This week, our In Focus section focuses on a March 12, 2025, announcement from the Centers for Medicare & Medicaid Services (CMS) regarding CMS Innovation Center programs under the new Administration. After reviewing the Innovation Center’s model portfolio, CMS has elected to discontinue four models ahead of their original end dates: Maryland Total Cost of Care (TCOC), Primary Care First (PCF), End-Stage Renal Disease (ESRD) Treatment Choices (ETC), and Making Care Primary (MCP). The agency also intends to downsize the Integrated Care for Kids Model (InCK) and forgo the launch of two drug pricing initiatives. According to the announcement, CMS appears to be moving forward with other Innovation Center models, but signaled upcoming modifications to models to align with Administration priorities as well as new model announcements.

The following is a discussion of CMS’s announcement and what it may signal about the agency’s commitment to value-based care, key takeaways regarding the four terminated models, and how stakeholders should be preparing to engage with the Innovation Center on current or future models while we await additional details.

CMS’s Strategic Decision

As part of CMS’s recent announcement about the model terminations, the agency reaffirmed its support for testing models that reduce program spending while maintaining or improving quality of care. Furthermore, the Innovation Center “plans to announce a new strategy based on guiding principles to make Americans healthier by preventing disease through evidence-based practices, empowering people with information to make better decisions, and driving choice and competition.” These statements should be seen as a commitment to using the Innovation Center to test new approaches to delivering care but with an expectation that the models will need to demonstrate significant cost and quality improvements as outlined in its statutory authority. According to CMS, the cancellation of these models is projected to save an estimated $750 million.

Because CMS said it may modify additional models in the future, it is reasonable to expect those changes will focus on achieving a higher level of savings or to see savings earlier in the demonstration, as well as aligning model design with the priorities of this Administration. The potential modifications could have an impact on the number of model participants, length of model testing, and financial arrangements, especially with regard to risk and quality improvement approaches.

Models Ending

CMS Innovation Center models are time-limited pilots meant to help the agency test which types of interventions lead to cost savings and improved quality and, if successful, can be scaled on a nationwide basis. These models are evaluated regularly, and CMS has the authority to modify or terminate models if they fall short of the statutory criteria.

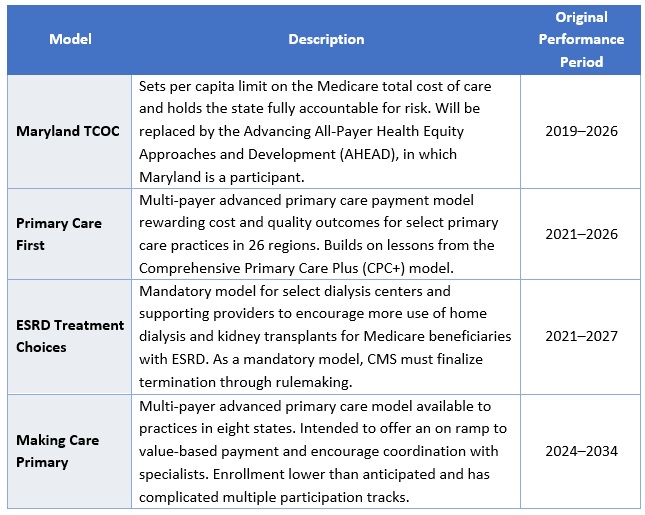

The four models the agency plans to terminate are ending for various reasons (e.g., underwhelming performance, forthcoming replacement by successor model, etc.) and, as stated above, the decision should not be seen as a retreat from value-based care, but rather as a signal regarding Administration priorities for Innovation Center models. For example, despite terminating PCF and MCP prior to their original end dates, CMS reaffirmed its support for primary care as a “foundational component of the Center’s strategy” and that future primary care payment reforms will focus on approaches that produce savings. CMS also noted that ending these models early offers an opportunity to move beneficiaries into more permanent programs, such as the Medicare Shared Savings Program (MSSP)—CMS’ flagship accountable care initiative—even going so far as to direct readers to the MSSP’s calendar year 2026 application.

CMS plans to advise current model participants of other options for advanced primary care payment before the models conclude by December 31, 2025. Table 1 presents information on the models scheduled for early termination.

Table 1: Models Ending by December 31, 2025

In addition, the agency is considering options to reduce the size of the InCK model and will no longer pursue the Medicare Two Dollar Drug List and Accelerating Clinical Evidence models. The latter two initiatives were included in a Biden Executive Order on drug pricing and were not implemented. Notably, CMS did not end another drug pricing Innovation Center model, Cell and Gene Therapy Access (CGT) Model.

Innovation Center’s New Strategic Plan

CMS also announced that it will soon release its new vision for the Innovation Center, based on principles designed to improve Americans’ health through evidence-based practices, empower individuals with decision-making information, and drive competition.

This vision will set the direction for future value-based care initiatives and reflect the leadership changes within CMS, including the anticipated confirmation of Mehmet Oz, MD, as CMS Administrator and the appointment of Abe Sutton, as the new Director of the Innovation Center. Mr. Sutton’s experience with value-based care—especially during his time as an advisor to then Department of Health and Services Secretary Alex Azar under the first Trump Administration and his subsequent private sector leadership of value-based companies—positions him to play a key role in shaping CMS’s future efforts.

Stakeholder Considerations

Stakeholders have several critical operational decisions and strategic considerations to address, including:

- Transition Support. Participants in the models scheduled to end must assess their options for sustaining certain components of the payment models without Innovation Center support. This effort will require strategic, operational, and financial analyses to make informed decisions.

- Evaluation of Other Programs. While the Innovation Center has signaled its intentions of announcing new models, participants should not wait to evaluate options. The Administration plans to prioritize permanent payment programs and will continue to support the MSSP as CMS’s permanent model for accountable care organizations (ACOs). Stakeholders interested in participating in the MSSP in 2026 must act quickly to assess their organizational readiness, conduct financial modeling of their potential benchmark and performance, evaluate potential partners, and prepare for the application process. Both existing and new ACOs should be exploring their strategies and infrastructures to optimize performance.

- Adapting to Changes in Existing Models. While CMS discontinued select models, it is likely the agency will make additional changes to the Center’s continuing models. These revisions likely will reflect President Trump’s executive actions and policy priorities. With the increased focus on cost savings, CMS may choose to spend fewer resources on model implementation, including participant support and model engagement.

- Policy and Market Intelligence. Monitoring the dynamic federal policy landscape and seeking strategic advisory support can help stakeholders navigate and inform potential future federal and state alternative payment model opportunities. Stakeholders should expect that existing and potential new models may have stricter requirements and higher expectations for financial risk. Providers, states, insurers, and other interested stakeholders should monitor public and private sector developments to understand the landscape and evolving opportunities.

Connect with Us

Health Management Associates, Inc. (HMA), is home to alternative payment model experts that can assist stakeholders in responding to changes in Innovation Center models and the agency’s approaches and to help prepare for participation in future model opportunities. Additionally, HMA produces a weekly briefing focused on public and private sector VBP-related news. To learn more about how HMA can support your organization’s federal engagement and innovation strategy, contact our experts below.