As the US Senate debates H.R. 1—a sweeping legislative package that the House passed on May 22, 2025, which would impose nationwide Medicaid work and community engagement requirements by the end of 2026— Health Management Associates’ (HMA’s) latest analysis offers insights into the potential impact of these changes. Drawing on Transformed Medicaid Statistical Information System (T-MSIS) data, HMA experts examine the health and demographic profiles of the approximately 16 million individuals who comprise the Medicaid expansion population.

This 10-slide presentation of findings underscores the high prevalence of chronic and behavioral health conditions among these individuals, raising important questions about how new eligibility requirements could affect access to care and health outcomes. Notably, the presentation contextualizes health needs with Medicaid spending patterns, comparing the Medicaid expansion group with other eligibility categories, such as dual eligibles and children. We explore how the proposals of the nine state 1115 demonstration applications could affect the work requirements policy and implementation landscape. It also breaks down pharmacy spending by therapeutic class, spotlighting common conditions like opioid use disorder.

These insights are especially valuable for Medicaid managed care organizations, providers, and other stakeholders that will play a key role in designing work requirement initiatives and operationalizing any new requirements. Our May 22, 2025, article—Building State Capacities for Medicaid Work and Community Engagement Requirements—delves into the issues that are central to such discussions.

With deep expertise in Medicaid policy, demonstration design, and advanced analytics, HMA is uniquely positioned to help states, plans, and providers navigate the evolving federal landscape. For more information about HMA’s T-MSIS capabilities, contact featured experts below.

On March 4, 2025, the Centers for Medicare & Medicaid Services (CMS) rescinded the 2023 and 2024 guidance on Health-Related Social Needs (HRSN) Section 1115 demonstrations. This policy shift signals a significant pivot in federal Medicaid priorities under the current administration. While states with approved HRSN demonstrations may continue operating under existing terms, the path forward for pending proposals and future renewals is less certain.

This article explores key considerations Health Management Associates (HMA), experts identified for states that need to realign HRSN activities with other activities to align with the Trump Administration’s federal policy objectives and priorities for Section 1115 Medicaid and CHIP demonstrations.

Background on HRSN Initiatives in Section 1115 Demonstrations

In November 2023 and December 2024, CMS published guidance on a new Section 1115 demonstration that gave state Medicaid and CHIP agencies the opportunity to address the broad environmental conditions, or social determinants of health (SDOH), that affect people’s health. This initiative permitted states to address the individual-level adverse social conditions of enrollees that contribute to negative health outcomes. To assist states in their efforts, CMS approved Section 1115 demonstrations that piloted the provision of housing, food, non-medical transportation, and other environmental supports that meet enrollees’ HRSNs.

What does CMS’s rescission of the HRSN demonstration policy initiative mean for states planning their next steps and priorities for Medicaid and CHIP?

First, CMS’s March 4 rescission has no impact on states with a current, active Section 1115 demonstration that includes HRSN. States with HRSN demonstrations can maintain their approved programs until the scheduled expiration date; however, requests to amend any aspect of the program before it expires could subject the state to renegotiation of HRSN components that align with the new federal direction.

Second, states with pending HRSN Section 1115 demonstration proposals should proactively consider new coverage approaches to authorize services that address an individual’s SDOH. Pending proposals developed using the now rescinded guidance may require substantial changes to gain approval. States should also prepare for additional public comment periods if revisions significantly alter the original design.

Looking ahead, CMS is not expected to renew demonstration components that no longer align with current federal objectives. This projection pertains to any demonstration component, not just the rescinded HRSN guidance. States should start planning now for how they will sustain successful HRSN-related outcomes through alternative coverage pathways.

Strategic HRSN Pivot Considerations

While the HRSN guidance has been rescinded, CMS has not withdrawn the 2021 State Health Official Letter RE: Opportunities in Medicaid and CHIP to Address Social Determinants of Health (SDOH) (SHO# 21-001), published during the first Trump Administration. This leaves room for states to pivot HRSN initiatives into other federal authorities, such as:

State Plan Amendments and Waivers. These approaches include state plan options, 1915 waiver options, CHIP Health Services Initiatives, as well as certain special program authorities like Program of All-Inclusive Care for the Elderly or Money Follows the Person.

Childhood Chronic Disease Prevention: States could consider aligning SDOH activities with the Make America Healthy Again initiative of the current administration by focusing on environmental factors that adversely affect an enrollee’s health, such as poor nutrition, chronic stress, overexposure to synthetic chemicals, and mental health challenges.

Justice-Involved Populations: States could explore reentry services and SDOH supports for individuals transitioning from carceral settings to the community, including compliance with new Medicaid requirements for incarcerated youth under the Consolidated Appropriations Act of 2023.

School-Based Health Services. States could explore SDOH activities as part of new approaches to address gaps in the provision of school-based health services to Medicaid and CHIP eligible children. CMS and the US Department of Education launched a joint effort to expand school-based health services by establishing the Medicaid School-Based Services (SBS) Technical Assistance Center to help states increase healthcare access to children enrolled in Medicaid and CHIP. States could explore SDOH initiatives that expand the capacity of school-based entities that provide assistance under Medicaid or CHIP.

Looking Ahead

As states recalibrate their Medicaid and CHIP strategies, understanding how they can align with evolving federal priorities is critical for all stakeholders. Notably, Medicaid stakeholders, including managed care organizations, hospitals and health systems, and providers, also have several opportunities, including:

Inform State Strategy: Plans and providers can share data and outcomes from HRSN interventions to help states assess the value of these services and whether they should continue under alternative authorities.

Shape New Demonstration Designs: As states pivot to align with new federal priorities, plans and providers can offer practical insights into how SDOH interventions could be integrated into behavioral health, reentry, school-based services, and chronic disease prevention efforts.

Strengthen Community Partnerships: Continued collaboration with community-based organizations will be essential to maintain service delivery and demonstrate impact in new policy contexts.

Connect With Us

HMA’s team—including former CMS Section 1115 leaders and other colleagues steeped in Medicaid and CHIP policies and operations—offers unique expertise in designing demonstrations that reflect current federal policy priorities and maximize state outcomes in alignment with program objectives that CMS will support.

For questions about these developments and your organization’s plan to adapt to new federal Medicaid policy priorities, contact our featured experts below. Connect with our experts and other leaders experienced in new pathways for covering effective services at the HMA National Conference, October 14-16, 2025, in New Orleans, LA.

As Congress intensifies negotiations over budget reconciliation, including potential changes to Medicaid financing and Affordable Care Act (ACA) subsidies, new data from Wakely Consulting Group, an HMA (Health Management Associates) company, sheds light on how the effects of the Medicaid redetermination process continued to unfold well into 2024. Appendix A of the May 2025 white paper Medicaid Redetermination Impacts on the Individual Market, provides a full-year view of enrollment and morbidity trends, showing that the influx of former Medicaid enrollees had some negative effects on risk scores. In fact, relative risk increased across all market types—state-based exchanges (SBEs), in federally facilitated exchange (FFE) Medicaid expansion states, and FFEs in non-expansion states—despite substantial enrollment growth.

Data presented in Wakely’s white paper and their experts’ findings challenge the conventional assumption that higher enrollment dilutes risk and suggest that many new enrollees may have had unmet health needs or delayed care. The data also show that states with the highest enrollment growth did not necessarily experience the greatest morbidity shifts. This decoupling of enrollment and morbidity complicates forecasting for insurers and policymakers alike, especially as Congress debates Medicaid funding and ACA subsidy structures in the ongoing budget reconciliation process.

What to Watch

As federal lawmakers consider reforms that could alter Medicaid eligibility, subsidies, and risk adjustment mechanics, these findings underscore the importance of monitoring not just how many people enroll, but who they are and the type of care they need. The individual market’s evolving risk profile will have direct implications for premium setting, subsidy design, and the financial stability of plans that serve this population.

Connect with Us

Wakely is experienced in all facets of the healthcare industry—from carriers to providers to government agencies. Wakely’s actuarial experts and policy analysts continually monitor and analyze potential changes to inform clients’ strategies and propel their success.

For more questions about the analysis contact our experts below.

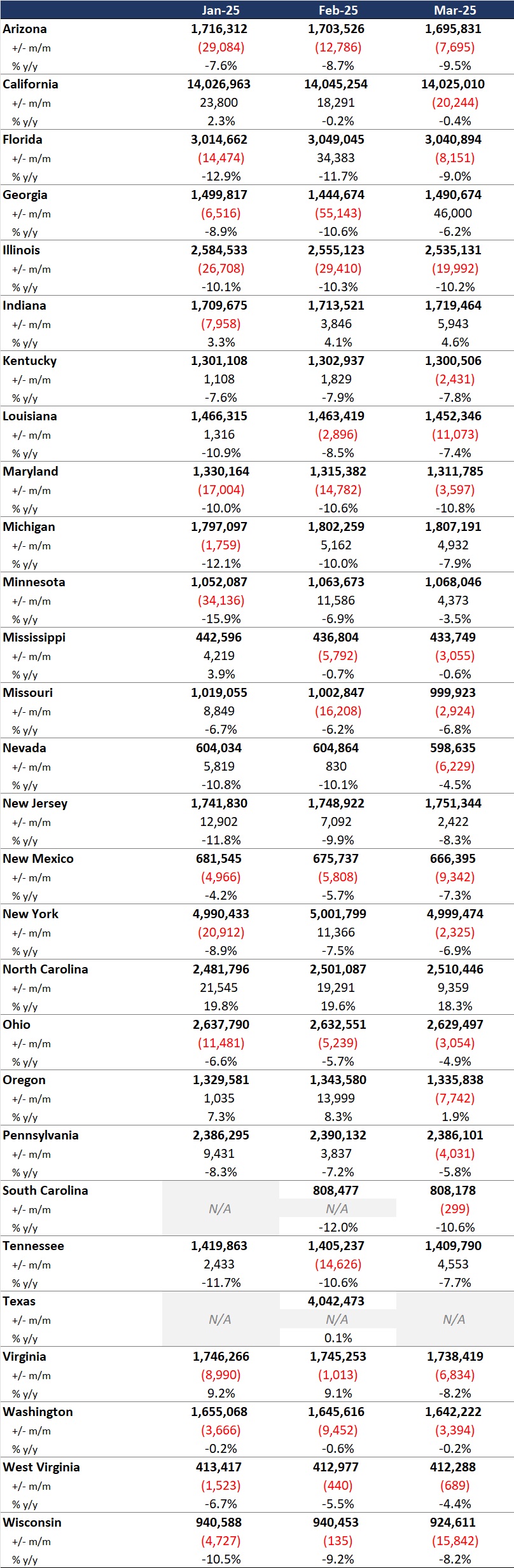

In this week’s In Focus section, Health Management Associates Information Services (HMAIS) draws on its database of monthly enrollment in Medicaid managed care programs to provide the latest quarterly analysis of Medicaid managed care enrollment, offering a snapshot of developments across 28 states.[1] The data and insights are particularly timely as stakeholders, including states, Medicaid managed care organizations (MCOs), hospitals and health systems, and providers, continue to plan for multiple possible federal policy changes and the operational realities that will follow.

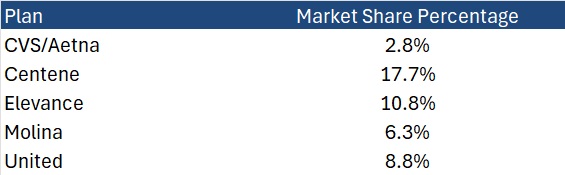

HMAIS also compiles a more detailed quarterly Medicaid managed care enrollment report representing nearly 300 health plans in 41 states. The report provides by plan enrollment plus corporate ownership, program inclusion, and for-profit versus not-for-profit status, with breakout tabs for publicly traded plans. Table 1 shows a sampling of plans and their national market share of Medicaid managed care beneficiaries based on a total of 66 million enrollees. These data should be viewed as a broader representation of enrollment trends rather than as a comprehensive comparison.

Key Insights from Q1 2025 Data

The 28 states included in our review have released monthly Medicaid managed care enrollment data via a public website or in response to a public records request from Health Management Associates (HMA). This report reflects the most recent data posted or obtained. HMA has made the following observations related to the enrollment data:

Year-over-year growth. As of March 2025, across the 28 states reviewed, Medicaid managed care enrollment declined by 2.5 million members year-over-year, a 3.9 percent drop as of March 2025 (see Figure 1). This marks a continuation of the downward trend reported in late 2024, though with notable variation across states.

Figure 1. Year-over-Year Growth in Medicaid Managed Care States, 2020−24, March 2025

Localized growth amid broader declines. While most states experienced enrollment reductions, Indiana and North Carolina bucked the trend with measurable gains, suggesting the influence of state-specific policy shifts or demographic factors. Oregon and Texas also saw modest growth.

Sharpest contractions. Illinois, Maryland, and South Carolina, reported double-digit percentage drops, underscoring the uneven impact of redeterminations and eligibility changes.

Difference among expansion and non-expansion states. Among the 21 states included in our analysis that expanded Medicaid, enrollment fell by 1.8 million (-3.6%) to 48.6 million. In contrast, the seven non-expansion states saw a steeper proportional decline (-5.4%), to a total of 12.2 million enrollees.

Table 1. Monthly MCO Enrollment by State, January 2025 through March 2025

Note: In Table 1 above and the state tables that follow, “+/- m/m” refers to the enrollment change from the previous month, and “% y/y” refers to the percentage change in enrollment from the same month in the previous year.

It is important to note the limitations of the data presented. First, states report the data at the varying times during the month. Some of these figures reflect beginning of the month totals, whereas others reflect an end of the month snapshot. Second, in some instances, the data are comprehensive in that they cover all state-sponsored health programs that offer managed care options; in other cases, the data reflect only a subset of the broader managed Medicaid population. This limitation complicates comparison of the data described above with figures reported by publicly traded Medicaid MCOs. Hence, the data in Table 1 should be viewed as a sampling of enrollment trends across these states rather than a comprehensive comparison, which cannot be established solely based on publicly available monthly enrollment data.

Market Share and Plan Dynamics

Using our data repository from 300 health plans across 41 states, HMAIS’s report addresses corporate ownership, program participation, and tax status. As of March 2025, Centene continues to lead with 17.7 percent of the national Medicaid managed care market, followed by Elevance (10.8%), United (8.8%), and Molina (6.3%), as Table 2 shows.

Table 2. National Medicaid Managed Care Market Share by Number of Beneficiaries for a Sample of Publicly Traded Plans, March 2025

What to Watch

The policy backdrop remains fluid. The US House of Representatives’ passage of the One Big Beautiful Bill Act introduces sweeping changes to Medicaid financing, including proposed cuts of up to $715 billion. Additional federal proposals, such as mandatory work requirements, could further reshape enrollment patterns.

Stakeholders should prepare for:

Implementation of work/community engagement mandates for certain adult populations

Potential redesign of Affordable Care Act expansion programs

Retraction of federal regulations focused on streamlining of eligibility and redetermination processes to improve accuracy and efficiency

Connect with Us

HMA is home to experts who know the Medicaid managed care landscape at the federal and state levels. As the Medicaid landscape continues to evolve, HMAIS equips stakeholders with timely, actionable intelligence. Our subscription service includes enrollment data, financials, waiver tracking, and a robust library of public documents.

For more information about the HMAIS subscription, contact our experts below.

[1] Arizona, California, Florida, Georgia, Illinois, Indiana, Kentucky, Louisiana, Maryland, Michigan, Minnesota, Mississippi, Missouri, Nevada, New Jersey, New Mexico, New York, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Tennessee, Texas, Virginia, Washington, West Virginia, Wisconsin.

We recently sat down with Medicare experts from HMA and Wakely to break down the most important and most pressing developments shaping the future of Medicare Advantage, including the latest updates from CMS on Risk Adjustment Data Validation (RADV) audits, specifically the two major announcements released on May 21st and May 30th that are sending waves through the payer and provider communities alike.

On May 21st, CMS issued new guidance related to extrapolation and how sampling methodology and medical record review standards will evolve under the updated RADV Final Rule.

Then, just nine days later, on May 30th, CMS released additional operational instructions that may tighten reporting windows, add new thresholds for error rate evaluation, and expand expectations around provider documentation compliance—particularly for retrospective reviews and risk adjustment data sourcing.

To help unpack this fast-moving landscape, we’ve spoken with our Medicare experts, Tony Pistilli, Ryan McEntee and David Nater, each bringing a unique lens to the RADV conversation.

What was your first thought when you read CMS’s latest RADV update last week?

Tony – My main takeaway was that CMS was really upping the game in terms of what payers need to do to not only do the appropriate measures to optimize their risk scores but then audit claims that are coming in from providers. So this isn’t just a matter of ensuring that risk score optimization strategies are appropriate, not overstepping, but also adding a new administrative task of auditing claims that you’re getting from providers that may have errors in them.

Can you quickly summarize what CMS actually changed in this latest announcement, and what’s most significant about it compared to the previous announcement in November last year and previous RADV audits?

Ryan – The core of these changes, prior to the old way of doing RADV is, of course the extrapolation methodology that CMS will be introducing, as well as the elimination of the fee-for-service adjuster, which is going to be huge. Then we can move on to that with the announcement of enhancements of staffing and technology.

It’s going to be very interesting how CMS looks to utilize that. As well as every single contract being audited that is eligible are probably the focus points within this, and with CMS they give you a little, and then you have to look into it a lot, so I think there’s still a lot more to come related to these initial announcements that are coming through.

What exactly does this mean from a health plan perspective in the near term – especially for those already in the trenches of risk adjustment audits or pre-audit reviews?

David – Most financial teams use claims as forecasting and having concurrent risk adjustment processes is really the optimal approach to make sure that there are no surprises on the financial end for month end and quarterly reports. Making sure that plans are getting ahead of this cleanup now is imperative to mitigate those financial impacts, and then on a concurrent level, optimizing the operational processes ensures just better forecasting and overall better financial outcomes.

With the latest announcements regarding RADV, what are the current unknowns at play related to this new look RADV strategy?

Tony – On a technical level, the key things we don’t know are how CMS is going to sample claims – They’ve indicated that they’re going to move from random sampling to targeted sampling – and we don’t know how they’re going to extrapolate that. So, if you do a targeted sample, do you extrapolate that just to a targeted extrapolation, or do you extrapolate that to the whole plan? And that’s your range of low impact to high impact.

Similarly, we don’t know what confidence interval CMS is going to use. There’s been some indications of 99% in the past. That’s going to be very conservative, but 95 or 90% would be plausible confidence intervals as well, and that gets you to much more aggressive recovery rates. There are a few other small technical issues that I don’t think will have as big of an impact, but those are the three ones that we’re really looking to CMS to figure out.

What’s the one thing you think plans need to prioritize immediately in light of this update – and what’s the trap they need to avoid?

Ryan – I think plans need to very quickly understand their exposure. One of the ways to do that—and one of the ways we are engaging our clients—is to run analytics looking at these high-risk codes. There are also certain indicators you can look at to see what needs to be reviewed and what has high error rates, based on previous OIGYG and CMS audits. From there, you need to get a quick plan in place to document and assess whether or not those codes are relevant. If they are not, submit them before the aggressive timeline CMS has put in place.

As I mentioned, there are less than two weeks to submit deletes for 2019 dates of service, and every 7 days after that thereafter for each payment year. So, the time to act is now. You need to quickly understand where your risk is and take action. And if you don’t have those capabilities, engage with strong consulting groups or partners who can support you through this.

What closing thoughts or takeaways would you like to share?

Ryan – If I put myself on the plan side, I see both a short-term, immediate plan and a long-term sustainability plan.

That short-term immediate plan is action to act NOW. Whether that is engaging with a partner, or engaging in your internal team, you need to be able to highlight where your risk areas are. Take action on this prior to CMS coming in and acting for you. What’s just as important is setting up a long-term roadmap to be able to mitigate this risk going forward.

To look at it concurrently, do you have the right analytics in place? Do you have the correct staffing in place to be able to look at these risk codes coming in? Assess them and send the necessary deletes coupled with closing the loop related to feedback. Are you pushing that information and education back to your physician groups? Because they’re the most important part to this. You need to be able to educate, communicate and meet with your providers to explain how important the act of documentation and coding is and have this at the forefront of every one of your initiatives and incentive programs going forward in value-based care.

David – HMA and Wakely are well-positioned to help in both the short-term and the long-term approach, and ideally both. Organizations need to act quickly and align their steady-state processes to ensure that they’re managing both the exposure at the health plan level and with the providers, especially those in risk-based arrangements.

Tony – Plans need to be thinking of the RADV risk here, apart from the risk that they might see from chart reviews and other add activity. You may be a plan that’s relatively unaggressive in chart reviews and adds that think “we’re not risk here”, but CMS has now assigned you risk for all the claims that providers are submitting, and you need to be ensuring that those are correct as well.

There’s a wholly separate administrative task here that plans have now assumed responsibility for, and your revenue is just as at risk for not doing the RADV as it is for being inappropriate in your chart reviews and adds and whatnot. So, you really want to be thinking of this as two separate things and acting from both fronts.

In May 2025, the US House of Representatives passed a budget bill that includes funding for cost-sharing reduction (CSR) payments, marking a potential end to the “silver loading” practice that has shaped pricing in the Affordable Care Act (ACA) Marketplace pricing since 2017. The US Senate is now considering this legislation as part of a broader budget reconciliation package that includes major Medicaid reforms, such as new work requirements and changes to eligibility and financing rules.

This evolving policy landscape has significant implications for states, payers, providers, and consumers. Wakely, an HMA Company, recently published Implications of Ending Silver-Loading on the Individual Market, which outlines how reinstating CSR payments could reshape ACA marketplace plan pricing, enrollment patterns, and federal subsidy flows. It also highlights the operational and financial risks stakeholders must prepare for in 2026.

Broad Loading and Silver Loading

Because CSR loading increases premium costs on silver plans that determine subsidies, they also increase federal payments for premium tax credit (PTC) subsidies. Guidance from the US Department of Health and Human Services on silver plan pricing has evolved over time. Three types of CSR loading are occurring in ACA markets, specifically:

Broad loading: Increasing premiums for all metal level qualified health plans (QHPs) in the individual market to collect enough revenue to offset the CSR costs of the silver plan variants enrollees

Two means of silver loading:

Increasing premiums for only silver QHPs in the individual market to collect enough revenue to offset the CSR costs of the silver plan variant enrollees

Raising premiums, functionally, for only on-exchange silver QHPs

As discussed in the Wakely paper, the impact of silver loading is that the federal government is likely paying out more in additional PTC subsidies than would be paid if CSR payments were fully funded. On Friday, May 2, 2025, the Centers for Medicare & Medicaid Services (CMS) released guidance related to silver loading and CSR payments for 2026 rate filings. This action was urgently needed, especially for states with May filing deadlines.

What’s at Stake

If Congress does appropriate funding for CSR payments, some issuers will be reimbursed for the difference in cost sharing between standard and CSR-enhanced silver plans. Issuers that cover nonemergency pregnancy termination services, would be ineligible for CSR payments; however, as the Wakely paper indicates, these payments would not cover the additional utilization driven by richer benefits. For example, it is anticipated that a member in a 94 percent actuarial value CSR plan will use more services (i.e., four primary care visits versus three in a standard plan), but reimbursement would only reflect the cost-sharing difference—not the increased volume of care.

States like Georgia and New Mexico, which mandate silver loading, could see significant shifts in premium relativities and enrollment behavior. Wakely’s modeling suggests that changes in CSR policy—especially if paired with the expiration of enhanced premium subsidies at the end of 2025—could lead to higher net premiums, reduced enrollment, and a deterioration in risk pool morbidity.

What to Watch

The Senate’s deliberations will determine whether CSR funding is restored and could have significant implications on whether enhanced premium subsidies are extended beyond 2025. These decisions will directly affect the following:

2026 rate filings and benefit designs

Marketplace affordability and enrollment stability

State reinsurance funding and 1332 waiver dynamics

Consumer costs and plan switching behavior

Wakely’s analysis also cautions that if CSR funding is restored without accounting for induced utilization, issuers may still need to price for higher service use—potentially leading to premium volatility. In addition, if broad loading is mandated instead of silver loading, it could raise premiums across all metal tiers and reduce the value of premium tax credits for many enrollees.

Key Considerations for Stakeholders

States should assess how CSR policy changes affect reinsurance programs, waiver funding, and Medicaid redeterminations.

Payers must prepare for multiple pricing scenarios and evaluate how changes in subsidy structures influence enrollment and risk adjustment, 1332 reinsurance programs, and overall market risk.

Providers should anticipate shifts in patient mix and utilization (i.e., more uncompensated care with more uninsured patients).

Advocates need to monitor how policy changes affect access and affordability for low-income and underserved populations.

These developments also create more opportunities for movement between Medicaid, Marketplace, and uninsured populations, underscoring renewed opportunity for integrated eligibility systems and coordinated outreach.

Connect with Us

Health Management Associates (HMA), experts are actively advising stakeholders on how to navigate these complex changes. Whether you’re a state policymaker, health plan executive, provider leader, or advocate, we can help you assess the impact and plan strategically.

These issues will also be explored in depth at the HMA Conference in October 2025. To discuss how these developments will affect your organization, contact our featured expert below.

A recent case study highlighted how Health Management Associates (HMA) worked with a medical supply firm to identify gaps in their revenue cycle, and by working with us have seen improvements in denial rates and reimbursement. Advanced Diabetes Supply (ADS)/ US Medical Supply (USMed) came to HMA for help with its revenue cycle goals. What began as a revenue cycle gap assessment at one ADS office in California was expanded to be repeated for the Florida office. As a result, HMA helped ADS produce 12% YoY increase in cash collections, resulting in more than $38 million in additional revenue, and a $16 million reduction in outstanding A/R within six months.

A leading provider of diabetes supplies, ADS faced challenges in optimizing their revenue cycle processes. By partnering with HMA, they embarked on a transformative journey that resulted in streamlined operations and improved financial performance. The case study highlights the key strategies implemented by ADS and HMA, including the adoption of advanced technologies, process re-engineering, and staff training. These initiatives not only addressed existing inefficiencies but also paved the way for future growth and innovation.

Organizations need efficient revenue cycle management to ensure sustainability and growth in the constantly changing and competitive healthcare landscape. As healthcare reimbursement can involve many complex processes, it creates opportunities for gaps and process breakdowns. HMA helps organizations implement the processes, training, and technology necessary to close process gaps, improve cash flow, determine root causes for gaps, and reduce denials.

HMA experts have decades of experience in every facet of the revenue cycle. They come from all sides of the healthcare industry, including providers, payers, managed care organizations, and more.

On May 22, 2025, the US House of Representatives advanced a comprehensive legislative package that includes expansive changes to healthcare spending and tax policies. The One Big Beautiful Bill Act, H.R. 1, will be subject to further revision in the Senate – and potentially again in the House – before it can be sent to the president for his signature. If enacted, the legislation would have significant implications for the Medicaid program, including a nationwide work and community engagement requirement. The House-passed bill establishes a deadline of December 31, 2026, for implementation, but individual states could move earlier.

As state legislatures pass work requirement bills, governors consider executive actions, and Congress contemplates revisions to the Medicaid work mandate, vetting key implementation issues may significantly affect the direction of related policies. Even before implementation, states must test operations, enable systems, and establish connections to beneficiaries to reduce potential implementation missteps, inappropriate disenrollments, and litigation risks.

If the goal of Medicaid work requirement policies is to stimulate connections between health benefits and employment/workforce, building state and federal capacities to support these approaches is critical to effectuating that change. In the remainder of this article, Health Management Associates (HMA), experts focus on the operational dynamics that need to be discussed, tested, and built as states begin introducing work and community engagement initiatives.

Federal Policies and Early State Actions on Work Requirements

The House bill would require all states to implement work and community engagement requirements for adults without dependents for at least 80 hours per month.[1] Employment, work programs, education, or community service (or a combination of those activities) would satisfy the requirement.

The work requirements in the House-passed legislation would apply only to individuals between the ages of 19 and 64 without dependents, and the following groups are exempted:

Women who are pregnant or entitled to postpartum medical assistance

Members of Tribes

Individuals who are medically frail (i.e., people who are blind, disabled, with chronic substance use disorder, has serious or complex medical conditions, or others as approved by the Secretary of the US Department of Health and Human Services)

Parents of dependent children or family caregivers to individuals with disabilities

Veterans

People who are participating in a drug or alcoholic treatment and rehabilitation program

Individuals who are incarcerated or have been released from incarceration in the past 90 days

In addition, individuals who already meet work requirements through other programs, such as Temporary Assistance for Needy Families (TANF) or the Supplemental Nutrition Assistance Program (SNAP), would be exempt. However, the House-passed version would make the eligibility verification and work requirements for SNAP more stringent and shift program costs to these states, which would affect cross-functional eligibility. The legislation also includes temporary hardship waivers for natural disasters and areas with an unemployment rate greater than 8 percent (150 percent of the national average).

Though the federal budget package has received a great deal of attention, at least 14 states already have moved forward (see Table 1) in advance of the current federal debate by passing laws and submitting work requirement demonstration requests to the Centers for Medicare & Medicaid Services (CMS).

Table 1. A Review of 2025 States’ Approaches to Work Requirements in Medicaid

Status

State

Population Criteria

Requirements

Exemptions/ Notes

Public Comment

Work Requirement Request Submitted

Arizona

Ages 19−55

80 hours/month

Multiple exemptions; 5-year lifetime limit

Closed

Work Requirement Request Submitted

Arkansas

Ages 19−64; covered by a qualified health plan (QHP)

Data matching to assess whether on track/not on track

No exemptions

Closed

Work Requirement Amendment Request Submitted

Georgia

Ages 19−64; 0-100% FPL

80 hours/month

Already has approval but is requesting reporting be changed from monthly to annually and adding more qualifying activities

Federal comment period open through June 1, 2025

Work Requirement Request Submitted

Ohio

Ages 19−54; expansion adults

Unspecified hours

Limited list of exemptions

Closed

Legislation Passed

Idaho

Ages 19−64

20 hours/week required

Limited list of exemptions

—

Legislation Passed

Indiana

Ages 19−64; expansion adults

20 hours/week required

Limited list of exemptions

—

Legislation Passed

Montana

Ages 19−55

80 hours/month required

Multiple exemptions

—

Ballot Initiative Passed

South Dakota

Expansion adults

—

2024 ballot initiative asking voters for approval for state to impose work requirements for expansion adults passed

—

Legislation Pending

North Carolina

—

—

Pursue requirements that are CMS approvable

—

Work Requirement Request Draft

Iowa

Ages 19−64; expansion adults

100 hours/month required

Limited list of exemptions Separate bill would end expansion if work requirements are withdrawn/ prohibited (80 hr./mo.)

Closed

Work Requirement Request Draft

Kentucky

Ages 19−60; no dependents; enrolled more than 12 months

Connected to employment resources

Multiple exemptions

State comment period open through June 12, 2025

Work Requirement Request Draft

South Carolina

Ages 19−64; 67%−100% FPL

Specified activities (work specific is 80 hours/month)

Limiting participation to 11,400 individuals based upon available state funding

State comment period open through May 31, 2025

Work Requirement Request Draft

Utah

Expansion adults ages 19−59

Register for work, complete an employment training assessment and assigned job training, and apply to jobs with at least 48 employers within 3 months of enrollment

Several exemptions, largely aligned with federal SNAP exemptions

State comment period open through May 22, 2025

Anticipated Waiver Request

Alabama

Non-expansion population

—

Potential to resubmit previous work requirement demonstration request

—

Key Questions to Guide State Policy Decisions

Considerable research and findings from previous Medicaid work requirement initiatives can help prepare policymakers to implement a potential new phase of Medicaid work requirement policies. Some previous findings include the high cost of administration relative to potential savings, the importance of systems that support foundational items like logging an enrollee’s compliance activities and exemptions, as well as developing an efficient appeals process. The Medicaid and CHIP Payment and Access Commission (MACPAC), General Accounting Office, National Institutes for Health, and multiple researchers have published assessments regarding previous experiences that could prove useful in policy making.

HMA experts have experience identifying key issues and considerations, analyzing options, and implementing critical issues and for state leaders and stakeholders who will be responsible for implementing work requirements. Several of these issues are described below and in more detail in the HMA blog, Building State Capacities for Medicaid Work and Community Engagement Requirements.

Exemptions, particularly medical frailty definitions and assessments. The federal government and states will need to identify individuals classified as “medically frail” and make them exempt from the mandates. Medically frail individuals include those with chronic, serious, or complex medical conditions. Various methods can be employed to identify these people.

Developing and streamlining systems and processes to promote continued coverage for eligible individuals. The Medicaid unwinding from the COVID public health emergency taught policymakers lessons about the complexities of Medicaid systems, patient engagement, and reliable methods of member outreach. State Workforce Commissions and Departments of Labor are clear partners, as they manage integrated eligibility systems and data-sharing agreements across programs like SNAP and TANF, which also serve many Medicaid participants. These and other partnerships will need further exploration.

Clinical and utilization data that promote eligibility assessment. Many, but not all, individuals with chronic diseases may be exempt from the requirements. Knowing the health status and chronic conditions of the populations affected and the conditions that qualify people for exemption are variables as implementation questions, like the definition of medically frail, are addressed.

Anticipated need for effective Medicaid managed care engagement in work requirements/community engagement initiatives. Approximately 80 percent of Medicaid expansion enrollees are members of comprehensive managed care organizations (MCOs). States will need to review the scope of existing vendor contracts as well as determine the need for new services, roles, third-party reporting, oversight, and potential exemptions for emergencies. Work requirements can disrupt MCO risk pool stability and care coordination. MCOs have a financial incentive to drive down inappropriate disenrollments and are uniquely positioned to support state responsibilities, including maintenance of up-to-date contact information.

Measuring impact and adapting policies as needed. Dynamic metrics that provide actionable information to federal and state policy makers will support effective oversight and monitoring.

Connect with Us

HMA helps stakeholders—including state agencies and their partners—manage the challenges of implementing new Medicaid or CHIP initiatives, with a focus on ensuring efficient integration and improvements in outcomes. Our teams are adept at developing materials for and supporting stakeholder engagement from design to implementation, which is a critical aspect for work and community engagement initiatives and other potential new eligibility and renewal requirements.

For support tracking federal and state level developments and enhancing your organization’s strategy and preparations for new Medicaid requirements, contact our featured experts below.

It is hard to keep abreast of the changes being made to the healthcare system at the Federal level, and how these changes will impact behavioral health (BH) services. The current reprioritization of funding by the Department of Health and Human Services (HHS) and the proposed changes in the budget bill pending in Congress will significantly reshape Medicaid and critical behavioral health programs. States and local organizations will need to sharpen their understanding of this new funding landscape, so they are able to focus on addressing critical needs for prevention and treatment of mental health and substance use disorders.

Register today – HMA’s Behavioral Health Town Hall, Thursday, May 29 at 12 p.m.

With Federal funding levels in question, States and their stakeholders need to consider how they are funding BH initiatives. We’ll address participant questions and topics we know are top of mind, for example:

What steps can states take to ensure sustainable funding for critical programs? Are states strategically utilizing their Medicaid programs to preserve BH specific program dollars for other purposes? What efficiencies and enabling technologies can organizations adopt to support their mission? How should state and local entities be thinking about the opioid settlement dollars to maximize support for services and initiatives that face uncertain future financial support?

In addition, Congress is debating changes to Medicaid eligibility and funding policies that may result in shifts in key aspects of the program. States can start planning now for changes to their processes and for outreach and education campaigns that will be essential in supporting individuals with mental health and substance use disorder diagnoses. Payers should be planning for changes in enrollment and enrollee risk profiles while providers should expect changes in their payer mix and a need for enhanced collaboration with community organizations. Are there different models that can be pursued to effectively navigate these shifts? How will all of this uncertainty affect the BH workforce? Stakeholders need to be prepared to engage in downside risk arrangements, think about their patient/consumer engagement strategies and integrating digital BH tools that are the focus of the CMS Innovation Center agenda.

You probably have questions that we didn’t even list here. Here is your chance to ask them: Join HMA on Thursday, May 29 at 12 p.m. at a dynamic and interactive Behavioral Health Town Hall where HMA experts Heidi Arthur, Rachel Bembas, Allie Franklin, Teresa Garate, Monica Johnson, and Sara Singleton will be available to answer your questions live on a wide range of critical topics, including:

Federal policy, personnel, and funding changes;

Emerging strategies for addressing social determinants of health, substance use disorder and crisis coordination (including 988);

Leveraging cross-sector partnerships to build ecosystems of care across communities promoting coordination and collaboration;

Behavioral health revenue cycle management and alternative payment models; and

Innovations in addressing workforce shortages, integrated service delivery, digital mental health tools, and best practices for community mental health service delivery.

Whether you’re navigating regulations, searching for new funding, designing service delivery systems, or just trying to understand what happens next, this town hall is your chance to ask questions, share insights, and discuss real-world solutions with industry experts.

This week, in our In Focus section, health IT experts at Leavitt Partners, an HMA Company, review the recently released Request for Information (RFI) from the Centers for Medicare & Medicaid Services (CMS) and the Assistant Secretary for Technology Policy/Office of the National Coordinator for Health (ASTP/ONC), titled Health Technology Ecosystem (CMS-0042-NC). The RFI, published May 16, 2025, signals a renewed federal focus on advancing digital health tools, improving data interoperability, and supporting patient-centered innovation.

Notably, this RFI aligns with the vision laid out in Leavitt Partners’ Kill the Clipboard policy blueprint, developed in collaboration with a broad coalition of healthcare stakeholders. The paper outlines a future in which patients and providers benefit from seamless digital experiences, real-time data exchange, and reduced administrative burden. The RFI reflects many of the same priorities—such as expanding FHIR® Application Programming Interfaces (APIs), improving provider directories, and promoting digital identity solutions—that were highlighted in the paper as essential to modernizing the healthcare system.

Why This RFI Matters

The RFI invites public input on how CMS and ASTP/ONC can strengthen the digital health ecosystem for Medicare beneficiaries. It builds on years of federal investment in interoperability. The agencies are now seeking feedback on how to reduce barriers to data access, promote innovation in digital health products, and align technology with value-based care goals.

This is a pivotal opportunity for stakeholders to shape the future of digital health policy—especially as CMS continues to explore how APIs, digital identity, and patient-facing tools can improve care delivery and outcomes.

Key Themes in the RFI

The RFI is broad in scope, but several themes stand out, including:

Addressing Patient and Caregiver Needs: The RFI asks patients which digital tools would be most helpful to them and their caregivers in managing their health needs, navigating care, and accessing all relevant health information in one place. It asks what features are most needed, what is missing from current apps, and how CMS can support adoption, especially for Medicare beneficiaries with limited digital experience. CMS is exploring how to make more data—beyond claims and clinical data—available through APIs. It also explores the role that CMS should play in reviewing and measuring the real-world impact of these tools on outcomes and costs. They also are considering how to promote the use of secure, standardized digital identity credentials (e.g., Login.gov, ID.me) to streamline patient access. Feedback also is sought on how TEFCA, FHIR APIs, and health information exchanges (HIEs) can better support seamless data exchange.

Provider Adoption of Digital Health Tools: CMS is exploring how to help providers, especially those in rural areas, adopt digital health tools by addressing barriers like workflow integration, data access, and interoperability. CMS is also looking to improve administrative functions like scheduling and intake through third-party apps. In addition, CMS is seeking to understand which FHIR APIs and capabilities are already being supported or utilized in provider systems. They are also interested in understanding how providers might accept standardized digital identity credentials from patients and any challenges that might inhibit its adoption. ASTP/ONC is also seeking information on revisions to the information blocking requirements.

Engaging Payers: The RFI invites payers to share how they can support interoperability and digital innovation, including through the use of APIs, digital identity credentials, and real-time access to clinical quality data. CMS is also interested in how payers can reduce provider burden, support value-based care (VBC), and contribute to a more connected digital health infrastructure. Feedback is requested on TEFCA participation, payer-to-payer data exchange, and the potential for a nationwide provider directory.

Advancing VBC Organizations: The RFI emphasizes the role of digital health in supporting alternative payment models (APMs) and accountable care organizations. CMS is seeking feedback on which digital capabilities are most essential for success in VBC—such as care coordination, quality measurement, and patient engagement—and how certification criteria and data standards can better align with these needs. The agencies are also exploring how to reduce complexity for APM participants while maintaining flexibility and data access.

Enabling Technology Vendors, Data Providers, and Networks: The RFI requests feedback from developers, data aggregators, and HIEs on how to unlock innovation through better access to CMS data, improved API standards, and streamlined certification processes. The RFI asks which technical and policy changes would enable more effective digital health products, recommendations to improve interoperability across networks, and means of supporting the viability of data exchange infrastructure.

Implications for Stakeholders

This RFI is more than a technical exercise; it is a strategic signal. The Trump Administration is maintaining momentum behind VBC and digital transformation. Stakeholders should consider:

Submitting comments to CMS by the June 16, 2025, deadline.

Assessing internal readiness to adopt or develop digital tools that align with CMS’s vision.

Engaging in policy discussions regarding digital identity, data standards, and patient access.

Monitoring related RFIs, including the Food and Drug Administration RFI exploring the potential use of HL7 FHIR standards to support the submission of study data derived from real-world data sources—such as electronic health records, claims, and registries—for regulatory purposes.

Next Steps

Health Management Associates, Inc. (HMA), encourages healthcare organizations to review the RFI and consider how their experiences, innovations, and challenges can inform CMS’s next steps. This is a rare opportunity to influence the infrastructure that will shape digital healthcare for years to come.

For support in drafting comments or understanding how this RFI intersects with your organization’s strategy, contact our Leavitt Partners health IT experts below.

On May 13, 2025, the Centers for Medicare & Medicaid Services (CMS) published its new strategic direction for the CMS Innovation Center. The strategy builds on the lessons of the first 15 years of the Innovation Center, while presenting a significant pivot in policy direction, which emphasizes evidence-based prevention, consumer engagement, and tech-enabled care, while prioritizing financial performance over broad participation.

The new strategy provides high-level direction on the Trump Administration’s vision for the next phase of value-based payment reform under the leadership of CMS Administrator Dr. Mehmet Oz and Innovation Center Director Abe Sutton. They intend to “double down on our commitment to value-based care and take the learnings from the[se] previous investments to build a health system that empowers people to drive and achieve their health goals and Make America Healthy Again.” Notably, the strategy also aligns with goals central to the Trump Administration’s Make America Healthy Again initiative.

This new direction affirms the administration’s commitment to continue advancing value-based care and opens additional opportunities for organizations seeking to enhance the delivery of services that drive positive outcomes. Health Management Associates (HMA), experts will be tracking the implementation of the Innovation Center’s new strategy, including expected forthcoming models, movement toward greater levels of downside risk, and changes to existing models to align with the administration’s priorities. In this article, our experts review the strategy and provide insights on key takeaways for stakeholders.

New Strategy Overview

CMS leaders view the Innovation Center agenda as a framework for accelerating healthy behaviors, leveraging the agency’s authority to test new approaches designed to incentivize and engage stakeholders. According to CMS officials, the Innovation Center “will work expeditiously toward the future of health—building a system in which people are empowered to achieve their health goals and providers are incentivized to compete to deliver high-quality, efficient care and improve the health outcomes of their patients.”

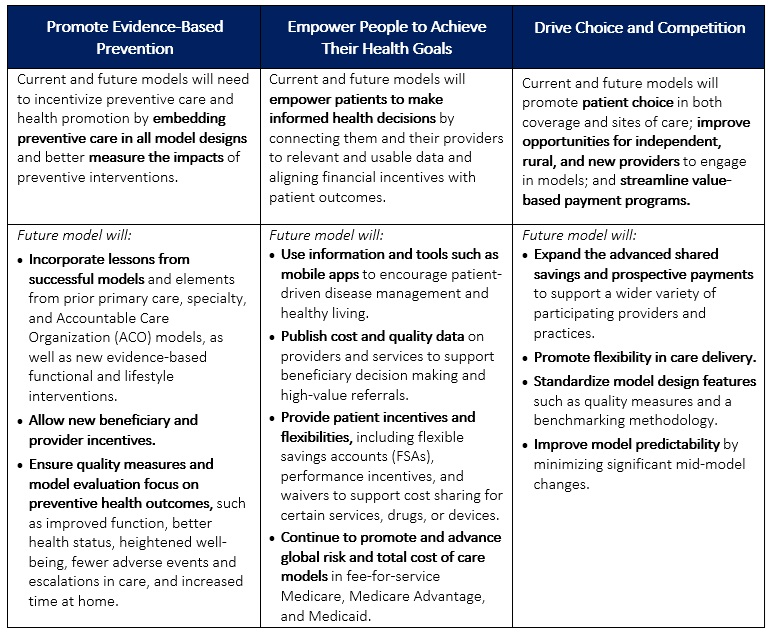

The strategy has three interrelated, foundational pillars:

Promoting evidence-based prevention

Empowering people to achieve their health goals

Driving choice and competition.

Table 1 provides more detail on each pillar.

In addition to the new agenda, CMS released a request for information (RFI) seeking industry input on strategies that can better leverage data and technology to empower consumers. The focus of the RFI aligns with the Innovation Center’s strategic pillars to use tools, information, and processes that better connect people to their health data and allow them to make informed health decisions alongside their providers.

Table 1. CMMI’s Interrelated Strategic Pillars

Takeaways and Considerations

Critical to CMS’s approach is the belief that empowering individuals to make their health decisions—through incentives, better data access, and more flexible options—can lead to better health outcomes and lower overall costs. This shift reflects an evolution in healthcare policy that places greater emphasis on personal accountability and private sector collaboration—a key theme that is emerging across the administration’s policy initiatives.

Consumer Engagement. One of the most notable aspects of the new Innovation Center strategy is the promotion of consumer engagement; it places more focus on direct consumer engagement through education and incentives compared with earlier initiatives. This is one area in which the Innovation Center plans to collaborate with the private sector to develop consumer-facing tools (e.g., mobile apps, nudges toward healthy behaviors, etc.).

The focus on consumer engagement also presents opportunities for organizations to enhance their customer experience. By understanding the needs and preferences of their patients, organizations can tailor their services and care models to better meet those demands. This personalized approach not only improves patient satisfaction, but also drives continuity of care, ultimately contributing to long-term improvements in health.

Data and Technology. The new strategy also emphasizes the importance of data, indicating intentions to better equip organizations that participate in the model with data that can inform decisions and optimize their processes. CMS officials are examining policies and collaborations that will empower private sector organizations, including model participants, researchers, and technology vendors, to develop innovative data-driven solutions to drive efficiencies and improved health.

To that end, the May 16, 2025, Request for Information (RFI) from CMS and the Assistant Secretary for Technology Policy/Office of the National Coordinator for Health (ASTP/ONC), Health Technology Ecosystem (CMS-0042-NC), focuses on Medicare beneficiaries’ use of technology to improve health outcomes. The RFI, which HMA experts analyze here [insert bookmark or link to the other In Focus article] underscores the administration’s intentions of taking “bold steps to modernize the nation’s digital health ecosystem.”

Medicare Advantage. The Innovation Center’s new strategy indicates that stakeholders should expect more models that address Medicare Advantage (MA). The agency stated that “features of a model could include testing changes to payment for MA plans, such as testing the impact of inferred risk scores, regional benchmarks, or changes to quality measures that better align with promoting health.” Additionally, the strategy references a forthcoming specialty-focused longitudinal care model within MA and Medicaid, signaling intentions to drive multi-payer alignment.

Saving Federal Tax Dollars. Another major aspect of the strategy is “protecting federal taxpayers.” This goal reflects a continued emphasis on total cost of care accountability and indicates a more aggressive shift to downside risk. The Innovation Center says it will “require all models to have downside financial risk and require providers to assume some of the financial risk..” Additional provisions of protecting tax dollars include reducing role of state governments in rate setting, simplifying model benchmark methodology, and ensuring “proper and nondiscriminatory provision of funds for health care services.”

What to Watch

For healthcare organizations, the Innovation Center’s agenda signals a need to prioritize consumer-centric models. Hospitals, providers, and insurers should anticipate the following:

Increased focus on preventive care initiatives to align with new model designs

More robust data-sharing and technology requirements, meaning investments in patient-focused digital tools will become essential

New opportunities in MA, given potential payment model innovations affecting plan structures and risk-adjusted reimbursement

Healthcare stakeholders should monitor possible developments related to the strategy.

While details on specific strategies have yet to emerge, the Innovation Center indicated it plans to provide more information on new models, as well as changes to existing models, in the coming months.

The Innovation Center has not provided a goal akin to the previous administration’s effort to have 100 percent of Medicare beneficiaries in accountable care relationships by 2030. It is still unknown whether these goals are forthcoming or if this will remain vague.

Stakeholders are still awaiting clarity on changes to existing models, including key models set to conclude at the end of 2026 (i.e., ACO REACH and Kidney Care Choices).

Strategy language indicates that the agency may develop payment innovation in prescription drugs, medical devices, and technology.

Connect With Us

The Health Management Associates Annual Conference, Adapting for Success in a Changing Healthcare Landscape, October 14-16, 2025, in New Orleans, LA, will feature discussions on how the new strategy is reshaping the healthcare system and care delivery for patients, particularly the opportunities to revisit provider contracts with MA plans and to integrate technology to advance the prevention of chronic conditions and achieve population health goals.

For more information about the opportunities and considerations the Innovation Center agenda presents for your organization, contact HMA’s featured experts below.

This week, our third In Focus section highlights the national 988 Suicide and Crisis Lifeline, the three-digit number for individuals in need of behavioral health crisis support. The 988 Lifeline is composed of 200-plus contact centers across the country, which connect people to trained counselors to deescalate crises, provide behavioral health resources, or connect individuals to an in-person responder. Supported by federal legislation to help create a nationwide, standardized, easy to remember 3-digit number, the program is still in its early stages, having been established three years ago this coming July.

In this article, Health Management Associates (HMA) experts provide important context about the 988 Lifeline and future policy direction and suggests actions state leaders can take to enhance use of this critical resource.

988 Lifeline: A Product of Coordinated Collaboration

The story of how the 988 Lifeline was created is an example of long-term advocacy and innovation that demonstrates how a solution needs to combine the state and local decisionmakers with federal policy and support. People experiencing a mental health crisis, thoughts of suicide, or concerns about substance misuse should receive the appropriate local response to seek support or care.

Prior to the 988 Lifeline, individuals experiencing a behavioral health crisis may have contacted 911 and, therefore, not always received the most appropriate response for their unique needs. In some situations, 911 responders—typically law enforcement, emergency medical services, or hospital emergency departments—are ill-equipped to direct people experiencing a behavioral health crisis. Trained behavioral health professionals responding to an individual experiencing a crisis is the appropriate intervention at most points of access. Increased diversion from 911 calls to 988 when an individual is experiencing a behavioral health crisis is an expected long-term outcome.

The federal government’s role is to continue to support the work to enhance the 988 Lifeline, but there’s so much more that needs to happen to increase education and awareness in states, localities, and Tribal nations. They still need support in building out their systems.

State Initiatives Strengthening the 988 Lifeline

Since the launch of the 988 Lifeline in July 2022, 50 percent of the states have approved some type of appropriation or some type of legislation to further cement 988 in their local communities. Some states have established trust funds or implemented 988 cell phone fees similar to what 911 does to provide financial support. Other states have established committees to study and support 988 implementation, building out the various components of a true coordinated crisis system of care.

HMA experts have identified strategic and operational recommendations to support this ongoing work, including:

Be intentional about having the right people at the table where decisions are made, including voices with lived experience and people who are part of the policy-making process. Establishing this formal, standardized 988 system enables local communities to better allocate resources in crisis situations. In most cases, the contact with the 988 Lifeline is the best intervention to ensure people get the support or resources needed to resolve or deescalate the crisis.

When designing a crisis system in a community, think about prevention and what happens when the crisis is over. Crisis systems established on a poor behavioral health foundation will fail. Stakeholders and decisionmakers should continue building out their systems by remembering that the entire continuum of care—from crisis to ongoing support—is needed.

Identify the data that are needed to tell the story about the value of the 988 Lifeline and crisis care systems. Anecdotes are essential and should be paired with data, especially when ongoing funding is needed.

Where Is the 988 Lifeline Headed?

It is likely to take decades to generate greater awareness about the 988 Lifeline, to have interoperability between 911/988, to ensure every person in the country has access to the service no matter their zip code, and to see a fully transformed behavioral health crisis system will take decades to accomplish. The collaboration between federal, state, territories, Tribal nations, and local communities is pivotal to reaching these goals.

While we are at the beginning phases of this work, much has been done that should be celebrated. The 988 Lifeline has transformed how we as a nation talk about behavioral health and suicide prevention. Still, we as a collective have work ahead to achieve the vision of transforming the behavioral health crisis care system.

Connect with Us

Health Management Associates (HMA) is hosting a live, interactive event on Thursday, May 29, 2025. [The Ask the Experts: Behavioral Health Town Hall https://www.healthmanagement.com/insights/webinars/ask-hma-experts-behavioral-health-town-hall/ ] will explore the latest developments in behavioral health—from policy shifts and funding trends to real-world solutions for service delivery, workforce challenges, and system design. HMA and Leavitt Partners, an HMA Company, experts will be on hand to answer participant questions and share insights about 988 and other topics:

Policy and funding updates at the federal level

Innovative approaches to crisis response, 988 implementation, and substance use services

Revenue cycle improvements and evolving payment models

Strategies to strengthen the workforce, integrate care, and leverage digital mental health tools

For more information about 988 systems and effective practices emerging in crisis care, contact Monica Johnson, Managing Director for Behavioral Health. Prior to joining HMA, Ms. Johnson, Managing Director for Behavioral Health, was the director of the 988 & Behavioral Health Crisis Coordinating Office at the Substance Abuse and Mental Health Services Administration—the federal agency that leads public health efforts to advance the behavioral health of the nation.