagnoses, whether audio-only telehealth may be less effective, and inadequate access.

- Key issues that may influence future Medicaid telehealth policy decisions include analysis of data, state legislation and federal guidance, and cost concerns.

Provider Rates and Taxes

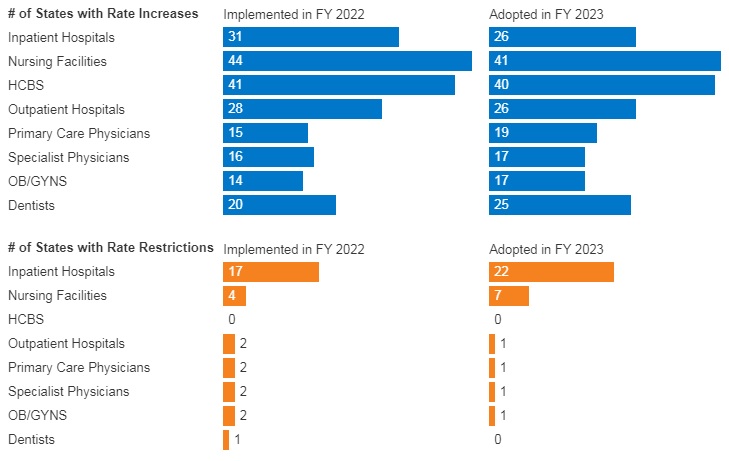

- In FY 2022, all 49 responding states reported implementing rate increases for at least one category of provider and 19 states reported implementing rate restrictions. In FY 2023, 48 states reported at least one planned rate increase and the number of states planning to restrict rates increased to 25 states.

- States reported rate increases for nursing facilities and home and community-based services (HCBS) providers more often than other provider categories. The survey also found an increased focus on dental rates with about half of reporting states (20 in FY 2022 and 25 in FY 2023) reporting implementing or plans to implement a dental rate increase

Figure 6 – FFS Provider Rate Changes Implemented in FY 2022 and Adopted for FY 2023

SOURCE: KFF survey of Medicaid officials in 50 states and DC conducted by HMA, October 2022.

- States continue to rely on provider taxes and fees to fund a portion of the non-federal share of Medicaid costs. All states but Alaska have at least one provider tax or fee in place. Thirty-eight states had three or more provider taxes in place in FY 2022 and eight other states had two provider taxes in place.

- The most common Medicaid provider taxes in place in FY 2022 were taxes on nursing facilities (46 states), followed by taxes on hospitals (44 states), intermediate care facilities for individuals with intellectual disabilities (33 states), and MCOs (18 states).

- Three states (Alabama, Mississippi, and Wyoming) reported plans to add new ambulance taxes in FY 2023.

Pharmacy

- Most states that contract with MCOs report that the pharmacy benefit is carved into managed care (34 out of 41 states that contract with MCOs). Six states (California, Missouri, North Dakota, Tennessee, Wisconsin, and West Virginia) report that pharmacy benefits are carved out of MCO contracts as of July 1, 2022. California was the latest to carve out pharmacy benefits as of January 1, 2022. Two states (New York and Ohio) report plans to carve out pharmacy from MCO contracts in state FY 2023 or later.

- In FY 2022, Kentucky began contracting with a single PBM for the managed care population. Louisiana and Mississippi report that they will require MCOs to contract with a single PBM designated by the state in FY 2023 and FY 2024, respectively.

- Seven states (Alabama, Arizona, Colorado, Massachusetts, Michigan, Oklahoma, and Washington) have value-based arrangements (VBAs) in place with one or more drug manufacturers.

- More than half of responding states reported newly implementing or expanding at least one initiative to contain prescription drug costs in FY 2022 or FY 2023.

- Six states (Florida, Kentucky, Massachusetts, Maryland, Nebraska, Nevada) reported recently implemented or planned policies to prohibit spread pricing or require pass through pricing in MCO contracts with PBMs.

Key Opportunities, Challenges, and Priorities in FY 2023 and Beyond

When asked to identify the top challenges for FY 2023 and beyond, Medicaid directors listed the following:

- The unwinding of PHE emergency measures and the resumption of redeterminations.

- Expiration of emergency authorities.

- Lasting focus on COVID-19, including vaccinations, long-COVID, decreased utilization of preventive care services, and future emergency preparedness.

Medicaid directors stated that future priorities shaped by COVID-19 include:

- Health equity.

- Specific populations and service categories, including behavioral health, long-term services and supports, and maternal and child health.

- Health care workforce challenges.

- Payment and delivery system initiatives and operations.

- IT system modernization.

- Social determinants of health.

Medicaid directors note that COVID-19 has presented both new opportunities and challenges and has also shifted and shaped ongoing Medicaid priorities.

Links to Kaiser/HMA 50-State Survey Reports