January 28, 2026

CMS Releases 2027 Advance Notice with Medicare Advantage and Part D Rates

HMA Insights – including our new podcast – puts the vast depth of HMA’s expertise at your fingertips, helping you stay informed about the latest healthcare trends and topics. Below, you can easily search based on your topic of interest to find useful information from our podcast, blogs, webinars, case studies, reports and more.

CMS Releases 2027 Advance Notice with Medicare Advantage and Part D Rates

As of January 1, 2026, nine governors had released proposed budgets for state fiscal year (SFY) 2027. With the phase down of federal funding and substantial policy changes approved in the 2025 budget reconciliation act (P.L. 119-21, OBBBA), these proposals offer insights into how governors plan to manage mounting fiscal pressures, navigate new federal mandates, and position their programs for long-term sustainability.

Today, Health Management Associates Information Services (HMAIS) published its first preliminary review of proposed SFY 2027 budget proposals. The initial installment includes budgets from Alaska, Colorado, Florida, Mississippi, New Mexico, South Dakota, Utah, Virginia, and Wyoming, with the latter two proposals covering the fiscal 2026–28 biennium.

HMAIS will release periodic updates as additional governors publish their budget proposals—the same rolling approach we used in 2025 (here and here). Because 15 states enacted 2025–27 biennial budgets last year, HMAIS also might review substantial mid-biennium health-related adjustments or supplemental funding.

The remainder of this article provides a snapshot of several notable themes and emerging trends detailed in the full report.

Implementation of New Federal Requirements

State leaders are preparing budgets for SFY 2027 at a time of heightened fiscal stress and structural uncertainty. Entering 2026, governors are facing reductions in federal funding, particularly in Medicaid and Supplemental Nutrition Assistance Program (SNAP) funding. In addition, they are preparing for new federal requirements that will begin to take effect later this year, including narrower flexibilities for financing and Medicaid community engagement policies and more frequent eligibility redeterminations.

Against this backdrop, governors are using FY 2027 budget proposals to comply with OBBBA’s mandates and to stabilize their safety net programs and realign state operations around stricter fiscal realities.

Medicaid Work Requirements. Virginia’s proposed budget includes funding to implement federal Medicaid community engagement requirements, including a recommendation to add nine new authorized positions in SFY 2027 and 12 more in fiscal year 2028 to meet workload demands. In addition, South Dakota’s governor proposed amending the state’s 2026 budget to secure funding to implement these requirements.

Eligibility and Redetermination. Several governors are proposing investments to support heightened eligibility checks across Medicaid, SNAP, and Temporary Assistance for Needy Families (TANF). For example, Colorado Gov. Jared Polis’s budget proposes $19.1 million to improve the state’s eligibility system for programs such as Medicaid, SNAP, and TANF. Utah’s proposed budget includes a recommended allocation of nearly $16.5 million to the Department of Workforce Services for “H.R. 1 Medicaid Eligibility Administration,” and nearly $10 million for the “H.R. 1 SNAP Administrative Services.”

SNAP Changes. States are backfilling lost federal funding and investing in error reduction and system modernization. New Mexico Gov. Michelle Lujan Grisham’s proposed budget, for example, includes $37 million to replace the decrease in federal funding for SNAP administration ($4 million of which will support 150 new full-time positions), as well as $8.9 million for systems improvements to reduce payment errors in SNAP. South Dakota Gov. Larry Rhoden’s proposed budget includes $5.5 million to offset a reduction in SNAP federal funding.

Strategic Cost Containment

Considering OBBBA implementation and the effects that it will have on their budgets, our first review of governors’ budget proposals signals that states are taking an aggressive posture toward limiting expenditure growth in 2026 and 2027. Initial proposals include targeted reductions, tighter utilization management, and restrictions on benefits.

Since the 2025 legislative session, Colorado has taken multiple steps to prepare for declining federal revenue. For example, Governor Polis’s proposed budget accounts for multiple actions approved through an amended executive order that would reduce spending to brace for OBBBA’s impacts. Examples include:

Former Virginia Gov. Glenn Youngkin’s budget—now inherited by Abilgail Spanberger following her inauguration January 17, 2026—includes multiple cost-containment proposals, such as:

States are expected to include additional cost-containment tools throughout 2026 and beyond as OBBBA’s fiscal effects become clearer over the coming months and years.

What to Watch

The budget proposals indicate the resources that executive agencies need and preview governors’ policy agendas for the year ahead. Stakeholders should track program reductions and rate changes, eligibility system investments, and shifts in care models.

In addition, some of the announced budget proposals consider federal awards to states under the Rural Health Transformation Program (RHTP). For example, the Alaska Department of Health budget request addresses the state’s RHTP implementation plans, and Wyoming’s budget proposal outlines RHTP priorities. Many states are preparing RFP processes to operationalize their RHTP strategies and make progress on the goals of their initiatives.

Connect with Us

As federal funding uncertainties continue, states and other stakeholders will need to adapt their delivery systems, administrative structures, and financing models throughout OBBBA’s multiyear rollout. HMA offers expertise, analytics, and strategic advisory services needed to navigate this evolving landscape. For details contact Andrea Maresca and Kathleen Nolan.

The full state of the states and governor budget report is available to HMAIS subscribers. In addition, HMAIS maintains a Rural Health Transformation Program (RHTP) Tracker that incorporates details of each initiative and the first year award.

As the 2026 Affordable Care Act (ACA) Marketplace open enrollment period nears its close—and with enhanced subsidies expiring, rates shifting, and consumer behavior evolving—questions about enrollment stability, affordability, and operational readiness have rapidly moved to the forefront. Andrea Maresca, Senior Principal, at Health Management Associates, caught up with Zach Sherman, Managing Director for Coverage Policy and Program Design at HMA, and Michael Cohen, PhD, who leads much of the federal policy analysis advanced by Wakely, an HMA company, to unpack what they’re seeing so far.

Q: This year’s open enrollment period has been unusually complex. At the federal level, what stands out most so far?

Michael: The headline is that new enrollment is down sharply, while returning consumers have held steadier than expected. That reflects the reality that the enhanced subsidies are gone, premiums have risen, and consumers are facing higher net costs across nearly every market.

But nuance matters: The real question now is how many of these plan selections will effectuate—meaning consumers pay their first month premium, and how many will stay enrolled the entire year? Average effectuated enrollment throughout the year is what truly determines 2026 risk mix and market stability.

Q: Enrollment appears to vary considerably from state to state. What are you hearing from state partners?

Zach: It’s a tale of two markets. StateBased Exchanges (SBEs) are generally seeing less attrition and, in some cases, even modest increases in plan selections. The reason is simple: Many states are doing a lot of heavy lifting to offset the loss of federal support.

For example, SBEs perform earlier and have more customized outreach. We’ve also seen some states step in and offer state-funded subsidies, which are cushioning the affordability loss in places like New Mexico, Maryland, and California.

While still early, the data suggest that states with heavy investment in awareness and enrollment assistance, operational support, and affordability are weathering the transition better because they have more tools to stabilize the consumer experience.

Q: There’s been a lot of speculation about how consumers are responding to the end of enhanced subsidies. What are the early signs?

Michael: Consumers appear to be buying leaner benefits or different metal tiers to manage premium increases.

Another underrecognized but incredibly important dynamic is that autoreenrolled consumers may not effectuate coverage once they see the final outofpocket premium. That dynamic won’t be fully understood until March, April, and even May.

Q: Idaho is a particularly interesting early case study. What are you learning from the first state to complete enrollment?

Zach: Your Health Idaho’s open enrollment finished on December 15, and while they saw a slight increase in plan selections, state officials are not celebrating as they expect a large wave of cancellations—up to 20,000—due to the expiring subsidies.

That’s the clearest early indication that affordability is the defining issue of 2026. States are preparing for higher-than-usual enrollment attrition in quarters one and two (Q1 and Q2), and they’re thinking hard about customer service capacity as consumers navigate changing net premiums, increased deductibles and out-of-pocket costs, and nonpayment grace periods.

Q: Are there policy levers states can still pull to mitigate affordability challenges going forward?

Zach: We’re seeing states explore options for mitigating affordability gaps and enrollment losses, including through state subsidy programs and increased investment in existing reinsurance programs. SBEs are also leaning on their core competencies—tailored and specific education campaigns and enrollment and plan comparison tools—to help their customers cut through the noise and navigate to the best option within their budget.

These aren’t perfect or quick fixes and most states don’t have the resources necessary to backstop the expiring subsidies, but state leaders increasingly view doing something as necessary to stabilize their markets.

Q: What should health plans, exchanges, and policymakers watch most closely over the next three months?

Michael: Effectuation, effectuation, effectuation. The composition of the effectuated population will define 2026 risk.

Zach: Agree. In addition, future regulatory action on affordability, eligibility and enrollment processes, and program integrity. The federal government is expected to issue its annual payment notice, the proposed 2027 Notice of Benefits and Payment Parameters, in the near future.

You can find more insights on the initial enrollment patterns to date in this Health Management Associates-Wakely paper, Individual ACA Open Enrollment Insights So Far and register for the 2027 ACA Considerations: Proposed NBPP and Other Key Changes and Trends.

Outlook 2026: ACA Marketplace Trends–A Conversation with Michael Cohen and Zach Sherman

Survey data from fiscal year (FY) 2022 suggest that entities that provide ground ambulance services in the State of New York are experiencing reimbursement challenges. Health Management Associates, Inc. (HMA), contracted with the United New York Ambulance Network (UNYAN) to conduct an independent study of the costs of delivering ground ambulance services in the state and the adequacy of payment for these critical services. The HMA-UNYAN survey data highlight the wide variation in costs within the ground ambulance industry in New York and the negative Medicaid margins the industry experiences. These data demonstrate that although ambulance entities of all sizes in New York have negative Medicaid margins, these margins worsen as entity size decreases and entities become more rural. Trends in negative margins appear to be linked to some degree to entities’ relative share of “responses without transport” or uncompensated transports. This white paper poses important considerations for policymakers.

As we kick off the new year, Health Management Associates (HMA) is launching a new series of brief, insightful interviews with our policy experts on issues that will define 2026—what’s changing, why it matters, and how federal, state, and industry decisions will shape what happens next. Building on our earlier analysis of the Rural Health Transformation Program ((RHTP), here and here), this week, we start with a pointed look at the Centers for Medicare & Medicaid Services’s (CMS) first year of RHTP awards.

An interview with Kathleen Nolan, Senior Advisor, HMA, and Sara Singleton, Principal, Leavitt Partners, an HMA Company.

Q: What do the new Rural Health Transformation Program awards tell us about US Department of Health and Human Services (HHS) and CMS priorities heading into 2026?

Kathleen Nolan: One of the clearest signals is that CMS expects visible progress in 2026. This is not a program that gives states months of planning runway. The application made it clear that CMS wants states to start doing the activities they proposed right away—not just planning or propping up existing systems. CMS wants to see meaningful movement on implementation in 2026, especially in the areas of workforce, infrastructure, technology modernization, and care delivery redesign.

Sara Singleton: Exactly, and CMS is using this investment to reinforce some of the administration’s broader policy goals. Many state proposals leaned heavily into chronic disease prevention, chronic care management, and expanding supports that promote healthier lifestyles. That alignment isn’t accidental. The Administration is looking for real traction on these priorities, and RHTP gives states both the resources and the accountability framework to make progress. So, the message from CMS is clear: Move quickly, implement strategically, and show early gains in the areas that matter for long-term population health.

Q: Was anything in the awards themselves surprising?

Singleton: There was a lot of speculation about how wide the spread in funding levels might be, particularly for states’ discretionary initiatives. But the distribution was relatively tight; 32 states fell in the “average” range of $190‒$230 million, with only four states above $230 million and 13 below $190 million. That suggests CMS isn’t signaling dramatic differences in expected performance or ambition.

Nolan: It reinforces that CMS is looking for consistent, measurable progress from every state. States that struggle to implement their plans could see less funding in about years.

Q: What should states keep top of mind heading into year one?

Nolan: Accountability. CMS has made it clear they will adjust budgets in later years if states don’t meet expectations on reporting and evaluation. That also means states need to know where the dollars are going and what they are getting for the investment. Year one performance really matters.

Singleton: And it’s not just CMS. Congress and the Office of Inspector General for HHS will also be watching how states use these funds.

Q: What rural health policy developments are you watching in early 2026?

Nolan: Decisions about the leadership for these initiatives and state legislatures. Federal investment can only go so far. States will need strong leaders and supportive policies to accelerate and sustain RHTP efforts in year one. What legislatures choose to prioritize will shape the impact of RHTP far beyond year one.

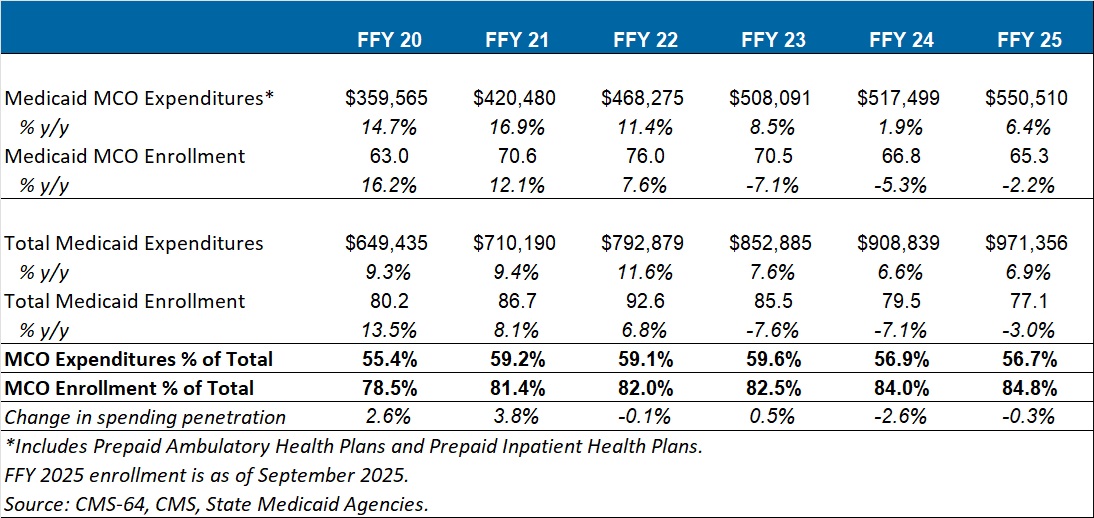

This week, our In Focus section highlights findings from a Health Management Associates Information Services (HMAIS) analysis of the Centers for Medicare & Medicaid Services (CMS) preliminary CMS-64 Medicaid expenditure report for federal fiscal year (FFY) 2025. The data show total medical services expenditures reached $971.4 billion across all states and territories, up 6.9 percent from FFY 2024.

This CMS-64 spending detail provides important context as states prepare for their upcoming legislative sessions and begin implementing changes required under the 2025 budget reconciliation act (P.L. 119-21, OBBBA). Early fiscal and operational pressures will stem from changes to the Supplemental Nutrition Assistance Program (SNAP) and preparations for community engagement requirements for Affordable Care Act (ACA) Medicaid expansion enrollees. In subsequent years, pressures will intensify because of major changes to provider tax financing and new federal limits on state directed payments in 2027 and early 2028.

In this article, we provide a deeper review of Medicaid spending, including the federal-state financing split. As Medicaid agencies prepare for upcoming spring sessions and anticipate potential program changes under OBBBA, it is notable that nearly two-thirds of Medicaid directors report an at least fifty percent likelihood of a Medicaid budget shortfall in FFY 2026.

Growth and Drivers in Medicaid Managed Care Spending

The HMAIS analysis looks at CMS-64 preliminary estimates of Medicaid spending by state for FFY 2025. CMS tracks state expenditures through the automated Medicaid Budget and Expenditure System/State Children’s Health Insurance Budget and Expenditure System (MBES/CBES).

While enrollment decreased for most states following the COVID-19 public health emergency unwinding, states saw an uptick in expenditures due to increased state directed payments, greater utilization and sicker populations, higher drug costs, increased provider rates, and greater use of long-term services and supports and behavioral health.

Key findings from HMAIS’ analysis (see Table 1), include:

These figures include spending on comprehensive risk-based managed care organizations (MCOs), prepaid inpatient health plans (PIHPs), and prepaid ambulatory health plans (PAHPs). PIHPs and PAHPs refer to prepaid health plans that provide a subset of services, such as dental or behavioral health care. This total is exclusive of fee-based programs such as primary care case management models.

Table 1. Medicaid MCO Expenditures as a Percentage of Total Medicaid Expenditures, FFY 2020–2025 (in millions)

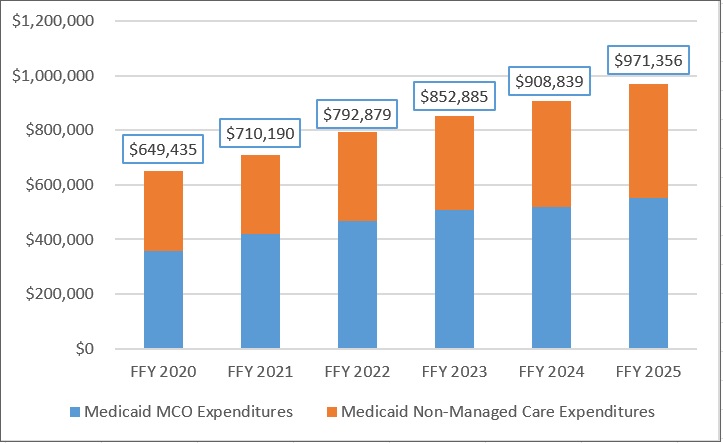

Annual Medicaid managed care expenditures have grown consistently with total Medicaid expenditures. After slower growth in FFY 2024—which aligned with the post-COVID-19 policy unwinding period when many states completed eligibility redeterminations—FFY 2025 again experienced an uptick in managed care growth (see Figure 1).

Figure 1. Total and MCO Medicaid Expenditures, FFY 2020–2025 ($M)

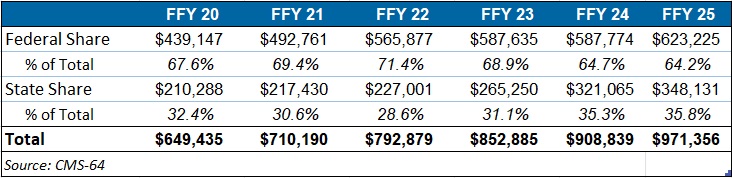

Federal versus State Share Spending

The preliminary FFY 2025 expenditure data provides a baseline before OBBBA’s changes are scheduled for implementation and as states continue to face Medicaid funding challenges. In FFY 2025, federal funding accounted for 64.2 percent of FFY 2025 spending, and non-federal matching funds accounted for 35.8 percent (see Table 2). Particularly later in 2027, 2028, and subsequent years, Medicaid expansion states stand to see disproportionally larger increases in their share of spending.

Table 2. Federal versus State Share of Medicaid Expenditures, FFY 2020–2025 (in millions)

T-MSIS Data Adds Detail to CMS-64 MCO Spending

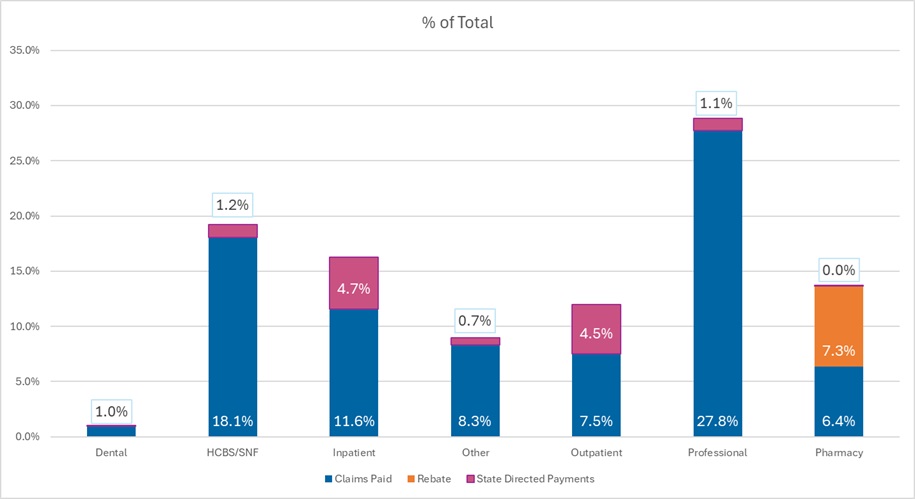

To complement CMS-64 macro-spending trends, HMA developed a methodology allowing us to use Transformed Medicaid Statistical Information System (T-MSIS) data to approximate managed care spending by service category. Although T-MSIS enables more granular views (e.g., professional services, inpatient/outpatient hospital services, skilled nursing facilities (SNFs), HCBS, clinics, pharmaceuticals), the most recent dataset typically lags one to two years behind CMS-64 totals.

HMA’s analysis of the T-MSIS data shows that while managed care remains the dominant delivery system model for Medicaid, spending by provider types helps contextualize the CMS-64 report. Notably, the CMS-64 reports FFY25 data and our report below on T-MSIS disaggregation uses 2023 data. Although the T-MSIS and CMS-64 data are for different years, it still highlights the main components of the largest spending component of the CMS-64 with more recent data.

The 2023 T-MSIS analysis shows the following:

Figure 2. T-MSIS Medicaid Spending by Service Category 2023 (MCO disaggregated plus FFS)

What to Watch

Because Medicaid is such a big part of state government spending, outlays for Medicaid will always be a focus and challenge for states. Upcoming state legislative sessions and OBBBA driven changes will begin in 2026 with SNAP pressures and major operational preparations for community engagement requirements for expansion states. Preparations for new limits on provider taxes and state directed payments will likely begin immediately, but the true impacts will occur in 2027 and early 2028. States will need to tailor their programs under funding constraints.

Connect with Us

HMAIS, a subscription-based tool that Health Management Associates offers, provides state-by-state analysis of the CMS-64 data, Medicaid managed care enrollment trends, and state budget reporting. For more information about an HMAIS subscription, contact Andrea Maresca and Alona Nenko. For details on T-MSIS data, contact Matt Powers and Shreyas Ramani.

Tracking Medicaid’s Growth: FFY 2025 Spending and T-MSIS Data Provide Insights on Managed Care Spending

This webinar was held on February 4, 2026 at 12pm ET.

Upon the release of the CMS final 2027 Notice of Benefit and Payment Parameters and the accompanying Letter to Issuers in January, health plans and state policymakers will face critical decisions that shape the next phase of the individual and small group markets.

Experts from HMA and Wakely discussed what the proposed rule means in practice and how stakeholders can begin preparing now. This webinar provided a clear overview of the final 2027 NBPP** and Letter to Issuers, highlighted the most significant policy changes and clarifications, and explored the operational and strategic implications for states. Speakers focused on how the final policies may influence market stability, affordability, program administration, and longer-term planning for 2027 and beyond.

** We expect that the NBPP will have been released before the webinar takes place, but if the NBPP is not yet released we will cover likely scenarios based on our best available information.

Learning Objectives:

•Understanding the proposed 2027 NBPP and Letter to Issuers

•Awareness of key implications for states and issuers

•Discussion of key planning considerations for 2027

The federal drug pricing landscape continues to undergo significant transformation as executive branch agencies advance an ambitious suite of regulatory and model testing initiatives intended to lower the costs associated with the Medicare and Medicaid programs. In response to ongoing concerns about rising out-of-pocket costs, increasing pressure to align US prices with those paid internationally, and the continued implementation of the Inflation Reduction Act (IRA), federal agencies are reshaping how prescription drugs are priced, reimbursed, and negotiated in federally financed programs.

The current policy environment reflects a growing emphasis on benchmarking drug prices to those in peer nations, referred to as “most favored nation” (MFN) benchmarks, and accelerating actions that require or encourage manufacturers to offer lower net prices. Health Management Associates (HMA), is tracking these developments in the public payer space, replicating Centers for Medicare & Medicaid Services (CMS) payment methodologies, and modeling alternative policies to assist life science companies, payers, and other stakeholders.

In this article, we review the administration’s recent efforts to reduce Medicare and Medicaid spending on drugs and biologics, including confidential manufacturer negotiations and three new models that together could reshape pricing dynamics across federal programs.

Executive Branch Negotiations Seek to Drive Access to MFN Discounts

In 2025, the administration issued an Executive Order directing federal agencies to pursue strategies to establish MFN pricing, linking US prices for certain drugs to the lowest (or second lowest) adjusted net prices among a targeted set of peer countries. Following the order, federal officials sent letters to 17 major pharmaceutical and biotechnology manufacturers, urging them to negotiate agreements that would voluntarily align prices with MFN-based benchmarks.

To date, 14 manufacturers have signed agreements, though full details remain confidential. These agreements are understood to accomplish the following:

Reports suggest that manufacturers entering these MFN-related arrangements may receive exemptions from several federal actions, including the Center for Medicare and Medicaid Innovation (Innovation Center) demonstration models described below and certain tariff-related policies.

MFNLinked Models Designed to Lower Drug Costs Across Medicare and Medicaid

Along with the negotiation efforts, the CMS Innovation Center has proposed three models that would test MFNbased pricing through structured rebate mechanisms. Each model targets different segments of the market while testing how international benchmarks could be integrated into federal drug payment policy.

New Models Test Alternatives to Inflation Rebates

Announced in December 2025, the Global Benchmark for Efficient Drug Pricing (GLOBE) Model and the Guarding US Medicare Against Rising Drug Costs (GUARD) Model are designed to test alternative approaches to the Inflation Reduction Act’s (IRA) inflation penalty policies. CMS plans to test the models’ potential for market driven price reductions if manufacturers choose to lower list prices instead of paying MFN-based rebates.

Key features of the GLOBE Model are as follows:

The GUARD Model will similarly test whether applying MFN-based rebates to Medicare Part D drugs will lower Medicare costs. Key aspects of this model include:

These models rely on pricing data from 19 countries. Manufacturers that voluntarily submit net price information would trigger quarterly benchmark updates; otherwise, CMS will use a fixed list price based benchmark for the entire pilot period.

CMS is seeking comments on whether additional categories, for example cell and gene therapies, should be excluded from GLOBE. GUARD is also open for comment through February 23, 2026.

GENErating cost Reductions fOr US Medicaid (GENEROUS) Model

The GENEROUS model, expected to begin in 2026, creates a voluntary pathway for state Medicaid programs and manufacturers to enter supplemental rebate agreements tied to MFNaligned prices. MFN pricing under this model is based on the second lowest net price in G7 countries plus Denmark and Switzerland. GENEROUS is also expected to align with pricing commitments negotiated through the administration’s manufacturer agreements.

Key Considerations and Potential Impacts

The combined effect of federal negotiations and Innovation Center models could be substantial, though outcomes will depend on manufacturer participation, benchmark stability, and operational feasibility. Key considerations include:

Connect with Us

HMA experts continue to track the federal drug pricing landscape closely as comments, operational details, and implementation timelines evolve across these initiatives. Our team replicates CMS payment methodologies and models alternative policies using the most current Medicare FFS and Medicare Advantage (100%) claims data.

For more information and questions about the policies described in this article, please contact our experts below.

On December 29, 2025, the Centers for Medicare & Medicaid Services (CMS) announced the state awards for the Rural Health Transformation Program (RHTP), a $50 billion federal initiative intended to stabilize rural health systems and support transformation. CMS stated that $10 billion will be available each year from 2026 to 2030, and that first-year (2026) state awards average $200 million, with totals ranging from $147 million to $281 million.

This announcement marks a pivot from planning to execution. In the coming months, states will move rapidly to finalize governance structures, confirm partners, and translate proposed initiatives into operational workplans and measurable outcomes.

Although CMS announced the overall awards for the first budget year, some states have signaled they continue to work with CMS on initiative-specific budgets and planning. In this article, Health Management Associates (HMA) reviews key themes and early trends based on the application initiatives and what is known about the budgets.

What the Awards Suggest About State Priorities

Although each state’s awarded approach reflects local realities, early patterns across awardees’ project abstracts suggest several recurring priorities that may shape implementation activity in 2026.

1) Building the Data, Analytics, and Interoperability Backbone

A number of awardees prioritized shared infrastructure for interoperability, analytics, performance monitoring, and operational backbone capabilities. Examples include:

2) Strengthening Maternal Health and Perinatal Care

Many awardees emphasized stabilizing rural maternity access and strengthening perinatal supports through strategies, such as:

Why it matters: Rural maternity deserts and workforce constraints remain critical drivers of avoidable complications and adverse outcomes. Approaches piloted in rural settings may inform broader statewide maternity care strategies.

3) Modernizing Emergency Medical Services and Mobile Care

Several awardees included investments intended to strengthen emergency response and build more reliable rural stabilization capacity.

Why it matters: EMS and mobile response models can function as connective tissue in rural systems with limited traditional access points.

Why it matters: Data-sharing infrastructure can enable multi-provider coordination, performance tracking, and the operational foundations needed for sustainable transformation.

4) Integrating Behavioral Health and Community-Based Supports

Awards also reflected ongoing efforts to expand behavioral health access and improve integration with physical health and community supports. For example:

Why it matters: Behavioral health capacity constraints are frequently more acute in rural areas, and integration strategies often require both reliable workforce and technology supports.

What to Watch Next

With awards announced, attention will quickly turn to implementation. Stakeholders should have processes to track the following:

CMS also signaled near-term oversight and engagement mechanisms, state-assigned CMS project officers, kickoff meetings, ongoing technical assistance, and regular progress updates, along with a planned annual CMS Rural Health Summit.

Tracking State RHTP Implementation

The HMAIS team developed a resource to capture available information about state RHTP activities, applications, and initiatives and provide a road map for identifying state-specific proposals, requested funding, governance structures, and other key aspects of state RHTP initiatives.

Following CMS’s award announcement, HMAIS is updating this Rural Health Transformation Program (RHTP) Tracker to incorporate award-specific details as they become publicly available. The resource includes information about FY26 awards by state and initiatives, links to CMS materials and state-posted implementation documentation, and a consolidated view of emerging themes and trends as implementation accelerates in 2026.

Looking Ahead

The award announcement is the beginning of implementation. As states operationalize initiatives in early 2026, organizations that align early to awarded priorities and implementation timelines will be best positioned to support rural-first efforts that deliver measurable and lasting results.

For questions about the RHTP opportunities for your organization and the solutions HMA can tailor to meet the needs of your state, contact Kathleen Nolan and Andrea Maresca.