New guidance outlines how CMS intends to implement Chief Actuary certification and a fundamentally different approach to budget neutrality beginning January 1, 2027.

[HMA’s analysis on this and related Medicaid changes is ongoing; this blog reflects an initial understanding of the 6/11 SMDL; additional analysis is forthcoming.]

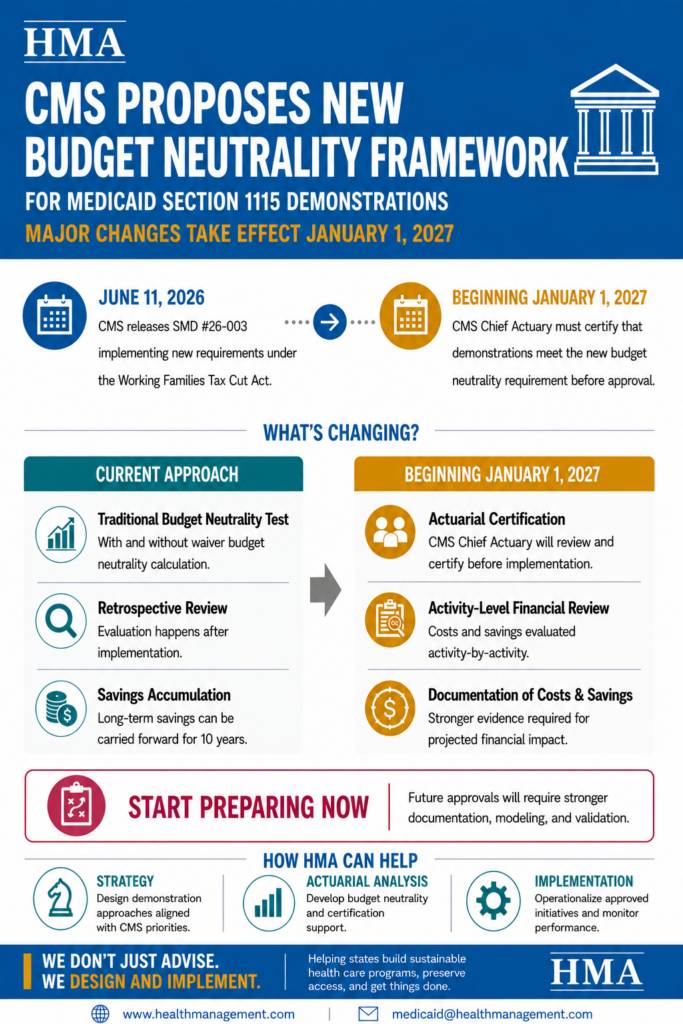

On June 11, 2026, the Centers for Medicare & Medicaid Services (CMS) released State Medicaid Director Letter (SMDL) #26-003, which provides long-anticipated guidance on how the agency intends to implement new statutory budget neutrality requirements for Medicaid section 1115 demonstrations beginning January 1, 2027.

The SMDL provides guidance on CMS’s implementation of provisions enacted in Public Law 119-21 (the One Big Beautiful Bill Act, or OBBBA), which CMS now refers to as the Working Families Tax Cut (WFTC) Act. The law requires the CMS Chief Actuary to certify that Medicaid section 1115 demonstrations will not increase federal Medicaid expenditures before CMS may approve new demonstrations, amendments, or renewals.

While the SMDL includes discussion of CMS’s preference that states rely on Medicaid state plan and other Title XIX authorities when available, the guidance primarily focuses on implementing the new budget neutrality requirements under section 1115(g).

The result is a proposed framework that could fundamentally change how states design, finance, evaluate, and renew section 1115 demonstrations.

Key Takeaway #1: Budget Neutrality framework is changing to become more accurate, detailed, and subject to enhanced review.

For decades, Medicaid Demonstrations under Section 1115 required budget neutrality calculations that relied on comparisons of projected with and without waiver expenditure. Retrospective assessments against established “without waiver” budget neutrality limits then occurred.

CMS now proposes a different model that includes enhancements to how the budget neutrality calculations are developed and reviewed. This will include an actuarial certification requirement that shows how the budget neutrality meets actuarially sound principles.

Beginning with applications, renewals, or amendments submitted after January 1, 2027, the following must occur:

- CMS’ Chief Actuary must certify that there will be no increase in federal expenditures compared to the expenditures projected in the absence of the Demonstration.

- A rigorous actuarial analysis of the projected financial impacts of individual demonstration activities must be performed. The budget neutrality analysis is certified by CMS’ Chief Actuary prior to Demonstration approval. This is a change from the historical “without waiver” expenditure cap calculation.

- With the review above, there is now no expenditure limit or budget neutrality cap. Instead, the budget neutrality is not approved if there is a projected increase in Federal Medicaid expenditures. (Note, approval of historical Demonstration applications and budget neutrality required a projection of reduced overall expenditures.)

- Monitoring budget neutrality in the Demonstration time period will utilize new special terms and conditions (STCs). There will be corrective actions implemented if expenditure substantially deviates from the State projections. Historically, quarterly and annual reporting was required, and States were subject to return to CMS any excess federal funds. The new guidance appears similar in that ongoing monitor will occur and action will be needed to the extent expenditures are not at or below projections.

For states to be compliant with this guidance, detailed actuarial analyses, methodology, assumptions, data, and documentation demonstrating the federal fiscal impact of each demonstration component will be necessary. States must provide sufficient information for CMS’s Chief Actuary to evaluate and certify budget neutrality, including the populations affected, covered services, payment methodologies, payment rates, administrative costs, and estimated federal expenditures associated with demonstration authorities.

Key Takeaway #2: Beginning January 1, 2027, certain benefits and services may be treated differently under Medicaid section 1115 demonstrations.

A central feature of the new framework is CMS’s proposed classification of demonstration activities into two categories.

The first category is Medicaid Authorizable Populations and Services (MAPS). These are populations and services that could otherwise be covered through the Medicaid state plan or another Title XIX authority. For budget neutrality purposes, CMS proposes treating MAPS expenditures as having a zero net financial impact because they represent expenditures that could have occurred absent the demonstration. This is similar to how current hypothetical expenditures are treated.

The second category consists of section 1115-only activities; that is, activities that could not otherwise be authorized through existing Medicaid authorities. These activities would become the primary focus of budget neutrality review.

States would be required to identify, measure, and document both the costs and savings associated with each section 1115-only activity, including administrative costs. CMS would then evaluate the aggregate financial impact of those activities when determining whether a demonstration qualifies for certification.

Key Takeaway #3: Medicaid 1115 demonstration savings will become more difficult to accumulate and carry forward.

CMS also proposes significant changes to the treatment of demonstration savings.

Historically, states have been able to accumulate budget neutrality savings and, under certain circumstances, carry those savings into future renewal periods. Many demonstrations have relied on these accumulated savings to support cost-not-otherwise-matchable expenditures and other demonstration initiatives.

Under the new approach, savings generally would be limited to those generated during the current demonstration period and could only be applied to the next immediate renewal period. CMS also proposes limiting rollover calculations to the most recent five years of demonstration experience and eliminating the longstanding ability to carry forward legacy savings across multiple renewal cycles.

CMS would provide a transition period for the first renewal after January 1, 2027, allowing states to use savings calculated under the current methodology. Over time, however, the proposed framework is expected to reduce the amount of demonstration savings available to states.

For states that have historically relied on demonstration savings as a key financing mechanism, these changes could require significant strategic and financial planning.

Key Takeaway #4: States and Medicaid-focused organizations should begin to identify alternative approaches, authorities, and partnerships to continue to advance the goals of certain 1115 demonstration initiatives.

One of the more closely watched aspects of the guidance involves CMS’s discussion of the relationship between section 1115 authority and other Medicaid authorities.

The final guidance stops short of directing states to systematically move authorities out of section 1115 demonstrations. Instead, CMS encourages states to reduce reliance on section 1115 authority when alternative Medicaid authorities are available, noting that doing so would strengthen oversight while reserving section 1115 authority for innovation and demonstration purposes. The agency specifically references Medicaid state plan authorities and other Title XIX authorities as potential alternatives where appropriate.

At the same time, CMS recognizes that, in certain circumstances, states may require concurrent section 1115 authority layered over other Medicaid authorities to achieve program goals and has indicated that it will provide technical assistance in those situations.

The interaction between this policy and the new MAPS framework may be particularly important. CMS provides examples showing that many authorities currently treated as hypothetical expenditures—including certain home- and community-based services (HCBS), managed care-related authorities, and other services that could be authorized elsewhere under Medicaid—would now be treated as MAPS activities for budget neutrality purposes.

For states, the immediate significance may be less about whether authorities remain within a section 1115 demonstration and more about how those authorities are treated under the new budget neutrality framework. As states assess the implications of the guidance, they may want to consider how various authorities are structured across section 1115 demonstrations, state plan authorities, and other Title XIX pathways. CMS’s discussion suggests that these decisions may increasingly be informed by both programmatic objectives and budget neutrality considerations.

Key Takeaway #5: States and Medicaid organizations can begin scenario planning and assessments now and monitor additional guidance and clarifications critical to operational issues.

Although CMS provides substantial detail regarding its intended direction, several important implementation questions remain unanswered. Among the issues states are likely to focus on over the coming months:

- How will CMS apply the new requirements to renewals that are already under review—or that are submitted before January 1, 2027—but remain pending after that date?

- How long will CMS’s Chief Actuary review take, and how should states adjust renewal and amendment timelines to account for the new certification process?

- How aggressively will CMS apply its stated preference for using state plan and other Title XIX authorities when alternative pathways exist?

- What level of documentation, modeling, and actuarial support will CMS ultimately require to support certification?

- How will CMS define acceptable methodologies and assumptions in the forthcoming rulemaking process?

CMS repeatedly notes that additional technical guidance, technical assistance, and formal rulemaking are forthcoming, suggesting that many operational details remain under development.

Key Takeaway #6: States should build additional time into future section 1115 renewal and amendment planning

Although significant details remain unresolved, the overall direction of federal policy is becoming clearer.

States with upcoming section 1115 renewals, amendments, or major demonstration redesign efforts should begin assessing which components of their demonstrations are likely to be classified as MAPS activities versus section 1115-only activities. They should also evaluate the extent to which future financing strategies depend on rollover savings or other elements of the current framework that may no longer be available after January 1, 2027.

In addition, states may want to assess whether certain demonstration authorities could be more appropriately administered through state plan, managed care, HCBS, or other Medicaid authorities, particularly given CMS’s stated preference for relying on alternative Title XIX pathways when available.

Most importantly, states should prepare for a future in which section 1115 approval decisions are increasingly driven by prospective actuarial analyses of the financial impact of individual demonstration activities that include detailed supporting documentation for CMS’s Chief Actuary to utilize for approval.

The forthcoming proposed rule will provide critical details; however, this guidance makes clear that CMS intends to reshape how section 1115 demonstrations are financed, evaluated, and renewed in the years ahead.

How HMA Can Help

HMA is actively helping states, health plans, providers, and other stakeholders assess the implications of CMS’s proposed budget neutrality framework and prepare for upcoming section 1115 renewals and amendments, as well as other changes due to recent guidance on community engagement requirements, state directed payments, and program integrity. Our experts bring deep experience in section 1115 demonstrations, Medicaid financing, budget neutrality modeling, actuarial analysis, managed care authorities, HCBS programs, waiver strategy, and federal negotiations.

As states evaluate the operational, financial, and policy implications of the new requirements, HMA can support strategic assessments, renewal planning, demonstration redesign, financial modeling, actuarial coordination, federal negotiations, and implementation planning. We are also tracking forthcoming rulemaking and additional CMS guidance that will further shape how section 1115(g) is implemented.

Be sure to register for our upcoming webinar, Understanding Work and Community Engagement Requirements and New Section 1115 Guidance, on July 15.