HMA Insights: Your source for healthcare news, ideas and analysis.

HMA Insights – including our new podcast – puts the vast depth of HMA’s expertise at your fingertips, helping you stay informed about the latest healthcare trends and topics. Below, you can easily search based on your topic of interest to find useful information from our podcast, blogs, webinars, case studies, reports and more.

HMA partners with state, county, and local government entities nationwide to strategically allocate opioid settlement funds, driving impactful solutions for opioid use disorder (OUD) and overdose prevention. Through collaboration with policymakers, engaged stakeholders, and community members, we help clients develop funding priorities that enhance public health outcomes and improve quality of life. Our team has extensive experience working with counties across the U.S. to design and implement effective OUD programs. By fostering partnerships with clients, community advisory boards, and local organizations, we co-create community engagement strategies, tools, and plans that ensure meaningful participation in decision-making and sustainable program success.

We have a successful track record developing strategic expenditure plans for opioid abatement settlement funds that align with key funding priorities to drive measurable improvements in quality of life for individuals experiencing OUD and to implement effective overdose prevention initiatives.

How HMA can help

Community-Driven Fund Allocation – Effective use of opioid settlement funds depends on robust community engagement and feedback, ensuring investments align with local needs and priorities.

Expert Facilitation of Consensus Building – HMA’s unique ability to navigate complex community dynamics enables us to diffuse tensions, validate diverse perspectives, and drive stakeholder alignment for impactful decision-making.

Data-Backed Strategic Planning – Our comprehensive data collection and analysis identify persistent challenges, best practices, and targeted actions across the continuum of care (prevention, intervention, and treatment), culminating in a final report that informs sustainable solutions.

Elevating Community Voices – We prioritize the insights of individuals with lived experience, healthcare providers, and tribal partners to ensure funding priorities reflect the real needs of those affected by OUD.

Blueprint for Sustainable Impact – The expenditure plan serves as a strategic manual for the effective use of opioid settlement funds, integrating state requirements with community-driven priorities to maximize long-term success.

OUR EXPERTISE

With deep expertise in opioid settlement fund expenditure planning and a proven track record of success, HMA is uniquely positioned to help organizations nationwide design and implement effective OUD programs. Our team brings unparalleled experience in strategic planning, community engagement, and policy development, ensuring that funding is maximized for sustainable impact. We leverage strong partnerships and customized engagement strategies to drive data-driven, community-centered decision-making.

Charles Robbins has been transforming communities for the past three decades. His extensive community-based organization career spans healthcare, child welfare, … Read more

Increasing the Cultural and Linguistic Accessibility of Services

National Standards for Culturally and Linguistically Appropriate Services (CLAS) in Health and Healthcare frame how to improve healthcare quality and reduce disparities through a whole-person approach. Implementation of the CLAS standards demonstrates respect for individuals and responsiveness to their health needs, cultural beliefs and practices, preferred languages, and other communication needs. These standards guide the provision of high-quality care to people from all cultures and backgrounds, as well as persons with disabilities and rural populations. The 15 CLAS standards focus on governance, leadership, workforce, communication, language access, engagement, continuous improvement and accountability.

Quality

Provide services that are responsive to diverse backgrounds across the US

Equity

Reduce persistent health disparities experienced by racial, ethnic, linguistic, sexual, and gender minorities; persons with disabilities; and rural populations

Experiences of Care

Respect the whole individual and respond to the individual’s health needs and preferences

Cost

Reduce total cost of care by addressing health disparities

WHY CARE ABOUT CLAS?

In 2022, Forbes reported that health inequities cost the US health system $320 billion now and could reach $1 trillion by 2040

Our experts work with states, Certified Community Behavioral Health Clinics (CCBHC), behavioral health organizations, health systems and providers, health plans, and public health organizations to develop CLAS programs, assess gaps in the cultural and linguistic accessibility of services across a system, and provide tailored technical assistance and trainings. Adherence to CLAS standards is required by the Substance Abuse and Mental Health Services Administration (SAMHSA) for initiatives like the CCBHC model due to its positive impact on programming, outcomes, and disparity reduction.

Our CLAS Work

Indiana Statewide Evaluation of Community Mental Health Center (CMHC) CLAS Compliance

HMA completed a comprehensive assessment of Indiana’s 24 CMHCs to evaluate the strengths and needs regarding CLAS standards. We provided coaching, technical assistance, and webinars to support the CMHCs to set goals, build action plans, operationalize CLAS standards, and align CCBHC demonstration preparation and CLAS efforts.

Delaware Division of Substance Abuse and Mental Health (DSAMH) CLAS Training & Mini-Grants

HMA collaborated with DSAMH to develop a strategy to increase cultural responsiveness of substance use disorder (SUD) services. This included implementing a CLAS mini-grant program to provide technical assistance and training for SUD services. We developed and delivered a CLAS “train-the trainer” curriculum for staff, focusing on culturally and linguistically responsive opioid use disorder (OUD) services for African American and Latine communities. We also created a CLAS standards assessment to frame community-based organization and provider improvement strategies.

CCBHC Transformation Projects Across the Country

Disparity reduction is key to the CCBHC model. Nationally, the HMA CLAS team offers technical assistance to states on how to embed CLAS standards into planning grant and demonstration grant applications. For states that have been awarded CCBHC funding, we can provide training on how to incorporate CLAS standards and disparity reduction strategies into various aspects of their operations. These include community needs assessments, advisory boards, policies and procedures, staff training, program operations, state administrative codes, quality improvement and assurance initiatives, as well as data collection and analysis processes.

Our CLAS Approach

HMA’s team tailors its support based on each client’s needs. HMA takes the following general approach to assess and implement CLAS standards:

Assess CLAS standard gaps at organization, system or state level focused on the three CLAS domains: Governance, Leadership and Workforce; Communication and Language Assistance; and Engagement, Continuous Improvement and Accountability

Provide tailored technical assistance and coaching to close gaps drawing on our team’s cultural and linguistic diversity and lived experiences with services that are inaccessible to persons with disabilities, as well as persons from racial, ethnic, linguistic, cultural, sexual, and gender minority groups

Design and facilitate training and webinars to address wide scale gaps. Webinar topics may include – using Continuous Quality Improvement (CQI) processes to reduce disparities; increasing language access through translation and interpretation best practices; how to use community needs assessments to identify disparities; and structuring advisory boards for maximum impact

Assist programs and states in developing a CQI strategy to monitor and adjust initiatives to ensure CLAS and disparity reduction initiatives are making demonstrable change

Leticia Reyes-Nash is an accomplished, innovative executive leader with 20 years of experience leading policy advocacy, projects, and community engagement, … Read more

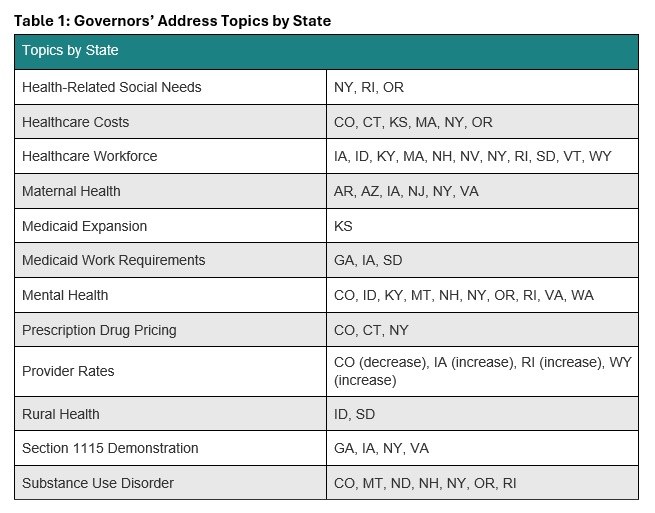

This week, our In Focus section examines governors’ healthcare priorities from their 2025 State of the State addresses. This article highlights common themes in addresses delivered between January 6, 2025, and January 16, 2025, and delves into specific proposals in Georgia, Iowa, New York, and Oregon, as analyzed in the Health Management Associates (HMA), Information Services (HMAIS) interim report, 2025 State of the State Overview.

State of the States in the Current Environment

Governors use their State of the State addresses to outline their priorities for the year, giving insight into the agendas and initiatives that their executive branches may pursue independently or in collaboration with their state legislature. These priorities often are informed by the status of the state’s budget, with some governors advancing healthcare proposals that will address budget deficits and others seeking to invest in services and workforce initiatives.

Monitoring governors’ policy priorities and initiatives is especially important in 2025 given the changing federal landscape. The transition in both the administration and Congress will require state leaders to carefully consider the risks and opportunities. As detailed below, governors’ responses will unfold differently across states and markets.

Common Threads

In all, 24 governors delivered a State of the State Address between January 6, 2025, and January 16, 2025. Many gubernatorial leaders have similar areas of priority and concern, with some continuing multiyear initiatives to address unmet behavioral health needs and control healthcare costs. Table 1 identifies the themes emerging from the first group of addresses.

Governors also are considering possible policy changes under the new Trump Administration. For example, some governors reported that their state is looking to strengthen or add Medicaid work requirements to their programs, resuming initiatives that were initially pursued during the first Trump Administration. Though not directly related to healthcare, governors’ decisions to mirror President Trump’s Department of Government Efficiency, with Iowa as an example, could indirectly affect local programs and markets. Other states are considering the implications of possible changes to federal Medicaid funding. A deeper look into the priorities in Georgia, Iowa, New York, and Oregon follows.

Georgia

Gov. Brian Kemp delivered Georgia’s State of the State address on January 16, 2025, during which he focused his healthcare remarks on the state’s Pathways to Coverage Section 1115 demonstration. Georgia’s waiver extends Medicaid coverage to able-bodied adults who earn up to the federal poverty level if they meet certain work requirements. The governor emphasized that he intends to work with the Trump Administration to further advance innovative approaches to healthcare access.

Governor Kemp stated that his administration is making it easier to apply for Medicaid coverage and will submit an amendment to the Centers for Medicare & Medicaid Services (CMS) that would extend the Pathways demonstration for five years beyond the current expiration date of September 30, 2025. The state plans to request several changes to the demonstration, including:

Changing the reporting requirements for qualified work activities

Adding more activities that qualify for program eligibility

Adding a retroactive coverage policy

Removing premiums and Member Reports Accounts

The governor’s proposed fiscal year (FY) 2026 budget includes $324 million to fully fund projected Medicaid enrollment and utilization growth and $36 million in additional support for pharmacy benefits, including recently approved gene therapy treatments for sickle cell disease.

Iowa

Iowa Gov. Kim Reynolds delivered the Condition of the State Address on January 14, 2025, during which she called for increased Medicaid reimbursement rates for OB/GYNs and primary care physicians who provide care to people with complex pregnancy cases, as well as certified nurse midwives. The governor also said she was in favor of adding doula services as a covered Medicaid benefit. Governor Reynolds is one of several governors who have announced plans to pursue a Section 1115 demonstration for Medicaid work requirements for able-bodied adults.

Governor Reynolds’s proposed FY 2026 budget includes investing $642,000 in newly unbundled Medicaid maternal rates, and more than double investments in five existing state healthcare loan repayment programs. The governor also proposes to establish a Medicaid Graduate Medical Education enhanced payment to draw down more than $150 million in federal dollars for more residency spots in Iowa’s teaching hospitals.

New York

New York Gov. Kathy Hochul delivered her State of the State Address on January 14, 2025, at which time she also released a State of the State Book. Addressing behavioral health is one of her chief priorities, and proposals include:

Allowing more involuntary commitments for people with severe mental illness

Developing programs to support youth mental health through after school programs

Expanding peer support programs

Improving the diagnostic process for children with complex needs

Supporting mental wellness in historically marginalized neighborhoods

Expanding Mobile Medication Units to bring opioid treatments to underserved areas

Governor Hochul intends to expand support for the state’s healthcare safety net. This part of her agenda would provide financial assistance to struggling medical facilities and hospitals through expansion of the state’s Safety Net Transformation Program and participation in the US Food and Drug Administration’s program that allows states to import lower-cost drugs from Canada.

The governor’s proposed $252 billion budget for FY 2026 would allocate $35.4 billion for the state Health Department’s Medicaid budget—a 14 percent increase from last year. Governor Hochul plans to offset some of the spending hike with revenue from the newly approved managed care organization tax, which is expected to raise $3.7 billion to help balance the state budget over three years.

Oregon

Gov. Tina Kotek delivered Oregon’s 2025 State of the State Address on January 13, 2025. The governor has a significant focus on mental health and substance use disorder treatment, as well as housing as an HRSN. Governor Kotek wants to strengthen the behavioral health system and proposed adding new treatment beds, increasing treatment capacity, eliminating backlogs at the state’s health licensing boards to improve access to qualified counselors, improving the provider pipeline, and increasing worker retention. During her speech, the governor also called for improved frontend care coordination to decrease the overflow of people at the Oregon State Hospital.

In addition, the governor intends to work toward improving care for the civil commitment population (i.e., people who are involuntarily detained in a psychiatric hospital) by dedicating permanent supportive housing funds to expanded residences with onsite services. Governor Kotek has directed her team to develop a new intensive permanent supportive housing model to more effectively support people with serious mental health needs.

Governor Kotek’s proposed budget for the 2025−2027 biennium includes $39.6 billion for the Oregon Health Authority, representing a 10.4 percent increase from the approved budget for 2023−2025. This budget includes $29.6 billion for the state Medicaid program and $1.6 billion for the Behavioral Health Division, in addition to $732.4 million for the division from the General Fund.

Connect With Us

HMAIS has prepared a comprehensive report summarizing each State of the State Address, which is available to HMAIS subscribers. The report also examines proposed budgets, highlighting key financial commitments and allocations that underscore these priorities for the upcoming year. The first iteration of the report covers AR, AZ, CO, CT, GA, IA, ID, KS, KY, MA, MT, ND, NE, NH, NJ, NV, NY, OR, RI, SD, VA, VT, WA, and WY. The document will be updated periodically as speeches occur.

Contact our experts below for more information about the report or to connect with one of HMA’s state policy and market experts.

During this webinar, attendees heard from experts on the details regarding new Health Related Social Needs (HRSN) services available through New York Medicaid. The discussion focused on how these services can be implemented successfully and considerations for organizations around funding, compliance, and service alignment. A panel of experts representing social care networks (SCN), community-based organizations (CBO), and funders shared their perspectives on the opportunities and challenges created by these new services.

Learning Objectives:

Understand the details that will support the integration of new Medicaid services into current organizational offerings

Learn how new Medicaid services can support current mission and funding needs

Understand operational and funding considerations for implementing new services

Hear from experts in the field who will share their perspective on opportunities, strategies, and considerations for CBOs considering new HRSN services

For just the third time in the company’s 37-year history, Lovell Communications, an HMA Company, has a new chief executive officer, Amanda Maynord.

Amanda joined Lovell in 2013 and quickly proved herself to be a keen strategist and expert crisis communicator. She became a vice president at the firm in 2022 and has led its Transaction and Crisis practice since that time, helping clients navigate complex healthcare issues such as high-profile mergers and acquisitions, regulatory and criminal investigations, management crises and other reputation-threatening medical, financial and environmental events.

Amanda is not only a skilled communicator and keen strategist, she’s a versatile consultant clients, as well as colleagues, trust and seek out again and again. She has worked in every aspect of operations at Lovell and has been a champion of integration into Health Management Associates (HMA) over the last two years. She is the ideal leader to move the team into the future.

As Amanda takes the helm at Lovell, Rosemary Plorin moves into the role of strategic advisor with HMA.

The year ahead promises challenges both new and old, and Lovell’s team of healthcare strategists look forward to helping clients across the country build and grow their organizations with strategic messaging, marketing and public relations.

This week, our In Focus section highlights how the new Administration and Congress are poised to significantly change healthcare policies, ranging from health equity and Affordable Care Act (ACA) Marketplace subsidies to Medicaid services and prescription drug costs. Stakeholders seeking to influence these potential changes should plan to engage quickly. Today’s section covers important developments that occurred through 2 pm January 29, and healthcare stakeholders will need to remain attune to future developments impacting federal healthcare programs.

Executive Action

Over the first week of his second term, President Donald J. Trump has issued several executive orders (EOs) and presidential directives affecting healthcare stakeholders. Presidents have increasingly used EOs at the beginning of their administration to rescind policies of their predecessors and direct the federal departments and agencies to exercise their authorities in line with the president’s directives.

Though some EOs require no further action, many are just the beginning of the policymaking process, with agencies tasked with implementing the directives. This timeline can provide stakeholders with opportunities to work with to policymakers to inform how they shape the rules for compliance with these directives.

Initial EOs issued so far by President Trump include policies that:

Executive Order 13985 of January 20, 2021, Advancing Racial Equity and Support for Underserved Communities Through the Federal Government

Executive Order 13988 of January 20, 2021, Preventing and Combating Discrimination on the Basis of Gender Identity or Sexual Orientation

Executive Order 13990 of January 20, 2021, Protecting Public Health and the Environment and Restoring Science to Tackle the Climate Crisis

Executive Order 14009 of January 28, 2021, Strengthening Medicaid and the Affordable Care Act

Executive Order 14070 of April 5, 2022, Continuing to Strengthen Americans’ Access to Affordable, Quality Health Coverage

Executive Order 14075 of June 15, 2022, Advancing Equality for Lesbian, Gay, Bisexual, Transgender, Queer, and Intersex Individuals

Executive Order 14087, of October 19, 2022, Lowering Prescription Drug Costs for Americans

Direct the Office of Management and Budget (OMB), the Attorney General, and Office of Personnel Management (OPM) to “coordinate the termination of all discriminatory programs,” including diversity, equity, and inclusion (DEI) programs, policies, and activities in the federal government.

Combat “illegal private-sector diversity, equity, and inclusion (DEI) preferences, mandates, policies, programs, and activities.”

Freeze federal rulemaking until department heads appointed or designated by the president can review and approve the rules and withdraw rules that have been sent to but not yet published in the Federal Register so they can be reviewed.

Establish and implement the Department of Government Efficiency (DOGE) as a temporary organization within the Executive Office of the President that reports to the White House Chief of Staff. Executive agencies are directed to establish DOGE teams of at least four employees. DOGE is intended to modernize Federal technology and software to maximize governmental efficiency and productivity.

Require OMB, OPM, and DOGE to submit a plan within 90 days to reduce the size of the federal government’s workforce through efficiency improvements and attrition.

Developments on the Federal Funding Pause

Notably, the White House OMB issued a memo (Temporary Pause of Agency Grant, Loan, and Other Financial Assistance Programs) on January 27, 2025, to all agencies with instructions to temporarily pause and provide a comprehensive analysis of all activities related to obligation or disbursement of federal financial assistance programs that EOs may affect. On January 29, 2025, the administration retracted the directive for a temporary pause on federal payments, though reiterated it will continue to review federal funding.

Though it is customary for a new administration to pause communications, regulatory activity, and new funding opportunities as incoming political appointees are confirmed and policy agendas are solidified, the breadth of the federal funding pause exceeds prior orders. The first lawsuit was filed on January 28, and a federal judge for the US District Court for the District of Columbia quickly issued a temporary stay on the federal funding pause until at least February 3, 2025, while she considers arguments in the case.

The now-rescinded January 27 memo was scheduled to take effect at 5:00 pm ET on January 28, 2025, to give the Trump Administration “time to review agency programs and determine the best uses of the funding for those programs consistent with the law and the President’s priorities.” According to the memo, the pause did not apply to Medicare or Social Security payments. In a subsequent document, OMB further clarified that “mandatory programs like Medicaid and SNAP [the Supplemental Nutrition Assistance Program] will continue without pause.”

What to Watch: Executive Actions and Budget Reconciliation

The Trump Administration has indicated that federal programs and funding should be aligned with his administration’s priorities. Healthcare stakeholders should be prepared for additional scrutiny of future funding awards.

Meanwhile, congressional Republicans are preparing to quickly leverage the budget reconciliation process to pass legislation related to several priority areas, including taxes, immigration, and domestic energy production (see Spotlight on Congress: Budget Reconciliation Update). Budget reconciliation provides a rare opportunity to pass significant healthcare legislative changes on a party-line basis. House Republicans have begun to develop their menu of healthcare options, which range from changes to the ACA premium tax credit structure, expanding Health Savings Accounts, and changes in Medicaid financing and eligibility.

In a January 2025 webinar, experts from Leavitt Partners, an HMA company, Liz Wroe, Sara Singleton, and Laura Pence discussed the potential health policy priorities of the Trump Administration, the implications of reconciliation for healthcare stakeholders, and the challenges and opportunities presented while navigating this expedited process.

Navigating Change

HMA experts are working with federally funded entities to quickly analyze their federal awards and plan for the next phase of federal agency actions and oversight. HMA companies also help healthcare stakeholders seeking to inform, shape, prepare for, and implement federal policy changes. Organizations seeking to influence the outcome of these policy debates and to thrive in a dynamic legislative and regulatory environment must have the most up-to-date information, informed by partners that understand the processes and the underlying policies under consideration.

HMA experts provide additional complementary services, including analyses to predict how the Congressional Budget Office will score the costs or savings of specific policies. Especially in the reconciliation environment, the budgetary impact of particular policies can significantly influence their likelihood of passage.

Connect with Us

To learn more about the these policy changes and the impact on your organization, watch our January 2025 policy webinar and contact one of our featured experts below.

As the Trump Administration takes office and a new Congress is convened, the legislative tool of budget reconciliation could play a pivotal role in shaping the nation’s policy landscape. In this webinar, Liz Wroe, Sara Singleton, and Laura Pence discussed the potential health policy priorities of the new Administration, the implications of reconciliation for healthcare stakeholders, and the challenges and opportunities presented while navigating this expedited process.

On January 6, The Centers for Medicare & Medicaid Services (CMS) approved Medicaid State Plan Amendment (SPA) #23-0010. The SPA authorizes the California Department of Health Care Services Service (DHCS) to use an alternative payment methodology (APM) to pay Federally Qualified Health Centers (FQHC), Rural Health Clinics (RHC), and Tribal Health Programs at the Medi-Cal fee-for-service (FFS) rate for dyadic services. FQHCs and RHCs will receive a separate payment for dyadic services in addition to their standard prospective payment system (PPS)/all-inclusive payment rates in certain circumstances. This SPA is retroactively effective to March 15, 2023.

Key provisions are as follows:

California’s new set of dyadic benefits supports relationship-based caregiver and family surveillance and family-based interventions that bolster child development, recognizing the importance of the parent/caregiver and child dyad to support healthy child development. Dyadic health care services are ideally provided in the context of routine well child care in pediatric settings, meeting families where they regularly receive health care and related services.

Services are linked to a child’s Medi-Cal coverage, providing a basis for revenue recovery for primary care pediatric settings and for cases in which the parent/caregiver may not be a Medi-Cal beneficiary.

Services are exempt from the same day exclusion applied to FQHCand RHC settings. If FQHCs or RHCs have met their visit per day limit, then dyadic services provided to Medi-Cal-eligible members (children or parents/caregivers) will be reimbursed at the FFS rate. Any dyadic services that are provided to a non-Medi-Cal-eligible parents/caregivers for the direct benefit of Medi-Cal-eligible children will be reimbursed at the FFS rate.

Payment for dyadic FQHC and RHC services will be reimbursed at the applicable FFS rate in addition to Medi-Cal member visits, which are reimbursed at the applicable PPS rate.

In addition, the dyadic care benefit provides a pathway for families to access additional supports via the new family therapy benefit. Family therapy is a psychotherapy service that managed care plans provide under Medi-Cal’s Non-Specialty Mental Health Services benefits. Family therapy services support members younger than age 21 to receive up to five family therapy sessions before a mental health diagnosis is required. More importantly, children and youth (younger than age 21) may receive family therapy without the five-visit limitation if they (or their parents/caregivers) demonstrate certain risk factors, including separation from a parent/caregiver because of incarceration, immigration status, or death; foster care placement; food insecurity; housing instability; exposure to domestic violence or trauma; maltreatment; severe/persistent bullying; and discrimination.

Health Management Associates (HMA) has been proud to partner with HealthySteps, as a DHCS-recognized model, to provide an evidence-based (APL 22-029 (ca.gov) approach to implementing the new dyadic care benefits. Contact our experts below to learn more.

With full Republican control, expect Congressional Republicans and the Trump Administration to quickly leverage the budget reconciliation process to pass legislation in several priority areas, including taxes, immigration, and domestic energy production. While expiring tax provisions may be the driving force of this year’s reconciliation efforts, Republicans are also likely to include other priorities, potentially including raising the debt ceiling, which will increase the need for reductions in mandatory health programs or changes to health care revenue to be used as offsets.

Budget reconciliation provides a rare opportunity to pass significant health care legislative changes on a party-line basis. However, while budget reconciliation has certain procedural advantages, it is also fraught with complex rules and procedures that can make it very difficult to pass large pieces of policy legislation intact.

Experts from Leavitt Partners, an HMA company, recently held a webinar reviewing the budget reconciliation process, opportunities and legislative strategies to navigate this process, and potential policies that could be considered. Access the webinar replay. Contact experts Elizabeth Wroe, Josh Trent, and Sara Singleton if you’re interested in learning more about the specialized services our team can offer your organization to navigate the Congressional budget reconciliation process and its outcomes.