HMA Insights: Your source for healthcare news, ideas and analysis.

HMA Insights—including briefs, webinars, and our podcast—gives you easy access to HMA’s deep expertise, helping you stay current on the latest healthcare trends and topics. Search for a topic of interest or browse the latest insights below.

This 10-slide presentation, Medicaid Expansion: Data-Driven Insights into Healthcare Needs, offers a focused analysis of the Medicaid Expansion population—non-disabled adults ages 19–64 with incomes up to 138% of the Federal Poverty Level—across more than 40 states. Using recent T-MSIS data, the deck highlights the high prevalence of chronic and behavioral health conditions within this group, while also detailing demographic trends among the approximately 16 million enrollees.

Developed by Matt Powers, Shreyas Ramani, Loren Anthes, and Lora Saunders, the presentation contextualizes health needs with Medicaid spending patterns, comparing the Expansion group to other eligibility categories, such as dual eligibles and children. It also breaks down pharmacy spending by therapeutic class, spotlighting common conditions like opioid use disorder. In light of recent federal legislative proposals such as H.R. 1, the deck explores how states are beginning to navigate policy changes through 1115 waiver activity—particularly around medically frail and good cause exemptions—offering early insight into likely implementation strategies.

Watch our Medicaid Town Hall hosted by Health Management Associates. Our experts answered your questions live on a wide range of timely and critical topics, including:

Key policies and insights about the ongoing 2025 federal budget reconciliation negotiations, including changes to Medicaid eligibility policies, financing, and cost-sharing rules.

New executive branch priorities to address program integrity and agency regulations and guidance reshaping provider tax rules and state-directed payment arrangements.

The evolving landscape of Medicaid Section 1115 demonstrations, including updated federal monitoring approaches and new state initiatives.

Medicaid managed care trends, payment innovation, and emerging strategies to address whole-person care focused on maternal health and behavioral health needs.

As Congress intensifies negotiations over budget reconciliation, including potential changes to Medicaid financing and Affordable Care Act (ACA) subsidies, new data from Wakely Consulting Group, an HMA (Health Management Associates) company, sheds light on how the effects of the Medicaid redetermination process continued to unfold well into 2024. Appendix A of the May 2025 white paper Medicaid Redetermination Impacts on the Individual Market, provides a full-year view of enrollment and morbidity trends, showing that the influx of former Medicaid enrollees had some negative effects on risk scores. In fact, relative risk increased across all market types—state-based exchanges (SBEs), in federally facilitated exchange (FFE) Medicaid expansion states, and FFEs in non-expansion states—despite substantial enrollment growth.

Data presented in Wakely’s white paper and their experts’ findings challenge the conventional assumption that higher enrollment dilutes risk and suggest that many new enrollees may have had unmet health needs or delayed care. The data also show that states with the highest enrollment growth did not necessarily experience the greatest morbidity shifts. This decoupling of enrollment and morbidity complicates forecasting for insurers and policymakers alike, especially as Congress debates Medicaid funding and ACA subsidy structures in the ongoing budget reconciliation process.

What to Watch

As federal lawmakers consider reforms that could alter Medicaid eligibility, subsidies, and risk adjustment mechanics, these findings underscore the importance of monitoring not just how many people enroll, but who they are and the type of care they need. The individual market’s evolving risk profile will have direct implications for premium setting, subsidy design, and the financial stability of plans that serve this population.

Connect with Us

Wakely is experienced in all facets of the healthcare industry—from carriers to providers to government agencies. Wakely’s actuarial experts and policy analysts continually monitor and analyze potential changes to inform clients’ strategies and propel their success.

For more questions about the analysis contact our experts below.

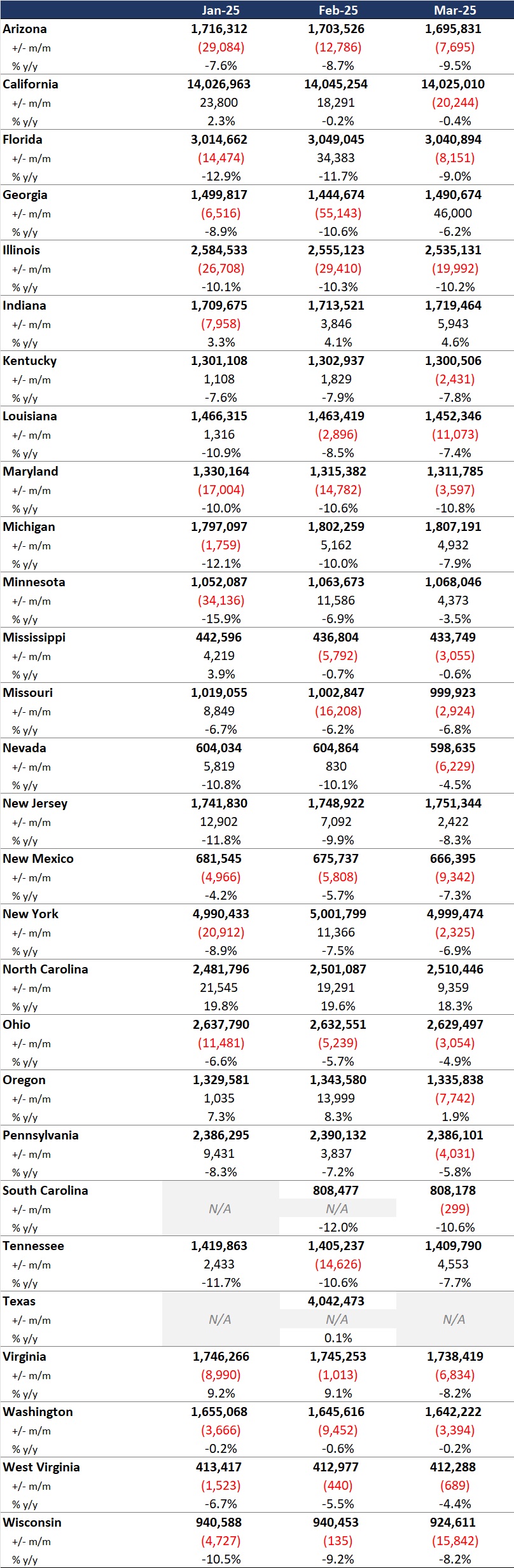

In this week’s In Focus section, Health Management Associates Information Services (HMAIS) draws on its database of monthly enrollment in Medicaid managed care programs to provide the latest quarterly analysis of Medicaid managed care enrollment, offering a snapshot of developments across 28 states.[1] The data and insights are particularly timely as stakeholders, including states, Medicaid managed care organizations (MCOs), hospitals and health systems, and providers, continue to plan for multiple possible federal policy changes and the operational realities that will follow.

HMAIS also compiles a more detailed quarterly Medicaid managed care enrollment report representing nearly 300 health plans in 41 states. The report provides by plan enrollment plus corporate ownership, program inclusion, and for-profit versus not-for-profit status, with breakout tabs for publicly traded plans. Table 1 shows a sampling of plans and their national market share of Medicaid managed care beneficiaries based on a total of 66 million enrollees. These data should be viewed as a broader representation of enrollment trends rather than as a comprehensive comparison.

Key Insights from Q1 2025 Data

The 28 states included in our review have released monthly Medicaid managed care enrollment data via a public website or in response to a public records request from Health Management Associates (HMA). This report reflects the most recent data posted or obtained. HMA has made the following observations related to the enrollment data:

Year-over-year growth. As of March 2025, across the 28 states reviewed, Medicaid managed care enrollment declined by 2.5 million members year-over-year, a 3.9 percent drop as of March 2025 (see Figure 1). This marks a continuation of the downward trend reported in late 2024, though with notable variation across states.

Figure 1. Year-over-Year Growth in Medicaid Managed Care States, 2020−24, March 2025

Localized growth amid broader declines. While most states experienced enrollment reductions, Indiana and North Carolina bucked the trend with measurable gains, suggesting the influence of state-specific policy shifts or demographic factors. Oregon and Texas also saw modest growth.

Sharpest contractions. Illinois, Maryland, and South Carolina, reported double-digit percentage drops, underscoring the uneven impact of redeterminations and eligibility changes.

Difference among expansion and non-expansion states. Among the 21 states included in our analysis that expanded Medicaid, enrollment fell by 1.8 million (-3.6%) to 48.6 million. In contrast, the seven non-expansion states saw a steeper proportional decline (-5.4%), to a total of 12.2 million enrollees.

Table 1. Monthly MCO Enrollment by State, January 2025 through March 2025

Note: In Table 1 above and the state tables that follow, “+/- m/m” refers to the enrollment change from the previous month, and “% y/y” refers to the percentage change in enrollment from the same month in the previous year.

It is important to note the limitations of the data presented. First, states report the data at the varying times during the month. Some of these figures reflect beginning of the month totals, whereas others reflect an end of the month snapshot. Second, in some instances, the data are comprehensive in that they cover all state-sponsored health programs that offer managed care options; in other cases, the data reflect only a subset of the broader managed Medicaid population. This limitation complicates comparison of the data described above with figures reported by publicly traded Medicaid MCOs. Hence, the data in Table 1 should be viewed as a sampling of enrollment trends across these states rather than a comprehensive comparison, which cannot be established solely based on publicly available monthly enrollment data.

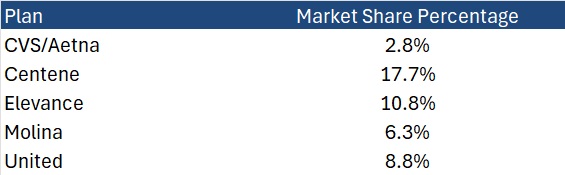

Market Share and Plan Dynamics

Using our data repository from 300 health plans across 41 states, HMAIS’s report addresses corporate ownership, program participation, and tax status. As of March 2025, Centene continues to lead with 17.7 percent of the national Medicaid managed care market, followed by Elevance (10.8%), United (8.8%), and Molina (6.3%), as Table 2 shows.

Table 2. National Medicaid Managed Care Market Share by Number of Beneficiaries for a Sample of Publicly Traded Plans, March 2025

What to Watch

The policy backdrop remains fluid. The US House of Representatives’ passage of the One Big Beautiful Bill Act introduces sweeping changes to Medicaid financing, including proposed cuts of up to $715 billion. Additional federal proposals, such as mandatory work requirements, could further reshape enrollment patterns.

Stakeholders should prepare for:

Implementation of work/community engagement mandates for certain adult populations

Potential redesign of Affordable Care Act expansion programs

Retraction of federal regulations focused on streamlining of eligibility and redetermination processes to improve accuracy and efficiency

Connect with Us

HMA is home to experts who know the Medicaid managed care landscape at the federal and state levels. As the Medicaid landscape continues to evolve, HMAIS equips stakeholders with timely, actionable intelligence. Our subscription service includes enrollment data, financials, waiver tracking, and a robust library of public documents.

For more information about the HMAIS subscription, contact our experts below.

[1] Arizona, California, Florida, Georgia, Illinois, Indiana, Kentucky, Louisiana, Maryland, Michigan, Minnesota, Mississippi, Missouri, Nevada, New Jersey, New Mexico, New York, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Tennessee, Texas, Virginia, Washington, West Virginia, Wisconsin.

As Medicaid faces another set of policy shifts, this episode provides a look-back on the many twists and turns Medicaid has faced throughout the years. Jay Rosen, president and chairman of HMA, reflects on his work with states and health plans over the past four decades in their efforts to deliver services to vulnerable populations amidst shifting federal and state priorities, innovative delivery and payment models, and increased private sector involvement. With a sharp focus on policy, equity, and system transformation, Jay offers strategic insights for leaders across healthcare, government, and investment sectors.

HMA focused this paper on how states disperse Medicaid funds to certain subpopulations within the program’s categorical eligibility infrastructure. A previous companion paper centered on increasing our understanding of Medicaid managed care spending by provider, offering more detail on the relative order of magnitude of the amounts spent on inpatient and outpatient hospital care, professional services, long-term care, pharmacy, and other health services.

As the latest national Medicaid managed care enrollment data show 75% of Medicaid beneficiaries were enrolled in comprehensive managed care organizations (MCOs), these two foundational papers illustrate the importance of developing a sound methodology to reliably estimate costs associated with MCOS. These papers, which are the first to present findings related to the development of the MCO methodologies, help lay the foundation for further work that will enable us to answer relevant questions, including:

How much do we spend on Medicaid patients with chronic conditions like asthma, diabetes, and hypertension?

How much do we spend on Medicaid patients receiving long-term services and supports (LTSS) and what is the unmet need?

How is Medicaid funding spent on childbirth and a child’s first year of life?

What are the opportunities to be more efficient and effective with Medicaid resources?

In May 2025, the US House of Representatives passed a budget bill that includes funding for cost-sharing reduction (CSR) payments, marking a potential end to the “silver loading” practice that has shaped pricing in the Affordable Care Act (ACA) Marketplace pricing since 2017. The US Senate is now considering this legislation as part of a broader budget reconciliation package that includes major Medicaid reforms, such as new work requirements and changes to eligibility and financing rules.

This evolving policy landscape has significant implications for states, payers, providers, and consumers. Wakely, an HMA Company, recently published Implications of Ending Silver-Loading on the Individual Market, which outlines how reinstating CSR payments could reshape ACA marketplace plan pricing, enrollment patterns, and federal subsidy flows. It also highlights the operational and financial risks stakeholders must prepare for in 2026.

Broad Loading and Silver Loading

Because CSR loading increases premium costs on silver plans that determine subsidies, they also increase federal payments for premium tax credit (PTC) subsidies. Guidance from the US Department of Health and Human Services on silver plan pricing has evolved over time. Three types of CSR loading are occurring in ACA markets, specifically:

Broad loading: Increasing premiums for all metal level qualified health plans (QHPs) in the individual market to collect enough revenue to offset the CSR costs of the silver plan variants enrollees

Two means of silver loading:

Increasing premiums for only silver QHPs in the individual market to collect enough revenue to offset the CSR costs of the silver plan variant enrollees

Raising premiums, functionally, for only on-exchange silver QHPs

As discussed in the Wakely paper, the impact of silver loading is that the federal government is likely paying out more in additional PTC subsidies than would be paid if CSR payments were fully funded. On Friday, May 2, 2025, the Centers for Medicare & Medicaid Services (CMS) released guidance related to silver loading and CSR payments for 2026 rate filings. This action was urgently needed, especially for states with May filing deadlines.

What’s at Stake

If Congress does appropriate funding for CSR payments, some issuers will be reimbursed for the difference in cost sharing between standard and CSR-enhanced silver plans. Issuers that cover nonemergency pregnancy termination services, would be ineligible for CSR payments; however, as the Wakely paper indicates, these payments would not cover the additional utilization driven by richer benefits. For example, it is anticipated that a member in a 94 percent actuarial value CSR plan will use more services (i.e., four primary care visits versus three in a standard plan), but reimbursement would only reflect the cost-sharing difference—not the increased volume of care.

States like Georgia and New Mexico, which mandate silver loading, could see significant shifts in premium relativities and enrollment behavior. Wakely’s modeling suggests that changes in CSR policy—especially if paired with the expiration of enhanced premium subsidies at the end of 2025—could lead to higher net premiums, reduced enrollment, and a deterioration in risk pool morbidity.

What to Watch

The Senate’s deliberations will determine whether CSR funding is restored and could have significant implications on whether enhanced premium subsidies are extended beyond 2025. These decisions will directly affect the following:

2026 rate filings and benefit designs

Marketplace affordability and enrollment stability

State reinsurance funding and 1332 waiver dynamics

Consumer costs and plan switching behavior

Wakely’s analysis also cautions that if CSR funding is restored without accounting for induced utilization, issuers may still need to price for higher service use—potentially leading to premium volatility. In addition, if broad loading is mandated instead of silver loading, it could raise premiums across all metal tiers and reduce the value of premium tax credits for many enrollees.

Key Considerations for Stakeholders

States should assess how CSR policy changes affect reinsurance programs, waiver funding, and Medicaid redeterminations.

Payers must prepare for multiple pricing scenarios and evaluate how changes in subsidy structures influence enrollment and risk adjustment, 1332 reinsurance programs, and overall market risk.

Providers should anticipate shifts in patient mix and utilization (i.e., more uncompensated care with more uninsured patients).

Advocates need to monitor how policy changes affect access and affordability for low-income and underserved populations.

These developments also create more opportunities for movement between Medicaid, Marketplace, and uninsured populations, underscoring renewed opportunity for integrated eligibility systems and coordinated outreach.

Connect with Us

Health Management Associates (HMA), experts are actively advising stakeholders on how to navigate these complex changes. Whether you’re a state policymaker, health plan executive, provider leader, or advocate, we can help you assess the impact and plan strategically.

These issues will also be explored in depth at the HMA Conference in October 2025. To discuss how these developments will affect your organization, contact our featured expert below.

On May 22, 2025, the US House of Representatives advanced a comprehensive legislative package that includes expansive changes to healthcare spending and tax policies. The One Big Beautiful Bill Act, H.R. 1, will be subject to further revision in the Senate – and potentially again in the House – before it can be sent to the president for his signature. If enacted, the legislation would have significant implications for the Medicaid program, including a nationwide work and community engagement requirement. The House-passed bill establishes a deadline of December 31, 2026, for implementation, but individual states could move earlier.

As state legislatures pass work requirement bills, governors consider executive actions, and Congress contemplates revisions to the Medicaid work mandate, vetting key implementation issues may significantly affect the direction of related policies. Even before implementation, states must test operations, enable systems, and establish connections to beneficiaries to reduce potential implementation missteps, inappropriate disenrollments, and litigation risks.

If the goal of Medicaid work requirement policies is to stimulate connections between health benefits and employment/workforce, building state and federal capacities to support these approaches is critical to effectuating that change. In the remainder of this article, Health Management Associates (HMA), experts focus on the operational dynamics that need to be discussed, tested, and built as states begin introducing work and community engagement initiatives.

Federal Policies and Early State Actions on Work Requirements

The House bill would require all states to implement work and community engagement requirements for adults without dependents for at least 80 hours per month.[1] Employment, work programs, education, or community service (or a combination of those activities) would satisfy the requirement.

The work requirements in the House-passed legislation would apply only to individuals between the ages of 19 and 64 without dependents, and the following groups are exempted:

Women who are pregnant or entitled to postpartum medical assistance

Members of Tribes

Individuals who are medically frail (i.e., people who are blind, disabled, with chronic substance use disorder, has serious or complex medical conditions, or others as approved by the Secretary of the US Department of Health and Human Services)

Parents of dependent children or family caregivers to individuals with disabilities

Veterans

People who are participating in a drug or alcoholic treatment and rehabilitation program

Individuals who are incarcerated or have been released from incarceration in the past 90 days

In addition, individuals who already meet work requirements through other programs, such as Temporary Assistance for Needy Families (TANF) or the Supplemental Nutrition Assistance Program (SNAP), would be exempt. However, the House-passed version would make the eligibility verification and work requirements for SNAP more stringent and shift program costs to these states, which would affect cross-functional eligibility. The legislation also includes temporary hardship waivers for natural disasters and areas with an unemployment rate greater than 8 percent (150 percent of the national average).

Though the federal budget package has received a great deal of attention, at least 14 states already have moved forward (see Table 1) in advance of the current federal debate by passing laws and submitting work requirement demonstration requests to the Centers for Medicare & Medicaid Services (CMS).

Table 1. A Review of 2025 States’ Approaches to Work Requirements in Medicaid

Status

State

Population Criteria

Requirements

Exemptions/ Notes

Public Comment

Work Requirement Request Submitted

Arizona

Ages 19−55

80 hours/month

Multiple exemptions; 5-year lifetime limit

Closed

Work Requirement Request Submitted

Arkansas

Ages 19−64; covered by a qualified health plan (QHP)

Data matching to assess whether on track/not on track

No exemptions

Closed

Work Requirement Amendment Request Submitted

Georgia

Ages 19−64; 0-100% FPL

80 hours/month

Already has approval but is requesting reporting be changed from monthly to annually and adding more qualifying activities

Federal comment period open through June 1, 2025

Work Requirement Request Submitted

Ohio

Ages 19−54; expansion adults

Unspecified hours

Limited list of exemptions

Closed

Legislation Passed

Idaho

Ages 19−64

20 hours/week required

Limited list of exemptions

—

Legislation Passed

Indiana

Ages 19−64; expansion adults

20 hours/week required

Limited list of exemptions

—

Legislation Passed

Montana

Ages 19−55

80 hours/month required

Multiple exemptions

—

Ballot Initiative Passed

South Dakota

Expansion adults

—

2024 ballot initiative asking voters for approval for state to impose work requirements for expansion adults passed

—

Legislation Pending

North Carolina

—

—

Pursue requirements that are CMS approvable

—

Work Requirement Request Draft

Iowa

Ages 19−64; expansion adults

100 hours/month required

Limited list of exemptions Separate bill would end expansion if work requirements are withdrawn/ prohibited (80 hr./mo.)

Closed

Work Requirement Request Draft

Kentucky

Ages 19−60; no dependents; enrolled more than 12 months

Connected to employment resources

Multiple exemptions

State comment period open through June 12, 2025

Work Requirement Request Draft

South Carolina

Ages 19−64; 67%−100% FPL

Specified activities (work specific is 80 hours/month)

Limiting participation to 11,400 individuals based upon available state funding

State comment period open through May 31, 2025

Work Requirement Request Draft

Utah

Expansion adults ages 19−59

Register for work, complete an employment training assessment and assigned job training, and apply to jobs with at least 48 employers within 3 months of enrollment

Several exemptions, largely aligned with federal SNAP exemptions

State comment period open through May 22, 2025

Anticipated Waiver Request

Alabama

Non-expansion population

—

Potential to resubmit previous work requirement demonstration request

—

Key Questions to Guide State Policy Decisions

Considerable research and findings from previous Medicaid work requirement initiatives can help prepare policymakers to implement a potential new phase of Medicaid work requirement policies. Some previous findings include the high cost of administration relative to potential savings, the importance of systems that support foundational items like logging an enrollee’s compliance activities and exemptions, as well as developing an efficient appeals process. The Medicaid and CHIP Payment and Access Commission (MACPAC), General Accounting Office, National Institutes for Health, and multiple researchers have published assessments regarding previous experiences that could prove useful in policy making.

HMA experts have experience identifying key issues and considerations, analyzing options, and implementing critical issues and for state leaders and stakeholders who will be responsible for implementing work requirements. Several of these issues are described below and in more detail in the HMA blog, Building State Capacities for Medicaid Work and Community Engagement Requirements.

Exemptions, particularly medical frailty definitions and assessments. The federal government and states will need to identify individuals classified as “medically frail” and make them exempt from the mandates. Medically frail individuals include those with chronic, serious, or complex medical conditions. Various methods can be employed to identify these people.

Developing and streamlining systems and processes to promote continued coverage for eligible individuals. The Medicaid unwinding from the COVID public health emergency taught policymakers lessons about the complexities of Medicaid systems, patient engagement, and reliable methods of member outreach. State Workforce Commissions and Departments of Labor are clear partners, as they manage integrated eligibility systems and data-sharing agreements across programs like SNAP and TANF, which also serve many Medicaid participants. These and other partnerships will need further exploration.

Clinical and utilization data that promote eligibility assessment. Many, but not all, individuals with chronic diseases may be exempt from the requirements. Knowing the health status and chronic conditions of the populations affected and the conditions that qualify people for exemption are variables as implementation questions, like the definition of medically frail, are addressed.

Anticipated need for effective Medicaid managed care engagement in work requirements/community engagement initiatives. Approximately 80 percent of Medicaid expansion enrollees are members of comprehensive managed care organizations (MCOs). States will need to review the scope of existing vendor contracts as well as determine the need for new services, roles, third-party reporting, oversight, and potential exemptions for emergencies. Work requirements can disrupt MCO risk pool stability and care coordination. MCOs have a financial incentive to drive down inappropriate disenrollments and are uniquely positioned to support state responsibilities, including maintenance of up-to-date contact information.

Measuring impact and adapting policies as needed. Dynamic metrics that provide actionable information to federal and state policy makers will support effective oversight and monitoring.

Connect with Us

HMA helps stakeholders—including state agencies and their partners—manage the challenges of implementing new Medicaid or CHIP initiatives, with a focus on ensuring efficient integration and improvements in outcomes. Our teams are adept at developing materials for and supporting stakeholder engagement from design to implementation, which is a critical aspect for work and community engagement initiatives and other potential new eligibility and renewal requirements.

For support tracking federal and state level developments and enhancing your organization’s strategy and preparations for new Medicaid requirements, contact our featured experts below.

Medicaid covers nearly 80 million people nationally, with an estimated 20 million covered through the Medicaid expansion. As state legislatures pass work requirement laws, governors consider executive actions, and Congress contemplates a nationwide mandate, vetting key implementation issues can significantly impact the direction of related policies.

It is difficult to generate accurate projections given the lack of specificity in the current legislation and state implementation variables. According to Congressional Budget Office (CBO) estimates, approximately 5 million people with coverage because of the Medicaid expansion would lose their coverage as a result of not meeting community engagement requirements. The legislation passed by the House on May 22nd establishes a deadline of December 31, 2026 for implementation, but individual states could move earlier. Even before implementation, states must test operations, enable systems, and establish connections to beneficiaries to reduce potential implementation missteps, inappropriate disenrollments, and litigation risks.

If the goal of Medicaid work requirement policies is to stimulate connections between health benefits and employment/workforce, building state and federal capacities to support these approaches is critical to effectuating that change. This blog focuses on introducing operational dynamics that need to be discussed, tested, and built.

Legislative and Other Context

In the language that House advanced, all states would be obliged to implement work and community engagement requirements for adults without dependents for at least 80 hours per month.[1] Employment, work programs, education, or community service (or a combination of those activities) would satisfy the requirement. There were also provisions which enabled states to implement more frequent eligibility checks and compliance requirements as well as co-pays for certain services. Though the federal authorization has received a great deal of attention, at least 14 states have moved forward (see Table 1) in advance of the current federal debate by passing laws and submitting work requirement demonstration requests to the Centers for Medicare & Medicaid Services (CMS).

Table 1. A Review of 2025 States’ Approaches to Work Requirements in Medicaid

Status

State

Population Criteria

Requirements

Exemptions/ Notes

Public Comment

Work Requirement Request Submitted

Arizona

Ages 19−55

80 hours/month

Multiple exemptions; 5-year lifetime limit

Closed

Work Requirement Request Submitted

Arkansas

Ages 19−64; covered by a qualified health plan (QHP)

Data matching to assess whether on track/not on track

No exemptions

Closed

Work Requirement Amendment Request Submitted

Georgia

Ages 19−64; 0-100% FPL

80 hours/month

Already has approval but is requesting reporting be changed from monthly to annually and adding more qualifying activities

Federal comment period open through June 1, 2025

Work Requirement Request Submitted

Ohio

Ages 19−54; expansion adults

Unspecified hours

Limited list of exemptions

Closed

Legislation Passed

Idaho

Ages 19−64

20 hours/week required

Limited list of exemptions

—

Legislation Passed

Indiana

Ages 19−64; expansion adults

20 hours/week required

Limited list of exemptions

—

Legislation Passed

Montana

Ages 19−55

80 hours/month required

Multiple exemptions

—

Ballot Initiative Passed

South Dakota

Expansion adults

—

2024 ballot initiative asking voters for approval for state to impose work requirements for expansion adults passed

—

Legislation Pending

North Carolina

—

—

Pursue requirements that are CMS approvable

—

Work Requirement Request Draft

Iowa

Ages 19−64; expansion adults

100 hours/month required

Limited list of exemptions Separate bill would end expansion if work requirements are withdrawn/ prohibited (80 hr./mo.)

Closed

Work Requirement Request Draft

Kentucky

Ages 19−60; no dependents; enrolled more than 12 months

Connected to employment resources

Multiple exemptions

State comment period open through June 12, 2025

Work Requirement Request Draft

South Carolina

Ages 19−64; 67%−100% FPL

Specified activities (work specific is 80 hours/month)

Limiting participation to 11,400 individuals based upon available state funding

State comment period open through May 31, 2025

Work Requirement Request Draft

Utah

Expansion adults ages 19−59

Register for work, complete an employment training assessment and assigned job training, and apply to jobs with at least 48 employers within 3 months of enrollment

Several exemptions, largely aligned with federal SNAP exemptions

State comment period open through May 22, 2025

Anticipated Waiver Request

Alabama

Non-expansion population

—

Potential to resubmit previous work requirement demonstration request

—

Key Questions Regarding State Policy Options

Considerable research and findings put policymakers in a better position to be prepared to act on a new law since previous attempts and implementing similar policies exposed fundamental problems. Some previous findings include the high cost of administration relative to potential savings, the importance of systems that support foundational items like logging an enrollee’s compliance activities and exemptions, as well as developing an efficient appeals process. The Medicaid and CHIP Payment and Access Commission, General Accounting Office, National Institutes for Health, and multiple researchers have published assessments regarding previous experiences that could improve policymaking.

Below we discuss critical issues and considerations including:

Exemptions, particularly medical frailty definitions and assessments

Developing and streamlining systems and process to promote continued coverage for eligible individuals

Clinical and utilization data that promotes eligibility assessment

Managed Care engagement in Work Requirements/Community Engagement initiatives

Measuring impact and adapting policies where needed

1. Which populations are exempt from work requirements?

The requirements in the current legislation would apply only to individuals between the ages of 19 and 64 without dependents, and the following groups are exempted: women who are pregnant or entitled to postpartum medical assistance, members of Tribes, individuals who are medically frail (i.e., people who are blind, disabled, with chronic substance use disorder, serious or complex medical conditions, or others as approved by the Secretary of the U.S. Department of Health and Human Services), parents or caregivers to a dependent child or individuals with a disability, veterans, people who are participating in a drug or alcoholic treatment and rehabilitation program, or individuals who are incarcerated or have been released from incarceration in the past 90 days. Additionally, individuals who already meet work requirements through other programs, such as Temporary Assistance for Needy Families (TANF) or the Supplemental Nutrition Assistance Program (SNAP), would be exempt. However, according to the House-passed version, the eligibility verification and work requirements for SNAP have been made more stringent and program costs are being shifted to states, which affects cross-functional eligibility. Lastly, the legislation includes temporary hardship waivers for natural disasters and areas with an unemployment rate greater than 8 percent or 150 percent of the national average.

The federal government and/or states will identify individuals classified as “medically frail” and make them exempt them from the mandates. This includes those with chronic, serious, or complex medical conditions. Various methods may be employed to identify these individuals, such as analyzing historical medical and pharmacy data to categorize complex conditions, using proprietary algorithms to stratify individuals with multiple comorbidities, and enabling physicians to evaluate enrollees without relying on a claims history.

2. Which systems best align to build from and support coverage?

The Medicaid unwinding from the COVID Public Health Emergency taught lessons about the complexities of Medicaid systems (e.g., assessing cases to ensure eligible children retain coverage if a parent is removed), patient engagement, and reliable methods of member outreach (e.g., email, text, and member portals rather than paper communication). Call abandonment rates, call center wait times, and application processing times surfaced as practical measures of performance (or lack thereof) during the Medicaid unwinding. Multiple informal sources point to poor mailing address or “return to sender” as being anywhere between 15 and 50 percent, bringing tangibility to an implementation baseline. TANF and SNAP programs have work requirement provisions. While those programs are regulated and administered by multiple federal and state agencies, the platforms that support those provisions and the potential for integration are critical vehicles to explore.

State Workforce Commissions and Departments of Labor are clear partners, as they manage integrated eligibility systems and data-sharing agreements across programs like SNAP and TANF, which also serve many Medicaid participants. These and other partnerships will need to be explored to address engagement challenges for many populations, including individuals facing housing instability, which disrupts communication, engagement, and compliance tracking.[2] It is essential that states develop targeted outreach and education strategies to support awareness of participation requirements and ways for individuals to meaningfully engage.

3. Do we have a sense of the healthcare needs/chronic conditions among the Medicaid enrollees that will be affected by work requirements?

Many individuals with chronic diseases may be exempt from the requirements, but not all of them. To that end, insights regarding pharmacy claims may be a useful lens through which we can ascertain an understanding of the potential impact on utilization trends. Notably, the Medicaid expansion population still has significant healthcare utilization rates for services related to behavioral health and for chronic health conditions like hypertension and diabetes. In fact, a recent Health Management Associates (HMA), analysis of CMS data indicated that the top pharmaceuticals spending classes for the Medicaid expansion population were hypoglycemics ($7.6 billion), antivirals ($5.5 billion), and anti-inflammatories ($3.3 billion). The drugs are used to treat autoimmune conditions, including rheumatoid arthritis and psoriatic arthritis. Knowing the health status and chronic conditions of the populations affected and which conditions qualify for exemption are variables as implementation issues like the definition of medically frail are addressed.

4. What does this mean for managed care organizations?

Approximately 80 percent of Medicaid expansion beneficiaries are enrolled in comprehensive managed care organizations (MCOs). States will need to review the scope of existing vendor contracts as well as determine the need for new services, roles, third-party reporting, oversight, and potential exemptions for emergencies. Work requirements can disrupt MCO risk pool stability and care coordination because of administrative burdens and disruptive, less predictable enrollment cycles. That said, MCOs not only have a financial incentive to drive down inappropriate disenrollments, but are also uniquely positioned to support state responsibilities, including maintenance of up-to-date contact information. The delineation of roles and clarification of contracts and responsibilities among states, MCOs, TPAs, and other specialty organizations supporting work requirements will be a critical early-stage framing point for a functional infrastructure.

Many states have sought to support more seamlessness among insurers, with a goal of having the same insurers provide coverage to people as they transition through Medicaid, Marketplace, and employer-sponsored insurance (ESI) as their employment status changes over time. States like Nevada, Rhode Island, and New Mexico require Medicaid MCOs to participate in the Marketplace. Additionally, states like North Carolina, Utah, and West Virginia not only require MCO participation in the Marketplace, but also enable MCOs to co-market Medicaid and Marketplace products for individuals who lose their Medicaid eligibility.

As Figure 1 indicates, Marketplace enrollment in non-expansion states has received considerable traction in recent years and has outpaced expansion states with respect to member growth in the past five years. Marketplaces have undeniably carved out large roles in the health coverage infrastructure in non-expansion states—a point that was less clear just a few years ago. Though, multiple factors affect those Marketplace growth rates, including congressional decisions regarding the continuation and funding of the enhanced premium tax credit program. In the current legislation, these credits expire, which the CBO estimates will lead to an additional coverage loss of nearly 5 million by 2034.

5. Can states measure and be nimble with policies as the impacts are determined?

Federal and state regulations that identify contextualized and dynamic metrics that provide actionable information to federal and state policy makers will support effective oversight and monitoring. States starting with listening sessions in the near term can help identify goals and metrics. The focus of such efforts could include actively monitoring potential changes and cost shifts for the uninsured population to non-public payers and providers.

The Medicaid unwinding also demonstrated that the story was far less of a red/blue story than a series of complex tasks that required many administrative resources, provider and community partnerships, and enrollee outreach to create a path that would limit unnecessary disruptions and expenses. CMS guidance for goals and evaluations as well as state inputs will need to emerge prior to implementation so policymakers can be well-equipped to be nimble and dynamic with policy changes as well as understanding the short-term and longitudinal effects of this fundamental shift.

[2] Soni A, Blackburn J. Health Characteristics of Adults Unable to Complete Medicaid Renewal During the Unwinding Period. JAMA Health Forum. 2025;6(3):e250092. doi:10.1001/jamahealthforum.2025.0092

This week, key committees in the House of Representatives released recommendations for legislative language that meets their federal savings and spending targets required in the fiscal year (FY) 2025 budget resolution. On May 11, 2025, the House Energy and Commerce Committee released legislation—and subsequently a substitute amendment—that contains several substantive Medicaid proposals designed to address eligibility and enrollment; financing; fraud waste, and abuse; and to institute mandatory work and community engagement requirements and cost sharing. The Committee completed its markup on May 14, 2025, voting to approve the provisions in the substitute amendment.

The release of text and committee markups are key steps in Congress’s budget reconciliation process; however, proposals may change during Senate proceedings.

Health Management Associates (HMA), and Leavitt Partners, an HMA company, are tracking these developments and analyzing the extensive health and health-related legislative text, including the Medicaid, Medicare, and Affordable Care Act (ACA) Marketplace proposals. Below, we review the status of congressional efforts and key policies.

Background

The budget reconciliation process is a powerful tool for enacting significant fiscal policy changes, as it allows for expedited consideration and passage of budget-related legislation. It has been used in the past to enact major tax reforms, healthcare legislation, and other important budgetary measures.

In 2025, Congress has been actively working to develop its budget bills through a series of steps. The House adopted a budget resolution on February 25, 2025, which sets the framework for federal spending, revenue, and the debt limit for fiscal year 2025 and outlines budgetary levels for the following years through 2034. The Senate passed an amended version of the budget resolution on April 5, 2025. The Senate’s amendments included reconciliation instructions that require $4 billion in gross deficit reductions and allow a $5.8 trillion net deficit increase. On April 10, 2025, the House agreed to the Senate’s amendments with a vote of 216−214. This agreement set the stage for the development of a reconciliation bill.

House Energy and Commerce Markup

On May 14, 2025, the House Committee on Energy and Commerce completed its second day of marking up legislative language to comply with the Concurrent Resolution on the Budget for Fiscal Year 2025, voting to advance the proposals out of committee. The committee’s proposal excluded certain significant structural reforms that had generated concern among some members and stakeholders, such as broad reductions in the federal matching rate (enhanced federal matching assistance percentage (FMAP)) for Medicaid expansion populations, per-capita caps on federal Medicaid cost growth, or reductions in the safe harbor threshold for state Medicaid provider taxes. The proposal does, however, contain more than a dozen provisions that would reduce federal health care spending by $715 billion with the funding reductions mostly focused on Medicaid, which the Congressional Budget Office projects will reduce the federal share of Medicaid spending, including:

Adding mandatory work and community engagement requirements for individuals ages 19−64 without dependents, subject to exceptions for pregnant women, people who are medically frail, people with disabilities, people in compliance with other government program work requirements, people living in areas experiencing a temporary hardship, and other individuals

Adding cost sharing for beneficiaries in the expansion population who earn more than 100 percent of the Federal Poverty Level, not to exceed $35 per item or service

Pausing implementation of several final rules published during the Biden Administration, including: the final rule published September 21, 2023, “Streamlining Medicaid; Medicare Savings Program Eligibility Determination and Enrollment”; the April 2, 2024 rule, “Streamlining the Medicaid, Children’s Health Insurance Program, and Basic Health Program Application, Eligibility Determination, Enrollment, and Renewal Processes”; and the May 10, 2024, final rule, “Minimum Staffing Standards for Long Term Care Facilities and Medicaid Institutional Payment Transparency Reporting”

Adding provider screening requirements

Increasing frequency of eligibility redeterminations for certain individuals and adding enrollee address verification policies

Reducing expansion FMAP for certain states that provide Medicaid coverage to undocumented individuals and families, regardless of the source of funding

Preventing certain spread pricing arrangements in Medicaid between states and pharmacy benefit managers

Restricting funding for certain essential community providers that furnish family planning services, reproductive health, and related healthcare services

Ending a temporary increased FMAP to new states adopting Medicaid expansion, revising policies governing the use of Medicaid provider taxes, and payment limits for state directed payments

Committee Markups

Various other House committees have begun holding markups for the reconciliation package. The Committee on Ways and Means conducted its markup on May 13, 2025, to discuss its portion of the reconciliation bill, which involves $4.5 trillion in deficit increases. The initial Ways and Means proposal did not include many significant healthcare proposals, but on May 12, 2025, the committee released a substitute amendment that includes several changes that would affect private insurance coverage and Medicare. Key provisions include:

Changes to Medicare and ACA premium tax credit (PTC) eligibility requirements related to immigration status

Improvements to ACA PTC eligibility verification checks

Changes to Health Savings Account flexibilities

Codification and renaming of individual coverage health reimbursement accounts, which serve as a defined contribution that employees can use to purchase insurance in the individual market

Other committees, such as the Education and Workforce, Judiciary, Armed Services, and Homeland Security Committees, also have conducted markups and approved their respective portions of the reconciliation bill.

Connect With Us

These steps are part of the ongoing process to finalize the budget and reconciliation legislation for FY 2025. Our federal policy experts with Leavitt Partners and across HMA are monitoring the legislative policies and ongoing negotiations in Congress and with the administration. They work with healthcare organizations and industry to plan for the range of scenarios and policies Congress is debating.

For more information about the impact of these policies, contact our featured federal policy experts below.

Section 1115(a) demonstrations, informally known as 1115 waivers, are experimental, pilot, or demonstration projects that give states flexibility to design, test, and evaluate state-specific approaches to improve their healthcare programs and better serve eligible populations.

Approved by the Centers for Medicare & Medicaid Services (CMS), 1115 demonstrations provide alternative options to provide access, coverage, financing, and delivery of services under the joint federal-state funded programs Medicaid and the Children’s Health Insurance Program (CHIP). Across multiple administrations, HMA has helped state Medicaid agencies and cross-agency leaders design programs aligned with federal priorities; develop budget-neutral pathways and sustainable financing strategies; reduce operational, financial, and implementation risk; and position programs for long-term success.

Medicaid and CHIP 1115 demonstrations allow states—and their stakeholders—to test new innovations to improve the health of enrollees and advance program efficiencies. These demonstrations require careful planning, rigorous actuarial analysis, political savvy, policy knowledge, and ongoing support through the application, approval, and implementation phases. In today’s environment, 1115 programs must be responsive to the policy priorities at the federal level and grounded in solutions that work in the state. Stakeholders need aligned engagement strategies and communications plans to achieve shared goals, including monitoring that drives continuous improvements after implementation.

HMA consultants bring extensive real-world and leadership expertise from decades of working with states and federal agencies prior to joining HMA. We offer the range of services and support needed to ensure 1115 programs are financially sustainable, operationally workable, and aligned with federal and state requirements:

Strengthening healthcare safety net sustainability through financial and operational supports

Developing solutions for complex patient populations such as individuals who are justice-involved or have extensive behavioral needs including substance use disorder

Designing coverage strategies for critical social needs, such as community reintegration of vulnerable populations such as the justice involved, including when these require collaboration with agencies and programs beyond Medicaid

Supporting states in meaningful stakeholder engagement efforts, provider training and guidance, and other activities necessary for successful program implementation

Working with managed care organizations, health plans, providers, and other stakeholders to apply our expertise in implementing 1115 demonstrations

HOW HMA CAN HELP

Providing strategic and operational support to design demonstration programs With several former state Medicaid directors and former CMS officials on staff, HMA helps states design successful new interventions to address the unique needs of their populations and ensures proposals meet CMS’ approval requirements and expectations, including aligning 1115 interventions with evolving federal priorities and objectives for the program. With HMA, states and stakeholders gain valuable insights on strategic engagement and partnerships.

Developing applications for 1115 demonstration proposals HMA has supported a variety of 1115 initiatives in several states, including developing proposals for new, continuing, and amended 1115 demonstration programs. HMA consultants bring decades of experience in 1115 program design that covers all of the components critical to developing and operating 1115 programs – policy, actuarial and budgeting, operations, communications, project management, and IT.

Supporting federal negotiations for approval of state 1115 demonstration proposals HMA helps states navigate the federal processes to secure approval for their 1115 initiatives. In many cases, HMA joins in active negotiations with the state agency to support federal negotiations. HMA has unique insight into federal approval parameters with former CMS officials.

Operational Support We help stakeholders—including state agencies and their partners—manage the challenges of implementing new Medicaid or CHIP initiatives, with a focus on ensuring efficient integration and improvements in outcomes.

Evaluation and Assessment of section 1115 demonstrations Federal regulations require evaluation of CMS-approved 1115 programs. HMA designs and conducts evaluation reports that meet federal requirements, such as hypotheses, data sources, and comparison strategies. HMA’s work on evaluation designs and evaluation reports has been held out by CMS as best practice models to other states for evaluating new policy interventions as well as for ongoing monitoring activities.

Developing materials for and supporting stakeholder engagement from design to implementation. HMA works closely with states and their partners to engage stakeholders early in the 1115 process to ensure that communities and local organizations are involved in the planning and implementation of 1115 programs.

Project Spotlights

HMA has supported approved section 1115 demonstration programs testing new strategies for addressing substance use disorder (SUD), serious mental illness (SMI), and/or serious emotional disturbance (SED) through new flexibilities around the federal institution for mental disease (IMD) exclusion in seven states (Alabama, Colorado, Delaware, Indiana, Missouri, Ohio, and Oklahoma). In addition to initial and extension application support, HMA teams also support the evaluation and financial modeling components of 1115 demonstration development. In the last four years, we have delivered six evaluation designs, two midpoint progress assessments, two interim evaluations, and two summative evaluations approved by CMS. In general, HMA’s approved evaluation design plans use multiple evaluation methods, including a mixed-methods approach, drawing from various data sources, measures, and analytics, including quasi-experimental methods, to produce relevant and actionable study findings to conduct analyses. Additional 1115 demonstration program development activities include completing budget neutrality estimates and rate setting for new interventions proposed under demonstrations.

California is the first state in the nation to receive approval from CMS to provide detained and sentenced individuals with 90-day pre-release healthcare services and behavioral health linkages. HMA helps clients build administrative capacity, information technology, pre-release services, care management models, and Medicaid claiming infrastructure to meet their unique needs and leverage this significant state-federal demonstration opportunity. Our planning and implementation support spans the breadth of the CalAIM Justice-Involved Initiative including: the pre-release Medicaid application process, 90-day pre-release services, behavioral health links, Enhanced Care Management (ECM), and Community Supports services. In addition to California, HMA supported other states, such as Illinois and Maryland, with the design, approval, and/or implementation of justice-involved demonstrations approved by CMS. Learn more about CalAIM Justice-Involved Reentry Initiative Planning and Implementation Services.

HMA has supported multiple states in developing alternate approaches to Medicaid eligibility and enrollment tailored to their unique policy goals. For example, our consultants have worked with the Indiana Family and Social Services Administration on the program design, approval, and implementation of the Healthy Indiana Plan (HIP), Indiana’s alternative Medicaid expansion demonstration program. We also supported the Iowa Department of Health and Human services in developing the Iowa Health and Wellness Plan (IHAWP) 1115 demonstration which provides an alternative benefit design to traditional Medicaid expansion. HMA also supported the Kentucky Cabinet for Health & Family Services (CHFS) with a variety of services related to its section 1115 demonstration, Kentucky HEALTH, the first community engagement program in the nation approved by CMS.

Federal statute requires states to provide non-emergency medical transportation (NEMT) to Medicaid beneficiaries who have no other means of getting to medically necessary healthcare facilities. Though NEMT programs must meet certain federal requirements, states have considerable flexibility in the design and operation of their NEMT program. As a result, states vary widely in their NEMT procurement and contract standards, metrics, reporting, and enforcement of requirements for NEMT brokers, MCOs, and transportation providers. Health Management Associates, Inc. (HMA), examined NEMT-related requests for proposals (RFPs) and contracts for five states and interviewed state Medicaid officials, transportation brokers and providers, MCOs, advocates, and subject matter experts (SMEs). The goal was to synthesize the information gathered to help inform states and other stakeholders about key NEMT standards, challenges and successes, and considerations for developing RFPs and contracts.