July 16, 2025

HHS Issues Immediate Policy Shift on Federal Benefit Eligibility Under PRWORA

HMA Insights – including our new podcast – puts the vast depth of HMA’s expertise at your fingertips, helping you stay informed about the latest healthcare trends and topics. Below, you can easily search based on your topic of interest to find useful information from our podcast, blogs, webinars, case studies, reports and more.

HHS Issues Immediate Policy Shift on Federal Benefit Eligibility Under PRWORA

This literature review explores the concept of Food Is Medicine (FIM)—a healthcare approach that integrates nutrition-based interventions to prevent, manage, and treat chronic diseases. The report emphasizes the role of produce prescriptions, medically tailored meals (MTMs) and groceries in improving health outcomes, especially among low-income populations.

In the current policy environment, we anticipate increased consolidation in various subsectors due to financial and regulatory headwinds. Organizations can take intentional steps pre- and post-integration to realize cost synergies.

HMA Strategy & Transformation consultants advise organizations in their integration activities, and find it valuable to conduct the following sequence of steps:

Map the operating model pre-close to understand organizational structure, systems, contracts, and key processes across both entities.

Identify risks and quick wins before close—including staffing gaps, system incompatibilities, or duplicative vendors.

Design a Day 1 plan to keep operations stable, align communication, and ensure continuity for staff, patients, and partners.

Stand up integration teams post-close to drive workstreams across finance, IT, HR, and clinical operations with clear timelines and ownership.

Track synergies and milestones to measure progress, course-correct where needed, and deliver the operational and financial goals of the deal.

A thorough, objective mapping is recommended, to investigate whether to cultivate in-house capabilities or maintain vendor relationships. Considerations include in-house capacity, contracted rates, and the flexibilities and risks associated with outsourcing. We recommend identifying favorable terms in existing vendor contracts that can be leveraged in enterprise-wide contracts.

Although there are internal and external pressures to move aggressively towards transaction deadlines, ensuring that appropriate pre- and post-close activities take place is key.

Whether you are focused on payments, healthcare delivery, government policy, behavioral health, life sciences, Medicare, Medicaid, or Managed Care, our HMA experts are ready to partner with you, from initial strategy-setting through implementation.

Related Resources

Learn more about our Strategy & Transformation services

Achieving financial resilience in a time of turbulence

CMS Shakes Up the Innovation Center Model Landscape: What Comes Next?

Building Sustainable Health Systems

How One Organization Unlocked Exceptional Financial Gains Through Revenue Cycle Optimization

In November 2023, the Los Angeles (LA) County Board of Supervisors passed a motion to address the implementation of new benefits for the child welfare-involved population launched through California’s Medicaid waiver, California Advancing and Innovating Medi-Cal, known as CalAIM. The CalAIM waiver expanded services to managed care beneficiaries, including enhanced care management (ECM) for coordinated case management, referrals, and community resource navigation and community supports, such as housing assistance, medically tailored meals, housing modifications, respite care for caregivers, and asthma management. These benefits are designed to better address health and social needs for the most vulnerable and at risk Medi-Cal beneficiaries, including children and youth involved in the child welfare system. The Board directed the Office of Child Protection (OCP), in collaboration with key county departments, to engage Health Management Associates, Inc. (HMA), as the technical assistance provider.

Recognizing that approximately two-thirds of child welfare-involved children and youth in LA County are enrolled in fee-for-service (FFS) Medi-Cal and ineligible for new CalAIM supports, HMA conducted a comparative analysis of the experience of children involved in the child welfare system in FFS versus managed care Medi-Cal through an analysis of federal T-MSIS data looking at a snapshot of data from December 2022. The analysis examined the experience of the child welfare-involved population in primary and preventive healthcare services (including well-child visits, dental visits, behavioral health) in Medi-Cal FFS versus managed care plan enrollment (MCPs) to inform decisions about existing practices for care management among the child welfare-involved population. The comparative analysis of the child welfare population in Los Angeles County, San Diego County, and Riverside County revealed children in managed care consistently showed higher rates of engagement in primary and preventative healthcare services.

Just one week after we reviewed the Senate’s version of the budget reconciliation bill, H.R. 1, President Trump has now signed the legislation into law. The final iteration of H.R. 1 includes sweeping changes to Medicaid, the Affordable Care Act (ACA) Marketplaces, and Medicare—several of which diverge significantly from the version that the House passed May 22, 2025.

This update outlines many of the most consequential healthcare provisions, with a focus on Medicaid financing, eligibility, and operational impacts. It also highlights how stakeholders can act now to prepare for what happens next.

From Proposal to Policy: What Changed

The Senate’s amended version of H.R. 1, approved on July 1 and passed by the House on July 3, 2025, reshaped several key provisions in the earlier version of the House bill. Although the bill retains its core focus on tax policy and entitlement reforms, it further constrains state Medicaid financing and eligibility and scales back Marketplace subsidies for certain populations.

According to preliminary analysis from the Congressional Budget Office, the final bill will reduce federal healthcare spending by approximately $1.15 trillion over the next decade but also will increase the number of uninsured individuals by 11.8 million by 2034 because of changes to both Medicaid and Marketplace programs.

Medicaid Eligibility: A New Era of Policy and Operational Complexity

Mandatory Community Engagement Requirements

By December 31, 2026, states must implement community engagement (work) requirements for certain Medicaid enrollees. These requirements cannot be waived under Section 1115, though states may request “good faith” exemptions through 2028.

States must notify enrollees through multiple channels and develop the infrastructure needed to track compliance. Managed care organizations and other entities that have financial relationships with Medicaid services are prohibited from determining compliance.

Tighter Eligibility and Redetermination Requirements

States must now conduct Medicaid eligibility redeterminations every six months for expansion populations. The bill also delays implementation of previously finalized rules that would have streamlined enrollment and imposes new verification requirements, including address checks. For immigrants, H.R. 1 narrows the definition of “qualified” individuals who are eligible for Medicaid and CHIP, removing coverage for refugees, asylees, and other humanitarian categories.

Cost Sharing for Expansion Adults

Starting in 2028, states must apply cost-sharing requirements to Medicaid expansion adults with incomes greater than 100 percent of the federal poverty level. Though primary care, mental health, and certain other services are exempt, the policy introduces new administrative burdens for states and many providers.

Medicaid Financing: A Structural Shift

Provider Tax Restrictions

H.R. 1 freezes existing provider tax programs and bars any new taxes. Also, Medicaid expansion states must phase down the maximum allowable tax rate from 6 percent to 3.5 percent by 2032. This change will significantly constrain states’ ability to use provider taxes to finance Medicaid and draw down federal matching funds.

Limits on State-Directed Payments

The bill caps state-directed payments at either 100 percent or 110 percent of Medicare rates, depending on the state’s expansion status. Grandfathered payment arrangements will be phased down by 10 percent annually beginning in 2028. These provisions will require states to reassess supplemental payment strategies and may affect provider participation and access to care.

Other Key Provisions

The Rural Health Transformation Program provides $50 billion over five years to support financially distressed rural providers. H.R. 1 requires that each state submit a plan, and the Centers for Medicare & Medicaid Services (CMS) administrator must approve or deny the plan by December 31, 2025, giving CMS and the US Department of Health and Human Services significant authority to shape the approval/denial processes, as well as critical details of the program and funding decisions.

For the Marketplace, the law eliminates ACA subsidy eligibility for certain lawfully present immigrants, ends conditional eligibility for ACA subsidies as well as passive re-enrollment, and eliminates the cap on ACA subsidy repayment at tax time. It also prohibits individuals who are not enrolled in Medicaid because of a failure to satisfy community engagement requirements from receiving any subsidies.

In addition, a new 1915(c) waiver option allows states to offer home and community-based services (HCBS) without requiring that they provide institutional level of care but only if waiting lists for existing services are not extended. Another provision excludes family planning and abortion service providers from receiving Medicaid funding if they received at least $800,000 in Medicaid reimbursements in 2023.

Finally, the law includes a one-year, 2.5 percent increase to the Medicare physician fee schedule conversion factor, which will be in effect for calendar year 2026 and expire thereafter.

What Stakeholders Should Do Now

States can begin planning for eligibility system changes, redetermination volume, and community engagement implementation, all of which require an understanding of the potential interactions of the federal Medicaid, Medicare, and ACA Marketplace policy changes. In addition, state officials should consider reassessing provider tax structures and supplemental payment strategies, where applicable. They need to engage early on rural health transformation funding opportunities and other provider supports.

Health plans can forecast enrollment and risk mix changes. They have opportunities to support states in compliance efforts to avoid federal funding recoupments. In addition, plans must prepare for new administrative requirements related to cost sharing and work requirements, among other policy changes on the horizon. Consumer communications should also be a focus area.

Providers and community-based organizations will need to prepare for greater uncompensated care needs and costs, which can lead to potential revenue loss, as well as new reporting and program integrity expectations. They also will play an integral role in assisting patients in maintaining coverage and navigating new requirements.

Vendors and health information exchanges have several opportunities to support the implementation of new requirements in H.R. 1 alongside the changing regulatory priorities. Examples include reviewing system capabilities to support new eligibility, verification, and reporting requirements and coordinating with states to ensure smooth implementation and program integrity.

Looking Ahead

The passage of H.R. 1 marks a turning point in federal health policy. Although the law’s fiscal goals are clear, its operational impacts will unfold over the coming months and years. States, plans, providers, and community organizations must now pivot from policy analysis to implementation readiness.

HMA will continue to monitor federal guidance, state responses, and stakeholder strategies. For more detailed analysis or support with scenario planning, contact our experts below.

This week, our In Focus section highlights findings from the Centers for Medicare & Medicaid Services (CMS) preliminary CMS-64 Medicaid expenditure report for federal fiscal year (FFY) 2024. According to the preliminary estimates, Medicaid expenditures on medical services across all 50 states and six territories in FFY 2024 totaled $908.8 billion.

This figure provides important context and an initial baseline for tracking Medicaid spending trends following the enactment of H.R. 1, the One Big Beautiful Bill Act. According to the Congressional Budget Office’s preliminary analysis, H.R. 1 will reduce federal Medicaid and Children’s Health Insurance Program (CHIP) spending by approximately $1.02 trillion over the next decade (2025−2034)—a significant share of total Medicaid expenditures.

Total Medicaid Managed Care Spending

The following analysis is based on a Health Management Associates Information Services (HMAIS) analysis of the draft CMS-64 report. This report contains preliminary estimates of Medicaid spending by state for FFY 2024. CMS tracks state expenditures through the automated Medicaid Budget and Expenditure System/State Children’s Health Insurance Budget and Expenditure System (MBES/CBES). The CMS-64 form identifies annual expenditures through these systems.

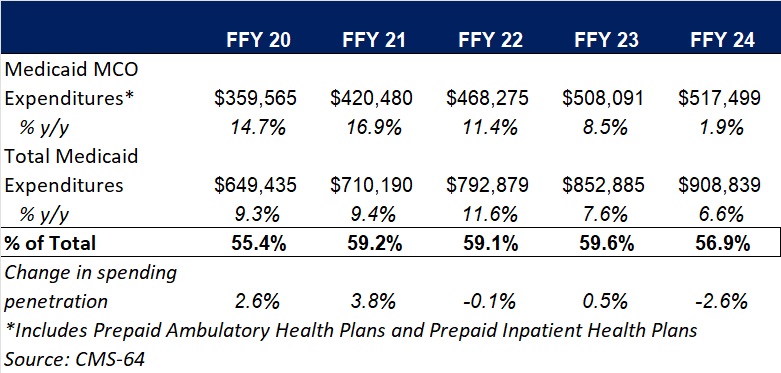

Key findings from HMAIS’ analysis, as also shown in Table 1, include:

These figures include spending on comprehensive risk-based managed care organizations (MCOs), prepaid inpatient health plans (PIHPs), and prepaid ambulatory health plans (PAHPs). PIHPs and PAHPs refer to prepaid health plans that provide only certain services, such as dental or behavioral health care. Fee-based programs, such as primary care case management models, are not included in this total.

Table 1. Medicaid MCO Expenditures as a Percentage of Total Medicaid Expenditures, FFY 2020−2024 ($M)

Medicaid Managed Care Spending Insights

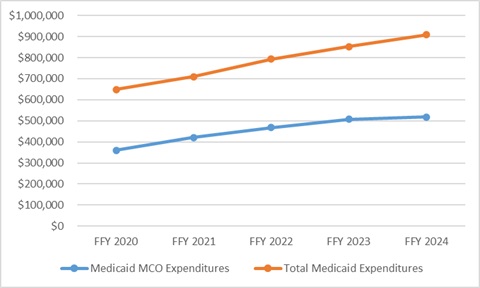

Medicaid managed care expenditures have grown consistently each year with total Medicaid expenditures. In FFY 2024, however, the growth in the share of managed care expenditures was notably lower than in the previous four years. The slower growth in managed care spending aligns with the post-COVID-19 policy unwinding period, during which many states completed eligibility redeterminations that had been paused during the public health emergency, driving historic enrollment increases (see Figure 1).

Figure 1. Total and MCO Medicaid Expenditures, FFY 2020−2024 ($M)

In addition, Health Management Associates (HMA) has access to data in the Transformed Medicaid Statistical Information System (T-MSIS) and has analyzed MCO spending in major categories of healthcare, including inpatient and outpatient hospital care, physician and other professional services, skilled nursing facilities (SNFs) and home and community-based services (HCBS), clinics, pharmaceuticals, and other services. Similarly, based on the CMS-64 data, in FFY 2024, the largest non-managed care spending categories included:

HMA’s analysis of the T-MSIS database shows that while managed care remains the dominant delivery system model for Medicaid, spending in certain categories, such as SNFs and professional services, is growing faster. This shift may explain the declining share of managed care in overall Medicaid expenditures, even as absolute spending remains high. Further details can be found on this webpage and this webpage as well.

Federal Versus State Spending

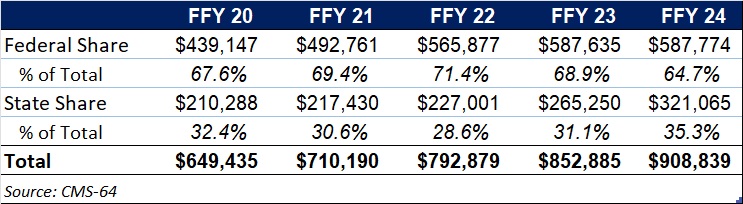

This year’s data reflect the phase-out of the temporary 6.2 percentage-point federal medical assistance percent increase under the Families First Coronavirus Response Act, which ended December 31, 2023. In FFY 2024, 64.7 percent of FFY 2024 spending came from federal sources (see Table 2).

Table 2. Federal versus State Share of Medicaid Expenditures, FFY 2020−2024 ($M)

What to Watch

Looking ahead, state Medicaid agencies will need to reassess financing strategies as total Medicaid federal funding declines because of H.R. 1 and other federal regulatory oversight and policy changes take effect. H.R. 1 includes provisions to gradually reduce allowable state provider tax rates from 6 percent to 3.5 percent by 2032, potentially requiring states to restructure financing or identify cost-saving measures.

CBO projections estimate that the Medicaid provisions in the bill will increase the number of uninsured individuals by an estimated 7.8 million by 2034.

Connect with Us

HMAIS, a subscription-based tool offered by HMA, provides detailed state by state analysis of the CMS-64 data and Medicaid managed care enrollment trends. For more information about the HMAIS subscription and access to the CMS-64 data, contact our experts below.

Healthcare business leaders face significant policy and regulatory headwinds. Ensuring that your organization is financially resilient to weather the storm should be a priority. Achieving financial resilience enables leaders to preserve core functions and staff. We’ve found that indirect costs are often overlooked and undermanaged and represent an opportunity to build margin (think overhead and administrative costs such as vendor spend).

We find it useful to conduct the following sequence of steps:

Review / categorize all vendor spend to find areas with unnecessary costs, overlapping services, or outdated pricing.

Analyze contracts line -by -line to identify where terms can be improved or where the scope no longer fits current needs.

Stack rank initiatives by risk levels and speed.

Negotiate directly with vendors to lower rates, adjust service levels, or consolidate under better pricing structures.

Monitor results and vendor performance to ensure savings hold over time and services stay aligned with operational needs.

In assessing indirect costs, we visually depict areas of cost reduction by risk of disruption to support client decision-making. There is often a locus of opportunity that can be trimmed with little or no impact to the core business.

As you prepare to batten the hatches, consider assessing indirect costs. Even if the storm isn’t fierce, conducting this work will give you improved real options for optimal decision-making.

Whether you are focused on payments, healthcare delivery, government policy, behavioral health, life sciences, Medicare, Medicaid, or Managed Care, our HMA experts are ready to partner with you, from initial strategy-setting through implementation.

Related Resources

Learn more about our Strategy & Transformation services

CMS Shakes Up the Innovation Center Model Landscape: What Comes Next?

Building Sustainable Health Systems

How One Organization Unlocked Exceptional Financial Gains Through Revenue Cycle Optimization

This webinar was July 22, 2025.

This is a powerful and practical town hall designed to inform Georgia’s community-based organizations (CBOs) with the knowledge to access new funding opportunities through the new community reinvestment requirements in Georgia Medicaid. Learn how HMA can help you to build strategic partnerships with managed care organizations (MCOs) to support your mission—and position your organization for success amid upcoming federal Medicaid work requirements.

Learning Ojectives:

Featured Speaker:

Lynnette Rhodes, Chief Health Policy Officer Georgia Department of Community Health

Since January 1, 2025, State of Reform (SOR), an HMA Company, has hosted eight conferences across states. SOR conferences give providers, health plans, lawmakers, and other stakeholders from all areas of healthcare the opportunity to have real-time discussions about pressing healthcare issues. These events provide a forum to bring together leaders with different perspectives and areas of expertise to discuss, digest, and synthesize issues and challenges at the state and local levels. These discussions allow states and their partners to improve healthcare delivery and prepare for changes before they happen.

This article explores common themes and issues addressed during the state-specific meetings.

Common Trends and State Priorities

Although each state has unique challenges and priorities, there is clear overlap in the issues being addressed. The exchange of ideas and best practices at these meetings is fostering a collaborative approach to tackling some of the most pressing challenges facing our nation today. Key themes include:

The conferences also provided a platform to discuss a range of other healthcare and health-related issues. Payment reform was a hot topic, with states exploring ways to make healthcare more affordable and efficient. Attendees were engaged in discussions about the impact of the federal Medicaid policy changes to coverage for health-related social needs (HRSNs), and the importance of community level strategies to address factors like housing, food security, and transportation. Maternal healthcare, the reentry population, the aging population, and rural health were other significant topics, each contextualized by the state-specific challenges and innovative solutions being explored.

What to Watch

The federal health policy landscape will continue to change over the coming months, which will greatly affect how states approach healthcare, especially Medicaid services. The policy changes and the downstream implications for state and local governments and their partners will be at the heart of discussions at the upcoming Health Management Associates (HMA) National Conference, Adapting for Success in a Changing Healthcare Landscape, and State of Reform conferences. Key topics include:

Connect with Us

Join a range of healthcare stakeholders, including HMA experts, at one of the upcoming State of Reform conferences. These events provide a unique opportunity to delve into state and local-specific discussions, allowing for a deeper understanding of regional healthcare challenges and solutions.

We also invite you to continue these important conversations at the national level at HMA’s 2025 conference, Adapting for Success in a Changing Healthcare Landscape, which will take place October 14−16 in New Orleans, LA. This conference will focus on both state and federal issues, fostering collaboration and learning among state and federal agencies, payers, health systems, providers, and other key stakeholders.

For more information on the HMA conference, contact Andrea Maresca. For more information on State of Reform, contact SOR program director Katharine Weiss.

On July 1, 2025, the US Senate voted 51–50, to advance its version of H.R. 1, continuing the budget reconciliation process. Like the bill that the House passed in May, the Senate language calls for making significant changes to the Medicare, Medicaid, Affordable Care Act (ACA) Marketplace programs, as well as health savings accounts (HSAs) and publicly funded programs such as the Supplemental Nutrition Assistance Program.

Relative to the House bill, however, the Senate differs substantially in approach and scope. Thus, the bill has been sent back to the House for consideration. Speaker of the House Mike Johnson (R-LA) intends to accelerate voting with the goal of clearing the legislation in the House by July 4, 2025.

Key Differences Between House and Senate Bills

Notable differences between the House and Senate packages pertain to the following:

Estimates from the Congressional Budget Office

The Congressional Budget Office (CBO) has provided several estimates of the cost and coverage impacts of the healthcare and tax provisions in multiple versions of the reconciliation legislation. CBO has provided cost estimates for the House-passed bill, as well as the Senate substitute amendment, but has yet to release information on the final Senate version. Of note, CBO estimated the following:

What to Watch

Stakeholders should plan for the financial, policy, and operational impacts of the many provisions that could be enacted, including:

The combination of the House and Senate reconciliation bills and the recently finalized Marketplace Program Integrity and Affordability rule indicate an uncertain future for cost sharing subsides and enhanced premium tax credits in Marketplace programs. Healthcare stakeholders should prepare for the impact of the expiration of the enhanced premium tax credits would have on benefit packages, enrollee risk profiles, uncompensated care, and other key issues affecting access, cost, and outcomes.

Connect with Us

To learn more about the these policy changes and the impact on your organization, contact our featured experts below.