HMA is pleased to welcome new experts to our family of companies in April 2023.

Jed Abell – Consulting Actuary Wakely

Jed Abell is a professional health insurance actuary with over 20 years of experience focusing on Medicare Advantage, Part D, and commercial employer group plans.

Surah Alsawaf – Senior Consultant HMA

Surah Alsawaf is a senior consultant with experience in creating and implementing regulatory strategies and workflows, conducting reviews and audits, and leading cross-functional teams to complete complex deliverables.

Elrycc Berkman – Consulting Actuary Edrington

Elrycc Berkman is experienced in Medicaid managed care rate development including managed long-term services and supports (MLTSS) and program of all-inclusive care for the elderly (PACE) rate development.

Monica Bonds – Associate Principal HMA

Monica Bonds is an experienced managed care professional with over 15 years of experience working in large and diverse organizations.

Yucheng Feng – Senior Consulting Actuary Wakely

Yucheng Feng has over 15 years of experience providing actuarial support for Medicare Advantage clients, including bid preparation, reserve, actuarial analytics and providing strategic recommendations. Read more about Yucheng.

Melanie Hobbs – Associate Principal HMA

Melanie Hobbs is an accomplished healthcare executive, consultant, and thought leader specializing in Medicare, Medicaid, and Special Needs Plans (SNPs).

Daniel Katzman – Consulting Actuary Wakely

Daniel Katzman is experienced in Medicare Advantage bid pricing and modeling as well as claims trend analytics and affordability/cost-savings analysis. Read more about Daniel.

Supriya Laknidhi – Principal HMA

Supriya Laknidhi has over 20 years of experience in the healthcare industry and a proven track record in driving growth and innovation for companies.

Donald Larsen – Principal HMA

Dr. Donald Larsen is a C-suite physician executive with over 30 years of experience spanning complex academic medical centers, community health systems, acute care hospitals, and research institutes.

Ryan McEntee – Senior Consultant Wakely

Ryan McEntee is an experienced managed care executive specializing in strategic leadership within Medicare Advantage plans. Read more about Ryan.

Nicole Oishi – Principal HMA

Nicole Oishi has over 30 years of experience in senior leadership roles as a healthcare clinician and executive.

This week our In Focus section reviews President Joseph R. Biden’s 2023 State of the Union Address (SOTU) to Congress. The President highlighted specific actions that Congress, and the Administration have taken over the last two years to advance his health care priorities.

During his first SOTU address in 2022, President Biden announced the creation of a “Unity Agenda”, which included priority policy areas with potential for bi-partisan support. The President highlighted several steps the Administration has taken to advance the “Unity Agenda” including:

The bipartisan effort to enact the Mainstreaming Addiction Treatment (MAT) Act, which removed the federal requirement for practitioners to have a waiver (known as the X-waiver) to prescribe medications, like buprenorphine, for the treatment of opioid use disorder

The Cancer Moonshot announcements for almost 30 new programs, policies, and resources to close the screening gap, tackle environmental exposure, decrease preventable cancers, advance cutting-edge research, support patients and caregivers, and more.

Addressing mental health needs through the expansion of Certified Community Behavioral Health Clinics and launch of the 988-suicide prevention hotline.

In his SOTU and accompanying White House materials, the President also proposed new policies and initiatives to further advance his health care agenda. These actions include a combination of issues that would require Congressional approval as well as actions regulatory agencies can already advance. Congress and the Administration are expected to build on previous bipartisan achievements to tackle the nation’s dual crises with addiction and mental health.

Notably, the policies outlined in the SOTU foreshadow an active regulatory agenda over the next 18 months as the Administration seeks to solidify key aspects of the President’s health care agenda ahead of the next Presidential election.

The Administration’s planned actions include the following:

Opioids

Calling on Congress to pass legislation to permanently schedule all illicitly produced fentanyl-related substances into Schedule I.

SAMHSA will provide enhanced technical assistance to states who have existing State Opioid Response funds, and will host peer learning forums, national policy academies, and convenings with organizations distributing naloxone beginning this spring.

By this summer, the Federal Bureau of Prisons will ensure that each of their 122 facilities are equipped and trained to provide in-house medication-assisted treatment (MAT).

This spring CMS will provide guidance to states on the use of federal Medicaid funding to provide health care services—including treatment for people with substance use disorder—to individuals in state and local jails and prisons prior to their release. California is the first state to receive approval for a similar initiative.

Mental Health

CDC plans to launch a new campaign to provide a hub of mental health and resiliency resources to health care organizations in better supporting their workforce.

The Department of Education (ED) will announce more than $280 million in grants to increase the number of mental health care professionals in high-need districts and strengthen the school-based mental health profession pipeline.

HHS and ED will issue guidance and propose a rule to make it easier for schools to provide health care to students and more easily bill Medicaid for these services.

The Administration is scheduled to propose new mental health parity rules this spring.

HHS will improve the capacity of the 988 Lifeline by investing in an expansion of the crisis care workforce; scaling mobile crisis intervention services; and developing additional guidance on best practices in crisis response.

HHS also plans to promote interstate license reciprocity for delivery of mental health services across state lines.

HHS intends to increase funding to recruit future mental health professionals from Historically Black Colleges and Universities and to expand the Minority Fellowship Program.

The Department of Veterans Affairs (VA), working with HHS and Defense, will launch a program for states, territories, Tribes and Tribal organizations to develop and implement proposals to reduce suicides in the military and among veterans.

VA will also increase the number of peer specialists working across VA medical centers to meet mental health needs

Cancer Moonshot

The President called on Congress to reauthorize the National Cancer Act to overhaul cancer research and to extend the funding for biomedical research established in the 21st Century Cures Act.

The Administration will take steps to ensure that patient navigation services are covered by insurance. This could require legislation depending on which type on insurance an individual has.

Health care costs

Urging Congress to pass legislation to cap insulin prices in all health care markets. Expanding the $35 insulin cap to commercial markets will require the 60 votes in the Senate.

Home and community services

Working with Congress to approve legislation to ensure seniors and people with disabilities can access home care services and to provide support to caregivers.

HMA and HMA companies are closely monitoring these federal policy developments. We can assist healthcare stakeholders in responding to the immediate opportunities and challenges that arise and contextualize these actions for longer-term strategic business and operational decisions.

If you have questions about these or other federal policy issues and how they will impact your organization please contact Andrea Maresca ([email protected]) or Liz Wroe ([email protected]).

Join us on Monday, March 6, 2023, at the Fairmont Chicago, Millennium Park, for “Healthcare Quality Conference: A Deep Dive on What’s Next for Providers, Payers, and Policymakers,” where Lee Fleisher, MD, chief medical officer and director of CMS’ Center for Clinical Standards and Quality, will deliver the keynote titled A Vision for Healthcare Quality: How Policy Can Drive Improved Outcomes.

HMA’s first annual quality conference will provide organizations the opportunity to “Focus on Quality to Improve Patients’ Lives.” Attendees will hear from industry leaders and policy makers about evolving health care quality initiatives and participate in substantive workshops where they will learn about and discuss solutions that are using quality frameworks to create a more equitable health system.

In addition to Fleisher, featured speakers will executives from ANCOR, CareOregon, Commonwealth Care Alliance, Council on Quality and Leadership, Intermountain Healthcare, NCQA, Reema Health, Kaiser Permanente, United Hospital Fund, and others.

Working sessions will provide expert-led discussions about how quality is driving federal and state policy, behavioral health integration, approaches to improving equity and measuring the social determinants of health, integration of disability support services, stronger Medicaid core measures, strategies for Medicare Star Ratings, value-based payments, and digital measures and measurement tools. Speakers will provide case studies and innovative approaches to ensuring quality efforts result in lasting improvements in health outcomes.

“What’s different about this conference is that participants will engage in working sessions that provide healthcare executives tools and models for directly impacting quality at their organizations,” said Carl Mercurio, Principal and Publisher, HMA Information Services.

View the Full Agenda

Early Bird registration ends January 30. Visit the conference website for complete details or contact Carl Mercurio at 212-575-5929/[email protected]. Group rates and sponsorships are available.

The holiday season is grounded in gratitude. At HMA, we are grateful for successful partnerships that have fueled change to improve lives.

We are proud to be trusted advisors to our clients and partners. Their success is our success. In 2022 our clients and partners made significant strides tackling the biggest healthcare challenges, seizing opportunities for growth and innovation, and shaping the healthcare landscape in a way that improves the health and wellness of individuals and communities.

HMA partnered with the Colorado Department of Human Services to support the planning and implementation of a new Behavioral Health Administration (BHA). HMA provided technical research and extensive stakeholder engagement, drafted models for forming and implementing the BHA, employed an extensive change management approach, and created a detailed implementation plan with ongoing support. Today the BHA is a cabinet member-led agency that collaborates across agencies and sectors to drive a comprehensive and coordinated strategic approach to behavioral health.

Wakely Consulting Group, an HMA Company, was engaged to support the launch of a Medicare Advantage (MA) joint venture partnership between a health plan and a provider system. Wakely was responsible for preparing and certifying MA and Medicare Part D (PD) bids, a highly complex, exacting, and iterative effort. The Wakely team quickly became a trusted advisor and go-to resource for the joint venture decision makers. The joint venture has driven significant market growth over its initial years, fueled by a competitive benefit package determined by the client product team.

In 2021 Indiana Governor Eric Holcomb appointed a 15-member commission to assess Indiana’s public health system and make recommendations for improvements. The Indiana Department of Health (IDOH) engaged HMA to provide extensive project management and support for six workstreams. HMA prepared a draft report summarizing public input as well as research findings and recommendations. The commission’s final report will form the basis of proposed 2023 legislation, including proposals to substantially increase public health service and funding across the state.

In early 2022 HMA and Wakely Consulting Group, an HMA Company, assisted multiple clients with their applications to participate in the new CMS ACO REACH model. The purpose of this model is to improve quality of care for Medicare beneficiaries through better care coordination and increased engagement between providers and patients including those who are underserved. The team tailored their support depending on each client’s needs. The application selection process was highly competitive. Of the 271 applications received, CMS accepted just under 50 percent. Notably, nine out of the 10 organizations HMA and Wakely supported were accepted into the model.

HMA, and subsidiaries The Moran Company and Leavitt Partners, were selected by a large pharmaceutical manufacturer to analyze the current pipeline of innovative therapies, examine reimbursement policies to assess long-term compatibility with the adoption of innovative therapies and novel delivery mechanisms, and make policy recommendations to address any challenges identified through the process. The project equipped the client with a holistic understanding of future potential impacts and actions to address challenges in a detailed pipeline analysis of innovative therapies.

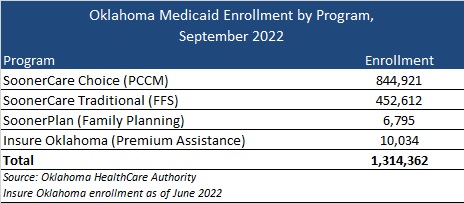

This week, our In Focus reviews the Oklahoma Medicaid managed care SoonerSelect Program request for proposals (RFP) and the SoonerSelect Children’s Specialty Program RFP released by the Oklahoma Health Care Authority (OHCA) on November 10, 2022.

Background

Oklahoma currently does not have a fully capitated, risk-based Medicaid managed care program. The majority of the state’s 1.3 million Medicaid members are in SoonerCare Choice, a Primary Care Case Management (PCCM) program in which each member has a medical home. Other programs include SoonerCare Traditional (Medicaid fee-for-service), SoonerPlan (a limited benefit family planning program), and Insure Oklahoma (a premium assistance program for low-income people whose employers offer health insurance).

Prior efforts to transition to Medicaid managed care have encountered roadblocks, starting in 2017 with a failed attempt to move aged, blind, and disabled members to managed care.

More recently, in June 2021, the Oklahoma Supreme Court struck down a planned transition of the state’s traditional Medicaid program to managed care, ruling that the Oklahoma Health Care Authority does not have the authority to implement the program without legislative approval.

Contracts had been awarded to Blue Cross Blue Shield of Oklahoma, Humana, Centene/Oklahoma Complete Health, and UnitedHealthcare. Centene/Oklahoma Complete Health also won an award for the SoonerSelect Children’s Specialty Program.

In May 2022, Governor Kevin Stitt signed a new Oklahoma law to implement Medicaid managed care by October 1, 2023.

SoonerSelect RFP

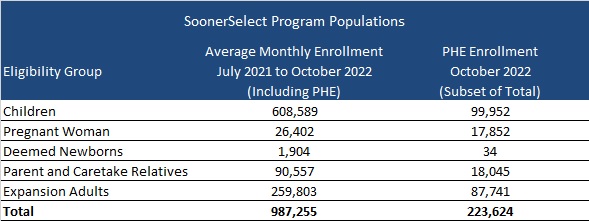

Oklahoma will award contracts to at least three entities to provide medical, behavioral, and pharmacy coverage to nearly one million eligible children, pregnant women, newborns, parents and caretake relatives, and the expansion population. However, enrollment in these populations is expected to drop following the end of the public health emergency (PHE).

At least one of the contracts may be awarded to a provider-led entity (PLE). PLEs would need to provide proof that a majority of their ownership is held by Oklahoma Medicaid providers or the majority of the governing body is composed of individuals who have experience serving Medicaid members and are licensed providers. PLEs would also be able to bid on urban regions if the PLE agrees to develop statewide readiness within a timeframe set by the OHCA. If no PLEs meet OHCA standards, Oklahoma can choose not to award a PLE.

Goals of the program will include:

Improve health outcomes for Medicaid members and the state as a whole

Ensure budget predictability through shared risk and accountability

Ensure access to care, quality measures, and member satisfaction

Ensure efficient and cost-effective administrative systems and structures

Ensure a sustainable delivery system that is a provider-led effort and that is operated and managed by providers to the maximum extent possible.

Timeline

Proposals will be due on February 8, 2023, and contract implementation is scheduled for October 1, 2023. The contract is expected to run through June 30, 2024, with five, one-year options.

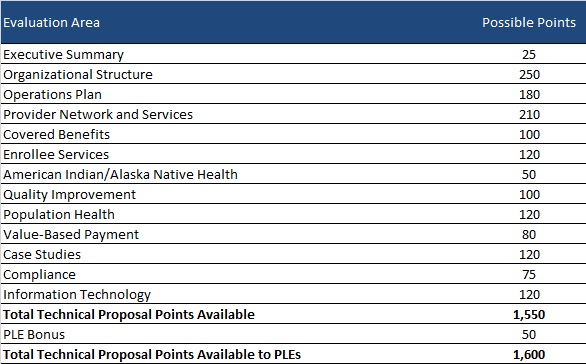

Evaluation

Bidder’s technical proposals will be scored out of a total 1550 points. OHCA will award PLEs an additional 50 points for qualifying, bringing the total up to 1600 points. OHCA may also choose to conduct oral presentations for an extra total of 50 points.

SoonerSelect Children’s Specialty Program RFP

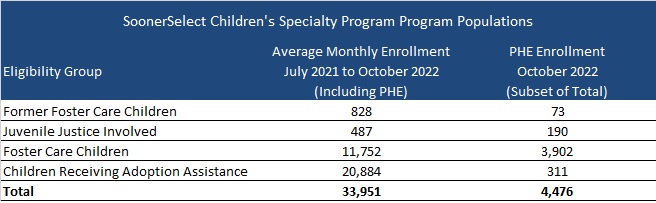

Oklahoma will select one of the awarded SoonerSelect plans for a separate statewide contract to provide comprehensive integrated health coverage to foster children, former foster children up to 25 years of age, juvenile justice-involved children, and children receiving adoption assistance. Contract terms will be the same as the main SoonSelect procurement, running from October 1, 2023, through June 30, 2024, with five one-year renewal options.

This week, our In Focus section reviews highlights and shares key takeaways from the 22nd annual Medicaid Budget Survey conducted by The Kaiser Family Foundation (KFF) and Health Management Associates (HMA). Survey results were released on October 25, 2022, in two new reports: How the Pandemic Continues to Shape Medicaid Priorities: Results from an Annual Medicaid Budget Survey for State Fiscal Years 2022 and 2023 and Medicaid Enrollment & Spending Growth: FY 2022 & 2023. The report was prepared by Elizabeth Hinton, Madeline Guth, Jada Raphael, Sweta Haldar, and Robin Rudowitz from the Kaiser Family Foundation and by Kathleen Gifford, Aimee Lashbrook, and Matt Wimmer from HMA; and Mike Nardone. The survey was conducted in collaboration with the National Association of Medicaid Directors (NAMD).

This survey reports on policies in place or planned for FY 2022 and FY 2023, including state experiences with policies adopted in response to the COVID-19 pandemic. The conclusions are based on information provided by the nation’s state Medicaid Directors.

Key Report Highlights

In the following sections, we highlight a few of the major findings from the reports. This is a fraction of what is covered in the 50-state survey reports, which include significant detail and findings on policy changes and initiatives related to delivery systems, health equity, benefits, telehealth, provider rates and taxes, and pharmacy. The reports also look at the opportunities, challenges, and priorities facing Medicaid programs.

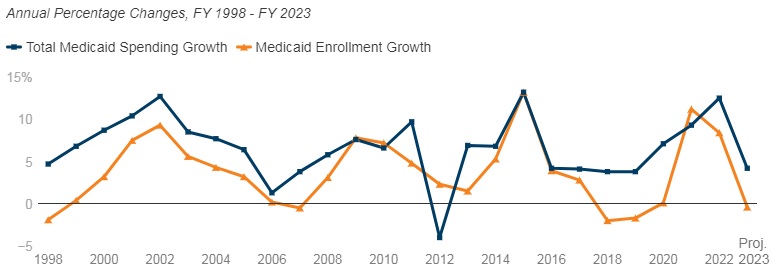

Medicaid Enrollment and Spending Growth

The COVID-19 pandemic created significant implications for Medicaid. During this time, Medicaid enrollment has reached record highs due to the Families First Coronavirus Response Act (FFCRA), enacted in March 2020, which authorized a 6.2 percentage point increase in the federal match rate, or Federal Medical Assistance Percentage (FMAP), retroactive to January 1, 2020, and until the Public Health Emergency (PHE) ends. The increase was available to states that meet certain “maintenance of eligibility” (MOE) requirements. Since the survey, the PHE was extended to mid-January 2023, somewhat delaying the anticipated effects described in survey.

Medicaid enrollment growth slowed to 8.4 percent in FY 2022, after a sharp increase in FY 2021 (11.2 percent). Almost all responding states reported that the MOE continuous enrollment requirement was the most significant factor driving FY 2022 enrollment growth. Responding states expect Medicaid enrollment growth to decline (-0.4 percent) in FY 2023, based largely on the assumption that the PHE and the related MOE requirements would end by mid-FY 2023. States anticipate larger declines as Medicaid redeterminations and renewals resume.

In FY 2022, total Medicaid spending is expected to reach a peak growth of 12.5 percent, with enrollment growth as the primary driver. For FY 2023, total spending growth is expected to slow to 4.2 percent, assuming slower enrollment growth after the unwinding of the PHE. State Medicaid spending grew by 9.9 percent in FY 2022 and is projected to increase by 16.3 percent in FY 2023 once enhanced federal fiscal relief expires. If the PHE is extended, state spending increases and enrollment decreases that states anticipated for FY 2023 could occur later.

Figure 1 – Percent Change in Medicaid Spending and Enrollment, FY 1998-23

SOURCE: FY 2022-2023 spending data and FY 2023 enrollment data are derived from the KFF survey of Medicaid officials in 50 states and DC conducted by Health Management Associates, October 2022. 49 states submitted survey responses by Oct. 2022; state response rates varied across questions. Historic data reflects growth across all 50 states and DC and comes from various sources.

Delivery Systems

Capitated managed care remains the predominant delivery system for Medicaid in most states. Forty-six states operated some form of Medicaid managed care (managed care organizations (MCOs) and/or primary care case management (PCCM)). Forty-one states contracted with risk-based MCOs. Of these, only Colorado and Nevada did not offer MCOs statewide. Only five states – Alaska, Connecticut, Maine, Vermont, and Wyoming – lacked a comprehensive Medicaid managed care model.

Thirty-four states, including Distrct of Columbia, operate MCOs only, five states operate PCCM programs only, and seven states operate both MCOs and a PCCM program.

Twenty-seven states contracted with one or more PHPs to provide Medicaid benefits, including behavioral health care, dental care, vision care, non-emergency medical transportation (NEMT), and long-term services and supports (LTSS).

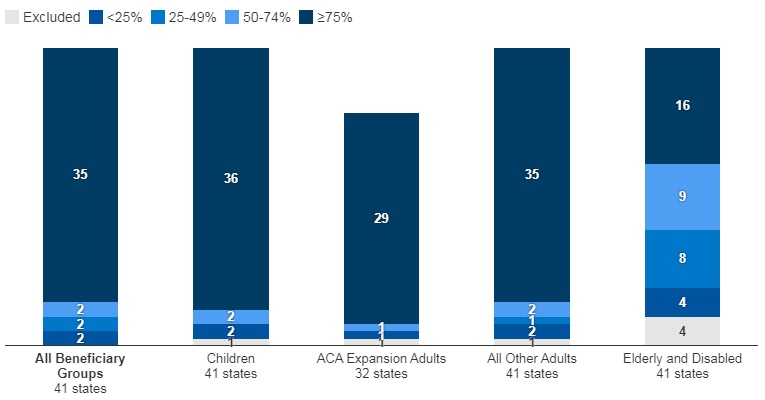

Of the forty-one states that contracted with MCOs, 35 reported that 75 percent or more of their Medicaid beneficiaries were enrolled in MCOs as of July 1, 2022.

Figure 2 – MCO Managed Care Penetration Rates for Select Groups of Medicaid Beneficiaries as of July 1, 2022

SOURCE: KFF survey of Medicaid officials in 50 states and DC conducted by HMA, October 2022.

Medicaid Managed Care and Delivery System Changes

California, Missouri, Nevada, New Jersey, and New York reported expanding mandatory MCO enrollment for targeted populations.

Missouri and Ohio reported introducing specialized managed care programs for children with complex needs.

California, Nevada, and Tennessee indicated that they were carving in certain long-term services and supports (LTSS) into their managed care programs.

California and Ohio reported carving out pharmacy services in FY 2022 or FY 2023, respectively. The District of Columbia carved out emergency medical transportation from its MCO contracts in FY 2022.

Maine, North Carolina, Oregon, and Washington reported changes to their PCCM programs.

Virginia plans to implement Cardinal Care in FY 2023, merging the state’s two existing managed care programs: Medallion 4.0 (serving children, pregnant individuals, and adults) and Commonwealth Coordinated Care Plus (CCC Plus) (serving seniors, children and adults with disabilities, and individuals who require LTSS).

Forty-one states reported at least one specified delivery system and payment reform initiative (e.g. Patient-Centered Medical Home (PCMH), ACA Health Homes, Accountable Care Organization (ACO), Episode of Care Initiatives, All-Payer Claims Database (APCD)).

Health Equity

Twenty-five states reported using at least one specified strategy to improve race, ethnicity, and language (REL) data completeness. Of the 45 responding states, 16 states reported requiring MCOs and other applicable contractors to collect REL data, 12 states reported that eligibility, renewal materials, and/or applications explain how REL data will be used and/or why reporting these data are important, nine states reported linking Medicaid enrollment data with public health department vital records data, and eight states reported partnering with one or more health information exchanges (HIEs) to obtain additional REL data for Medicaid enrollees.

Twelve of 44 responding states reported at least one financial incentive tied to health equity in place in FY 2022. The vast majority of these incentives were in place in managed care arrangements (11 of 13). Within managed care arrangements, states most commonly reported linking or planning to link capitation withholds, pay for performance incentives, and/or state-directed provider payments to health equity-related quality measures. Only two states (Connecticut and Minnesota), reported a FFS financial incentive in FY 2022. Five additional states report plans to implement financial incentives linked to health equity in FY 2023.

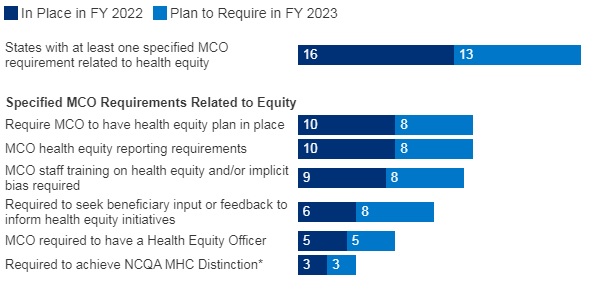

Sixteen of 37 responding MCO states reported at least one specified health equity MCO requirement in place in FY 2022. The number of MCO states with at least one specified health equity MCO requirement in place is expected to grow significantly in FY 2023, from 16 to 25 states. Examples of MCO requirements to address health equity include having a health equity plan, designating a Health Equity Officer, and staff training on health equity and/or implicit bias.

Figure 3 – MCO Requirements to Address Health Equity, FYs 2022-23

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; n=37 states.

Benefits

Thirty-three states reported new or enhanced benefits in FY 2022 and 34 states are adding or enhancing benefits in FY 2023. Two states reported benefit cuts or limitations in FY 2022 and no states reported cuts or limitations in FY 2023.

Figure 4 – Select Categories of Benefit Enhancements or Additions, FYs 2022-23

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; Arkansas and Georgia did not respond.

Behavioral Health Services. States reported service expansions across the behavioral health care continuum, including institutional, intensive, outpatient, home and community-based, and crisis services. States reported addressing SUD outcomes, including coverage of opioid treatment programs, peer supports, and enhanced care management. At least ten states are expanding coverage of crisis services, which aim to connect Medicaid enrollees experiencing behavioral health crises to appropriate community-based care, including mobile crisis response services and crisis stabilization centers.

Pregnancy and Postpartum Services. In April 2022, a temporary option under ARPA to extend Medicaid postpartum coverage from 60 days to 12 months took effect. In addition to the states that took advantage of this eligibility change, some states are enhancing coverage of pregnancy and post-partum services. Nine states (California, District of Columbia, Illinois, Maryland, Michigan, New Mexico, Nevada, Rhode Island, and Virginia) are adding coverage of services provided by doulas and seven states (Alabama, Delaware, Illinois, Maryland, Ohio, Oregon, and Vermont) are investing in the implementation or expansion of home visiting programs.

Preventive Services. Sixteen states reported expansions of preventive care in FY 2022 or FY 2023. For example, seven states are expanding services to prevent and/or manage diabetes, such as continuous glucose monitoring. Other reported preventive benefit enhancements relate to asthma services, vaccinations, and genetic testing and/or counseling.

Services Targeting Social Determinants of Health. Many states reported new and expanded benefits targeting social determinants of health. Twelve states reported new or expanded housing-related supports, as well as other services and programs tailored for individuals experiencing homelessness or at risk of being homeless.

Dental Services. Nine states are adding comprehensive adult dental coverage, while additional states report expanding specific dental services for adults.

Telehealth

Most states have or plan to adopt permanent Medicaid FFS telehealth expansions that will remain in place even after the pandemic, though some are considering guardrails on such policies. Nearly all responding states that contract MCOs reported that changes to FFS telehealth policies would also apply to MCOs.

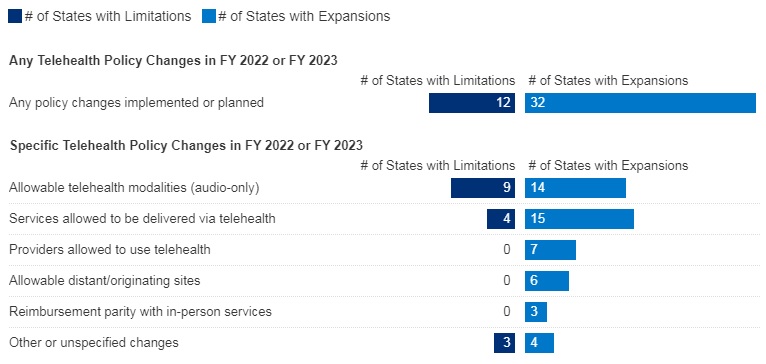

Figure 5 – Changes to FFS Medicaid Telehealth Policy, FY 2022 or FY 2023

SOURCE: KFF survey of Medicaid officials conducted by HMA, October 2022; n=48 states.

Nearly all responding states added or expanded audio-only telehealth coverage in Medicaid in response to the COVID-19 pandemic. Twenty-eight states reported that they newly added audio-only coverage while 19 states expanded existing coverage. Nearly all states reported audio-only coverage of mental health and substance use disorder (SUD) services. States least frequently reported audio-only coverage of home and community-based services (HCBS) and dental services. Two states (Mississippi and Wyoming) reported no coverage of audio-only telehealth for the services in question.

Telehealth utilization by Medicaid enrollees has been high during the pandemic but has decreased and/or leveled off more recently. States noted that telehealth utilization trends over time correspond to COVID-19 outbreaks, with higher utilization during COVID-19 surges and lower utilization when case counts are lower. In general, states reported that telehealth utilization was projected to continue at higher levels than before the pandemic, at least for some service categories.

Thirty-seven states (out of 47 responding) reported that behavioral health services were among those with the highest utilization. Additionally, a majority of states reported high utilization of evaluation and management (E/M) services and/or other physician/qualified health care professional office/outpatient services, including primary care.

States reported ACA expansion adults as one of the groups most likely to use telehealth (about one-third of responding states), followed by children and individuals with disabilities (each identified by about one-sixth of responding states).

Concerns regarding services delivered via telehealth included the quality of diagnoses, whether audio-only telehealth may be less effective, and inadequate access.

Key issues that may influence future Medicaid telehealth policy decisions include analysis of data, state legislation and federal guidance, and cost concerns.

Provider Rates and Taxes

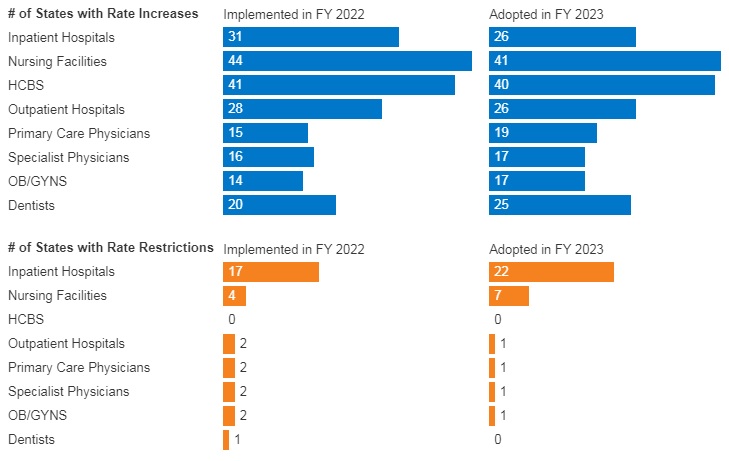

In FY 2022, all 49 responding states reported implementing rate increases for at least one category of provider and 19 states reported implementing rate restrictions. In FY 2023, 48 states reported at least one planned rate increase and the number of states planning to restrict rates increased to 25 states.

States reported rate increases for nursing facilities and home and community-based services (HCBS) providers more often than other provider categories. The survey also found an increased focus on dental rates with about half of reporting states (20 in FY 2022 and 25 in FY 2023) reporting implementing or plans to implement a dental rate increase

Figure 6 – FFS Provider Rate Changes Implemented in FY 2022 and Adopted for FY 2023

SOURCE: KFF survey of Medicaid officials in 50 states and DC conducted by HMA, October 2022.

States continue to rely on provider taxes and fees to fund a portion of the non-federal share of Medicaid costs. All states but Alaska have at least one provider tax or fee in place. Thirty-eight states had three or more provider taxes in place in FY 2022 and eight other states had two provider taxes in place.

The most common Medicaid provider taxes in place in FY 2022 were taxes on nursing facilities (46 states), followed by taxes on hospitals (44 states), intermediate care facilities for individuals with intellectual disabilities (33 states), and MCOs (18 states).

Three states (Alabama, Mississippi, and Wyoming) reported plans to add new ambulance taxes in FY 2023.

Pharmacy

Most states that contract with MCOs report that the pharmacy benefit is carved into managed care (34 out of 41 states that contract with MCOs). Six states (California, Missouri, North Dakota, Tennessee, Wisconsin, and West Virginia) report that pharmacy benefits are carved out of MCO contracts as of July 1, 2022. California was the latest to carve out pharmacy benefits as of January 1, 2022. Two states (New York and Ohio) report plans to carve out pharmacy from MCO contracts in state FY 2023 or later.

In FY 2022, Kentucky began contracting with a single PBM for the managed care population. Louisiana and Mississippi report that they will require MCOs to contract with a single PBM designated by the state in FY 2023 and FY 2024, respectively.

Seven states (Alabama, Arizona, Colorado, Massachusetts, Michigan, Oklahoma, and Washington) have value-based arrangements (VBAs) in place with one or more drug manufacturers.

More than half of responding states reported newly implementing or expanding at least one initiative to contain prescription drug costs in FY 2022 or FY 2023.

Six states (Florida, Kentucky, Massachusetts, Maryland, Nebraska, Nevada) reported recently implemented or planned policies to prohibit spread pricing or require pass through pricing in MCO contracts with PBMs.

Key Opportunities, Challenges, and Priorities in FY 2023 and Beyond

When asked to identify the top challenges for FY 2023 and beyond, Medicaid directors listed the following:

The unwinding of PHE emergency measures and the resumption of redeterminations.

Expiration of emergency authorities.

Lasting focus on COVID-19, including vaccinations, long-COVID, decreased utilization of preventive care services, and future emergency preparedness.

Medicaid directors stated that future priorities shaped by COVID-19 include:

Health equity.

Specific populations and service categories, including behavioral health, long-term services and supports, and maternal and child health.

Health care workforce challenges.

Payment and delivery system initiatives and operations.

IT system modernization.

Social determinants of health.

Medicaid directors note that COVID-19 has presented both new opportunities and challenges and has also shifted and shaped ongoing Medicaid priorities.

Health Management Associates (HMA) has a rich history of serving the healthcare infrastructure needs of Native American and Alaska Native communities – through healthcare IT support, clinical governance for change management, culturally competent stakeholder engagement, and revenue cycle management that implements an approach that is tailored to the provider and payer entities that deliver care in Native American and Alaska Native communities.

American Indian and Alaska Native (AI/AN) people experience disproportionately poorer health status compared to Americans as a whole. AI/ANs born today have a life expectancy that is 5.5 years less than the national average for all races. HMA has expertise with healthcare issues that uniquely impact American Indian and Alaska Native populations and is experienced in addressing these issues through American Indian and Alaska Native leadership engagement that is culturally sensitive and respectful.

Case Studies

Examples of HMA’s work with tribal health providers include:

HMA provided training and technical assistance to Skokomish Indian Tribal Health Center in Skokomish, Washington. This support includes the provision of clinical oversight services by one of HMA’s clinicians as Interim Medical Director.

HMA: (1) assessed the Tribal Health Center’s billing practices and assisted in the development of a procurement and contract with a new third-party billing vendor; (2) developed a screening and intervention program for medications for addiction treatment (MAT) of opioid and alcohol use disorders, including training for providers and administrative and medical staff; (3) established policies and procedures to support the clinic to move to a primary care medical home model of care, including development of a back office manual and trainings to clinic staff and providers; and (4) provided technical assistance to the Tribal Health Center as it developed telehealth programs for both video visits and remote patient monitoring (RPM), including development of policies and procedures for maintaining operations during emergencies, procedures and workflow approaches for working with IT vendors and potential purchase and implementation of a new electronic health record.

HMA conducted a feasibility assessment to determine how best Fort Belknap Tribal Health Department could take over administration of behavioral health services through a 638 contract with the Indian Health Service (IHS) agency. To do this, HMA conducted a review of select documentation, contracts, and data sets, including clinical and financial data. Through site visits, HMA conducted focus groups and interviews with tribal, IHS, and community stakeholders. HMA also provided research of other tribal behavioral health programs and interviews with tribes successfully delivering comprehensive behavioral health services.

HMA provided consultation regarding integration of behavioral health into primary care sites, sharing expertise and advice on privacy and confidentiality regulations and integrated care, how to manage during the transition from traditional behavioral health to integrated care, ideas for including medical family therapy more broadly in patient care, and the implementation of patient assessments.

The Montana Healthcare Foundation (MHCF) convened tribal health care leaders to develop shared priorities to jointly pursue with the Montana Department of Public Health and Human Services (DPHHS) and the Legislature. HMA was engaged by MHCF to help the group assess implementation options related to the Centers for Medicare and Medicaid Services’ (CMS) revised interpretation of the 100 percent federal match for state Medicaid programs for American Indian Medicaid enrollees for services. HMA proposed options for how DPHHS can use the new match funding to support IHS and tribal health facilities as they implement these new processes and support shared priorities. Priorities identified by the tribal health leaders included operational and policy issues such as improving health information technology capacity; identifying opportunities to compact aspects of health care delivery from IHS; and improving clinic operations through business management training.

HMA served as the independent evaluator for Montana Office of Public Instruction (OPI) Substance Use and Mental Health Services Administration (SAMHSA) Tribal Systems of Care Evaluation. The five-year evaluation assesses the impact of High-Fidelity Wraparound services being provided to American Indian students in schools on six tribal reservations throughout the state. Evaluation activities include tracking quantitative data to measure progress toward grant goals and tracking qualitative data to assess impact of wraparound activities through key informant interviews, small group listening sessions, and site visits. Evaluation findings are regularly reported to SAMHSA and presented locally to key stakeholders.

Montana Tribally Operated Substance Use Disorder (SUD) Continuum of Care Concept Brief

HMA worked in coordination with the American Indian Health Leaders (AIHL) workgroup, a group made up of leadership from Montana’s seven tribes representing tribal health departments and urban Indian health centers, to develop a SUD Continuum of Care Concept brief, describing potential approaches for design and financing of a jointly tribally operated SUD treatment facilities. This work was conducted through a contract with Montana Healthcare Foundation.

Montana Tribally Operated Substance Use Disorder Continuum of Care

HMA provides technical assistance and facilitation and consulting expertise to support the development of a statewide joint tribally operated SUD Continuum of Care. HMA facilitated discussions with AIHL and Chemical Dependency Center (CD) directors. HMA provided subject matter expertise on the various design options available based on American Society of Addiction Medicine (ASAM) service needs criteria as well as analysis support. HMA is also providing consulting support on financial and operational planning for the development of new facilities. This work could include methods for short-term and long-term forecasting and scenario modeling, identification, and negotiation of capital and operational financing for construction and start-up phase, and technical assistance on revenue cycle best practices to ensure satisfactory patient experience and sustainable revenue. This work is being conducted through a contract with the MHCF.

Health Policy and Advocacy

HMA consultants have worked with the following organizations associated with American Indian health policy and advocacy issues:

A tribally driven non-profit organization with a mission of improving health outcomes for American Indians and Alaska Natives through a health policy focus at the Washington state level. AIHC works on behalf of the 29 federally recognized Indian tribes and two urban Indian health organizations.

An Alaska Native-owned, nonprofit health care delivery and advocacy organization serving nearly 65,000 Alaska Native and American Indian people living in Anchorage, Matanuska-Susitna Borough and 55 rural villages. Southcentral Foundation and the Alaska Native Tribal Health Consortium own and manage the Alaska Native Medical Center that serves the entire Alaska Native and American Indian population in the state.

Engaged in many areas of Indian health, including legislation, policy analysis, health promotion and disease prevention, as well as data surveillance and research. The Northwest Portland Area Indian Health Board (NPAIHB) is a non-profit tribal advisory organization serving the forty-three federally recognized tribes of Oregon, Washington, and Idaho.

A non-profit organization located on the Apsáalooke (Crow) Reservation in Montana whose mission is to improve the health of individuals on the Crow Indian Reservation and outlying areas through community-based projects that empower communities to assess and address their own unique health-related challenges.

For more information about HMA’s Native American and Alaska Native support services, contact [email protected].

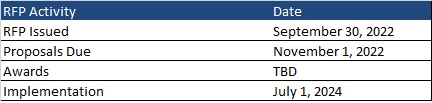

This week, our In Focus section reviews the Mountain Health Promise request for proposals (RFP) released by the West Virginia Department of Health and Human Resources on September 30, 2022, for specialized Medicaid managed care for children and youth in foster care.

Mountain Health Promise RFP

The selected managed care organization (MCO) will provide physical and behavioral health services to children and youth in the foster care system, individuals receiving adoption assistance, youth formerly in foster care up to age 26 who aged out of foster care while on Medicaid in the state of West Virginia, and children eligible under the children with serious emotional disorders (CSED) waiver. Potential expansions could include, but are not limited to, children at risk for foster care placement and the family of youth in crisis. Additionally, the MCO will act as an administrative services organization (ASO) and provide statewide administrative services for all individuals accessing socially necessary services (SNS).

Some of the goals of the program include:

Enhance coordination and access to services

Enhance quality of care and minimize barriers for youth and families/improve access to treatment

Reduce fragmentation and offer seamless continuity of care

Improve health and social outcomes for youth and impacts on families

Help reduce the number of children removed from the home and reduce lengths of stay per episode of care through increased family-centered care that provides necessary and coordinated services to all members of the family

Decrease children involved with the juvenile justice and corrections systems

Reduce out-of-home and out-of-state placements

Develop new or enhance existing services, such as children’s mobile crisis response (CMCR), inState Psychiatric Residential Treatment Facilities (PRTF) to reduce the need for out-of-state placements, and intensive home-based treatment

Physical and behavioral health services will be reimbursed through a Medicaid per member per month (PMPM) capitation payment. For SNS administration, the Bureau for Social Services (BSS) will provide a fixed monthly rate. The PMPM capitation rate will not include carved out SNS costs.

It is encouraged, but not required, that the MCO subcontract with regional child welfare organizations, residential mental health treatment facilities (RMHTFs), and organizations that provide home and community-based services for children with serious emotional disorders to assist in the care coordination of services for this population.

Market

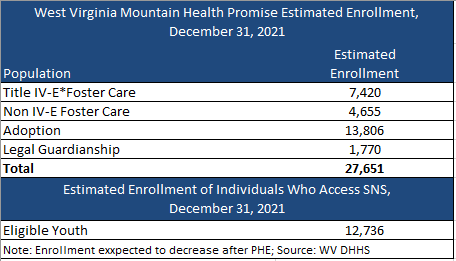

There are nearly 28,000 individuals currently enrolled in Mountain Health Promise, with about 13,000 eligible for SNS. Enrollment, however, is expected to decrease following the end of the Public Health Emergency (PHE). CVS Health/Aetna is the incumbent plan. Aetna had contracted with Kepro to serve as the ASO for SNS.

Timeline

Proposals are due November 1, 2022. The contract is anticipated to run from July 1, 2024, through June 30, 2025, with three one-year options.

Evaluation

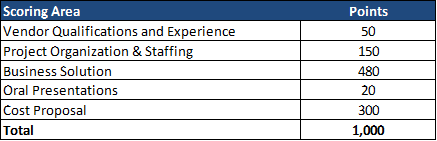

The winning MCO will be chosen based on the highest score of a possible total 1,000 points. The technical evaluation will be a total of 700 of 1,000 points. Cost represents 300 of 1,000 total points.

This week, our In Focus section looks at the current federal policy landscape and trends and the legislative outlook for the remainder of 2022 and beyond. Experts from HMA continue to monitor developments in this area and provide additional updates as more information becomes available.

Legislative Branch

To date in 2022, Congress passed multiple comprehensive bills, including the Inflation Reduction Act (IRA), which was signed by President Biden on August 16, 2022. The IRA extends Exchange plan premium tax subsidies through 2025, institutes an out-of-pocket drug spending cap for Medicare beneficiaries, expands Medicare, Medicaid, and CHIP coverage protections for certain vaccines, allows Medicare to negotiate drug prices, and implements a penalty payment in the Medicare program for prescription drug prices that rise faster than the rate of inflation.

Going forward, stakeholders have an extensive list of immediate Medicare payment issues for Congress to tackle while lawmakers continue to consider fundamental reforms to the program. Priorities include mitigating Medicare payment reductions scheduled for 2023; providing relief to address inflationary cost pressures; extending the 5 percent bonus for physicians participating in Advanced Alternative Payment Models (APMs), which expires at the end of 2022 for Accountable Care Organizations (ACOs); and permanently expanding telehealth access and payment policies after the federal COVID-19 public health emergency (PHE) declaration expires. Many stakeholder groups are also urging the Senate to act on the House-approved legislation, Improving Seniors Timely Access to Care Act (H.R. 3173), to reform Medicare Advantage prior authorization policies.

Congress did not include major Medicaid proposals in the Inflation Reduction Act. Medicaid stakeholders want Congress to revisit certain Medicaid policies in one of the remaining legislative vehicles this year. Significant proposals of interest include closing the Medicaid coverage gap in non-expansion states, enhanced coverage for justice involved populations, and expanding support for home and community-based services (HCBS). States and some stakeholders have also sought more certainty in the timing and guardrails for ending the COVID-19 Public Health Emergency (PHE) policy that links enhanced federal Medicaid funding with the requirement for continuous Medicaid coverage.

Congressional leaders and key influencers are laying the groundwork for 2023 legislative efforts. Congress is likely to defer action on most major legislative issues until after the November mid-terms, including finalizing federal fiscal year 2023 funding for most departments. A change in control of either or both chambers of Congress will likely lead to greater scrutiny of the Biden Administration’s health care policies and actions, which have largely gone untested by this Congress.

Executive Branch

Executive orders have been a major source in driving federal workstreams in 2022. Following enactment of several major bills, implementation responsibilities have shifted to the Executive Branch and stakeholders will have multiple opportunities to further shape and support new programs, regulatory and policy updates, and funding opportunities. Executive orders passed include:

Advancing Racial Equity and Support for Underserved Communities, January 21, 2021

Promoting Competition in the American Economy, July 9, 2021

Improving the Customer Experience, December 13, 2021

Access to Affordable, Quality Health Coverage, April 5, 2022

Equality for LGBTQI Individuals, June 15, 2022

Protecting Access to Reproductive Healthcare Services, July 8, 2022

The Administration will continue to address COVID-19 emergency needs while stepping up efforts to support states, health plans, providers and other stakeholders as they prepare for the post-COVID environment. The current PHE declaration expires October 13, 2022, but since HHS has not signaled that it plans to end the PHE in October, another extension is likely until January 11, 2023. The next advance notification about the end of the PHE would be Nov. 12, 2022. Once the PHE declaration expires, numerous Medicare and Medicaid, TANF, and SNAP flexibilities will end, including Medicaid’s continuous coverage requirement and certain telehealth flexibilities, among others. Additional federal agency guidance is expected to support post-PHE transitions.

The Centers for Medicare & Medicaid Services (CMS) plans to advance new policy direction across several service and delivery areas, including strengthening long-term services and support and innovations via Section 1115 demonstration programs. CMS is expected to approve transformational 1115 proposals in additional states. Several state proposals focus, in part, on building capacity among local and regional entities and community-based organizations to address social drivers of health. Many state proposals are also strengthening behavioral health delivery systems and seek to meet enrollees’ urgent behavioral health needs. Additionally will want to monitor CMS’ regulatory efforts to align and strengthen managed care and fee-for-service (FFS) access and network adequacy policies as well as updates to the agency’s in lieu of services policy in managed care programs.

The Administration is also expected to accelerate work on its top policy priorities and regulatory agenda in advance of the next Presidential election, and this will require ongoing engagement among health care stakeholders.

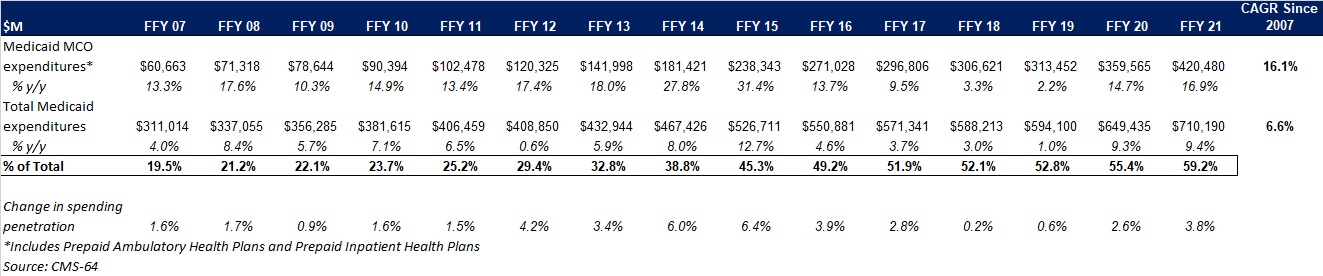

This week, our In Focus section reviews preliminary 2021 Medicaid spending data collected in the annual CMS-64 Medicaid expenditure report. After submitting a Freedom of Information Act request to the Centers for Medicare & Medicaid Services (CMS), HMA received a draft version of the CMS-64 report that is based on preliminary estimates of Medicaid spending by state for federal fiscal year (FFY) 2021. Based on the preliminary estimates, Medicaid expenditures on medical services across all 50 states and six territories in FFY 2021 was nearly $710.2 billion, with over 59 percent of the total now flowing through Medicaid managed care programs. In addition, total Medicaid spending on administrative services was $30.8 billion, bringing total program expenditures to $741 billion.

Total Medicaid Managed Care Spending

Total Medicaid managed care spending (including the federal and state share) in FFY 2021 across all 50 states and six territories was $420.5 billion, up from $359.6 billion in FFY 2020. This figure includes spending on comprehensive risk-based managed care programs as well as prepaid inpatient health plans (PIHPs) and prepaid ambulatory health plans (PAHPs). PIHPs and PAHPs refer to prepaid health plans that provide only certain services, such as dental services or behavioral health care. Fee-based programs such as primary care case management (PCCM) models are not counted in this total. Below we highlight some key observations:

Total Medicaid managed care spending grew 16.9 percent in FFY 2021. The rate of growth has been increasing since the COVID-19 pandemic. Prior to 2020, the rate had decelerated since FFY 2016.

Managed care spending growth was due in large part to the COVID-19 pandemic and the resulting higher Medicaid enrollment.

In terms of dollars, the increase in Medicaid managed care spending from FFY 2020 to FFY 2021 was $60.9 billion, compared to $46.1 billion from FFY 2019 to FFY 2020.

Medicaid managed care spending has increased at a compounded annual growth rate (CAGR) of 16.1 percent since FFY 2007, compared to a 6.6 percent growth in total Medicaid spending.

Compared to FFY 2020, Medicaid managed care spending as a percent of total Medicaid spending in FFY 2021 increased by 3.8 percentage points to 59.2 percent.

Figure 1: Medicaid MCO Expenditures as a Percentage of Total Medicaid Expenditures FFY 2007-2021 ($M)

As the table below indicates, 69.4 percent of FFY 2021 spending came from federal sources, which is 12 percentage points higher than the pre-Medicaid expansion share in FFY 2013, and 1.8 percentage points higher than FFY 2020.

Figure 2: Federal vs. States Share of Medicaid Expenditures, FFY 2013-2021 ($M)

State-specific Growth Trends

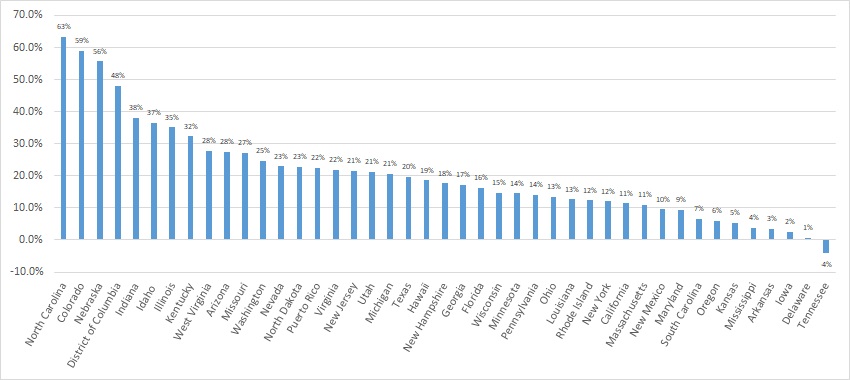

Forty-five states and territories report managed care organization (MCO) spending on the CMS-64 report, including Alaska, which utilizes a PIHP/PAHP model exclusively. Oklahoma is expected to implement a Medicaid managed care program in 2023. Of the remaining 44 states and territories that contract with risk-based MCOs, average MCO spending in FFY 2021 increased 17.6 percent. On a percentage basis, North Carolina experienced the highest year-over-year growth in Medicaid managed care spending at 63.3 percent due to the implementation of its risk-based Medicaid managed care program. Among states with more mature programs, Colorado experienced the fastest growth in FFY 2021 at 59 percent, followed by Nebraska at 55.6 percent.

The chart below provides additional detail on Medicaid managed care spending growth in states with risk-based managed care programs in FFY 2021.

Figure 3: Medicaid Managed Care Spending Growth on a Percentage Basis by State FFY 2020-21

Source: CMS-64; *Note: Not all states are included in the table.

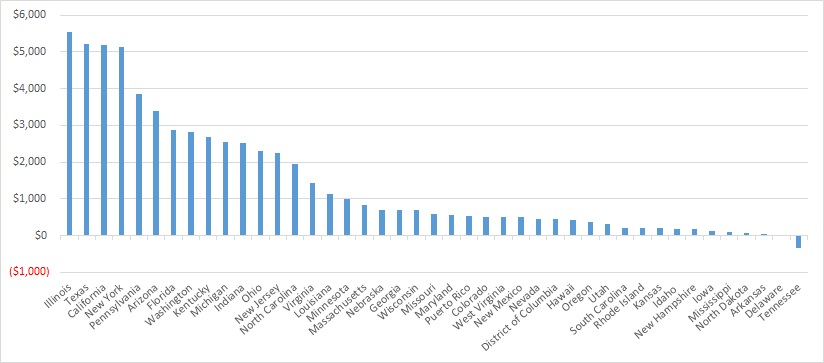

Looking at year-over-year spending growth in dollar terms, Illinois experienced the largest increase in Medicaid managed care spending at $5.5 billion. Other states with significant year-over-year spending increases in dollar terms included Texas ($5.2 billion), California ($5.2 billion), and New York ($5.1 billion). The chart below illustrates the year over year change in spending across the states.

Figure 4: Medicaid Managed Care Spending Growth on a Dollar Basis by State FFY 2020-21 ($M)

Source: CMS-64; *Note: Not all states are included in the table.

The percentage of Medicaid expenditures directed through risk-based Medicaid MCOs increased by more than five percentage points in 14 states from FFY 2020 to FFY 2021. The managed care spending penetration rate rose 13.4 percentage points in the District of Columbia, 9.7 percentage points in Indiana, 9.5 percentage points in Nebraska, 9.2 percentage points in North Carolina, and 9.1 percentage points in Illinois.

Figure 5: Medicaid MCO Expenditures as a Percentage of Total Medicaid Expenditures in States with a 5 percent or Greater Increase from FFY 2020 to FFY 2021 ($M)

Source: CMS-64

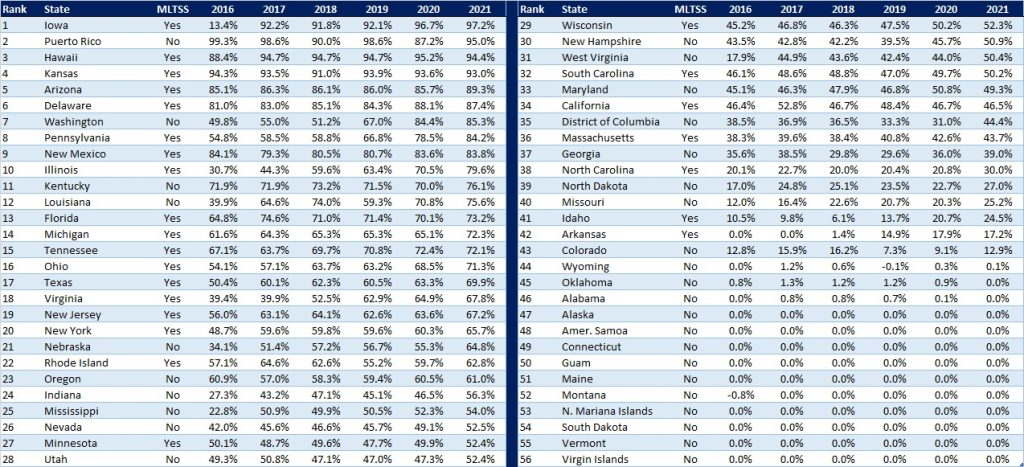

The table below ranks the states and territories by the percentage of total Medicaid spending through Medicaid MCOs. Iowa reported the highest percentage at 97.2 percent, followed by Puerto Rico at 95 percent, and Hawaii at 94.4 percent.

We note that in many states, there are certain payment mechanisms which may never be directed through managed care, such as supplemental funding sources for institutional providers and spending on retroactively eligible beneficiaries. As a result, the maximum achievable penetration rate in each state will vary and may be below that achieved in other states. The Medicaid managed care spending penetration rate is greatly influenced by the degree to which states have implemented managed long-term services and supports (MLTSS) programs.

Figure 6: Medicaid MCO Expenditures as a Percent of Total Medicaid Expenditures, FFY 2016-2021

Non-MCO Expenditures

Despite the rapid growth in Medicaid managed care over the last 10 years, program spending still represented approximately 59 percent of total Medicaid expenditures in FFY 2021. So where is the remaining fee-for-service (FFS) spending (approximately $291 billion) going? First, as noted above, there are many states/territories with Medicaid managed care programs in which certain beneficiaries or services are carved-out of the program, and these are typically associated with high-cost populations. The total amount of non-MCO spending in the 44 states with risk-based managed care in FFY 2021 was $260.4 billion. Assuming an average “full penetration” of 85 percent of total Medicaid spending, then HMA estimates that an additional $221 billion in current FFS spending could shift to a managed care model just in the states that already employ managed care for a subset of services and/or beneficiaries.

Thirteen states/territories did not utilize a comprehensive risk-based managed care model in FFY 2020. In general, the 13 states/territories that do not utilize managed care today are smaller states. Oklahoma, with $5.3 billion in Medicaid spending is expected to shift to risk-based Medicaid managed care in 2023. Total Medicaid spending across all 13 non-managed care states/territories was $29.8 billion. The 13 states/territories that did not employ a risk-based comprehensive Medicaid managed care model in FFY 2021 were Alabama, Alaska, American Samoa, Connecticut, Guam, Maine, Montana, Northern Mariana Islands, Oklahoma, South Dakota, Vermont, Virgin Islands, and Wyoming.

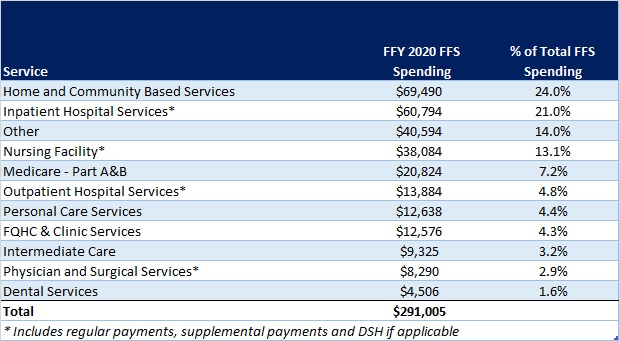

In terms of spending by service line, the largest remaining FFS category is home and community-based services at $69.5 billion, which accounts for 24 percent of FFS spending. Inpatient hospital services represent 21 percent of FFS spending at $60.8 billion.

Figure 7: Fee-for-Service Medicaid Expenditures by Service Line, FFY 2021

While the CMS-64 report provides valuable detail by service line for all FFS expenditures, it does not capture how spending directed to Medicaid MCOs is allocated by category of service. Therefore, it is not possible to calculate total MCO spending by service line, a challenge that will only intensify as more spending runs through MCOs.