Amy Bassano is a Managing Director at Health Management Associates and a nationally recognized Medicare policy expert. In this episode of Vital Viewpoints on Healthcare, we unpack the complexities of Medicare innovation and examine where the program is headed next. Drawing on decades of experience—including her leadership at the Center for Medicare and Medicaid Innovation—Amy breaks down what makes value-based care so complex, why scaling successful models is harder than it sounds, and how Medicare Advantage continues to reshape the healthcare landscape. She also discusses how financial incentives, regulatory constraints, and the urgent need for system-wide efficiency are shaping the next chapter of Medicare policy. This conversation offers practical insights for policymakers, providers, and advocates navigating the future of one of the nation’s most essential programs.

252 Results found.

The Medicare Advantage VBID Program Is Ending: Here’s What All Plans Can Do to Prepare for What’s Next

This week, our second In Focus article addresses the transition to end the Medicare Advantage Value-Based Insurance Design (VBID) model, which launched in 2017 and subsequently has been expanded with bipartisan support. This model was designed to promote flexible benefit design, reduce cost barriers, and enhance care for targeted populations, especially dual eligibles and individuals with chronic conditions. In December 2024, however, the Centers for Medicare & Medicaid Services (CMS) announced that the model would be terminated by the end of 2025, citing unmitigable costs to the Medicare Trust Funds, totaling more than $4.5 billion across 2021 and 2022 alone.

Despite its popularity and effectiveness in improving medication adherence and addressing social determinants of health, CMS concluded that the cost trajectory was unsustainable within the parameters of the Innovation Center’s mandate.

The end of the VBID model is not the end of innovation in Medicare Advantage (MA); rather, it is a strategic inflection point. Plans that approach this transition with a proactive, data-driven lens will be best positioned to maintain competitive advantage, compliance, and member trust. This article reviews critical steps VBID plans should be taking and how Medicare Advantage Organizations (MAOs) and their partners can best prepare for future opportunities.

Pain Points and Key Strategic Decisions for MAOs

As plans prepare for a post-VBID world, they face a series of complex trade-offs—especially those with Dual Eligible Special Needs Plans (D-SNPs) that had $0 drug cost sharing under VBID. With the end of CMS’s drug cost offset in the initial coverage phase, MAOs will need to determine whether and how to absorb those costs through alternative mechanisms. In addition, plans will need to make important decisions regarding their other VBID benefits, namely, whether to discontinue or transition them to the special supplemental benefits for the chronically ill (SSBCI) program. MAOs should consider the following key strategic decisions:

- Offer an Enhanced Alternative (EA) or Basic Alternative (BA) Part D Plan: To replicate $0 cost sharing, MAOs would need to use EA or BA plan designs with $0 deductibles and $0 copays across all tiers—an expensive move and potentially untenable investment for many.

- Tier-Specific Buy-Downs (T1/T2): Some plans may consider buying down T1 and T2 copays to $0, a much less costly approach. Others may consider moving key T2 drugs to T1, while keeping T1 copays at $0 to protect access and using non-zero dollar T2 copays to limit costs.

- Competitive Alignment Considerations: MAOs offering broader cost-sharing reductions (e.g., $0 copays on both T1 and T2 drugs) may experience undesirable shifts in enrollment patterns depending on how competitors structure their formularies and benefit designs. MAOs should consider competitive parity and attempt to maintain a balanced benefit structure that aligns with market norms.

- Transferring VBID Benefits to SSBCI: Some benefits—like non-health-related transportation, healthy foods, and general supports for living—could migrate to the SSBCI program. But SSBCI has strict eligibility, documentation, and operational requirements, calling for nuanced workflows and cross-departmental coordination.

Action Plan: What MAOs Should Be Doing Now

To navigate this transition successfully, teams of experts at Wakely, a Health Management Associates, Inc. (HMA) Company, are already working with VBID stakeholders to evaluate multiple transition scenarios. Our experts recommend that MAOs take the following actions:

What to Watch: Future Innovation in Medicare Advantage

Though VBID is ending, the innovation landscape is far from static. With the new Trump Administration and the return of Abe Sutton—a VBID expansion advocate—appointed as Director of the CMS Innovation Center, our experts are closely monitoring the potential for a revised version of VBID or similar models. Stakeholder advocacy could influence how CMS prioritizes the next wave of innovation. Plans should consider engaging in dialogue now to shape what happens next.

Connect with Us

Wakely is embedded in MA strategy and policy. Wakely and HMA teams are working with clients to evaluate multiple transition scenarios, helping them optimize value, protect Star Ratings, and preserve member satisfaction during this pivotal shift, while also supporting targeted policy engagement efforts to ensure their perspectives are reflected in future CMS and Innovation Center decision making.

Our joint capabilities bring together:

- Actuarial modeling expertise to quantify cost and risk impacts of design alternatives

- Regulatory insight to ensure compliance with CMS requirements

- Operational support to help you implement SSBCI programs efficiently

- Market strategy consulting to align your plan offerings with local competition and enrollment goals

- Policy advocacy to help clients engage in the conversation around what comes next after VBID

To connect on additional questions contact our featured experts below.

FY 2026 Medicare Hospital Inpatient Proposed Regulation Signals Several Changes Lie Ahead for the Hospital Industry and Beneficiaries

This week, our In Focus section reviews the policy changes that the Centers for Medicare & Medicaid Services (CMS) proposes to make in the Fiscal Year (FY) 2026 Medicare Hospital Inpatient Prospective Payment System (IPPS) and Long-Term Acute Care Hospital (LTCH) Proposed Rule (CMS-1833-P). The IPPS proposed rule, released April 11, 2025, includes several important policy changes that will alter hospital margins and change administrative procedures, beginning as soon as October 1, 2025.

Key Provisions of the FY 2026 Hospital IPPS and LTCH Proposed Rule

For FY 2026, CMS proposes to modify several hospital inpatient payment policies. We highlight and interpret six of these proposed policies that may be among the most impactful for Medicare beneficiaries, hospitals and health systems, payers, and manufacturers, as follows:

- Annual inpatient market basket update

- Labor share reduction

- Medicare Advantage (MA) data integration in measuring hospital readmissions

- New Technology Add-on Payment (NTAP) program growth

- Transforming Episode Accountability Model (TEAM) modifications

- Uncompensated care payment increase for disproportionate share hospitals (DSHs)

Annual Inpatient Market Basket Update

Proposed Rule: CMS’s FY 2026 Medicare IPPS Proposed Rule will increase payments to acute care hospitals overall by 2.4 percent from FY 2025, amounting to an estimated $4 billion increase in reimbursement. This update is based on a hospital market basket increase of 3.2 percent and a 0.8 percent reduction for total factor productivity.

HMA Analysis: CMS’s 2.4 percent increase results from the estimated rate of increase in the cost of a standard basket of hospital goods—the hospital market basket. For beneficiaries, this payment increase will lead to a slightly higher standard Medicare inpatient deductible and an increase in out-of-pocket costs. For hospitals and health systems, payers, and manufacturers, the proposed payment increase (2.4 percent) is consistent with economy-wide inflation over the past year (2.4 percent) and below the amount that MA plans will receive for 2026 (5 percent).[1], [2] Although the published payment update for FY 2026 is 2.4 percent, other policy changes result in the average change in inpatient payments totaling slightly more than 3 percent. We anticipate the proposed 2.4 percent increase will increase somewhat by the time CMS finalizes these rates later in the year.

Labor Share Reduction

Proposed Rule: CMS proposes to modify the hospital labor share used to reimburse hospitals for inpatient services. Using 2023 hospital cost report data CMS proposed a national labor‑related share of 66.0 percent, a decrease from the labor share of 67.6 percent.

HMA Analysis: Every five years, CMS recalculates the hospital market basket and the hospital labor share using updated cost data from the hospital cost reports. For FY 2026, CMS conducted its routine rebasing calculation using 2023 cost report data, replacing the 2018 cost data currently used. As a result, CMS calculated that the cost of labor accounts for a slightly smaller share of total hospital costs in 2023 than in 2018. The labor share is used within the IPPS to identify the proportion of payments that are affected by the hospital wage index in an effort to adjust payments for geographic variation in labor costs. The consequence of a lower hospital labor share is that a slightly smaller share of hospital inpatient payments will be adjusted by the hospital wage index. The subtle impact of this change is that hospitals with higher wage index values may experience reductions in payment. Further, this downward revision of the labor share signals that hospital wages, salaries, and employee benefits account for a smaller share of total costs in the post-pandemic environment. This change may come to a surprise to some, as hospital labor costs have been a subject of concern since the COVID-19 public health emergency.

Medicare Advantage Data Integration in Measuring Hospital Readmissions

Proposed Rule: CMS proposed to make several modifications to the Hospital Readmissions Reduction Program (HRRP), including:

- Refining all six readmission measures to add MA patient data

- Removing the COVID-19 patient denominator exclusion from measures

- Reducing the applicable period from three years to two

- Modifying the DRG payment ratios in the payment adjustment formula to include MA beneficiaries

- Clarifying that CMS has the discretion to grant an extension to hospitals under the extraordinary circumstances exception (ECE)

CMS also proposed to include MA data in other measures included in the Hospital Value-Based Purchasing (VBP) program and the Inpatient Quality Reporting (IQR) program.

HMA Analysis: The inclusion of MA data in the HRRP may have significant payment implications for many hospitals because it will alter their readmission rates in unanticipated ways, particularly if hospitals’ MA patients differ substantially from traditional Medicare beneficiaries. Importantly, the inclusion of MA data in the HRRP measures, and also within the VBP program and the IQR program, signals that CMS is moving toward broader integration of MA data into Medicare fee-for-service reimbursement systems.

New Technology Add-on Payment Program Growth

Proposed Rule: CMS proposed to continue NTAP status for 26 products because they continue to meet the newness criteria required under this program. In addition, within the proposed rule CMS discusses new NTAP applications for 43 additional products. Among these applications, 29 were submitted under the alternative pathways for breakthrough devices and qualified infectious disease products (QIDP).

HMA Analysis: The overall number of products with NTAPs is on par with other recent years, but the number of NTAP applications has blossomed in FY 2026 as the result of the alternative breakthrough application pathway. This alternative pathway allows breakthrough devices and certain antibiotic and antimicrobial drugs to apply for NTAP using an abbreviated application process.

Transforming Episode Accountability Model Modifications

Proposed Rule: CMS proposed several modifications to the forthcoming CMS Innovation Center TEAM framework. Among the various methodological modifications proposed to this mandatory payment model beginning January 1, 2026, CMS proposed to take the following actions:

- Limit the deferment period for certain hospitals

- Replace the Area Deprivation Index (ADI) with the Community Deprivation Index (CDI)

- Use a 180-day lookback period and Hierarchical Condition Categories (HCC) for risk adjustment

- Remove health equity and health-related social needs data reporting

- Expand use of the Skilled Nursing Facility (SNF) three-day rule waiver

HMA Analysis: The critical aspect of CMS’s TEAM provision is that the agency proposes to follow through with this Innovation Center model while cancelling other Innovation Center payment models in recent months. It also is noteworthy that the agency has proposed to remove the health equity data reporting requirements for TEAM in line with actions taken with many other CMS programs. Another proposal of note is the plan to expand the use of the waiver to circumvent the SNF three-day inpatient stay rule, which will allow hospitals to discharge patients more quickly to SNFs.

Uncompensated Care Payment Increase for Disproportionate Share Hospitals

Proposed Rule: CMS proposes to increase uncompensated care payments to DSHs by $1.5 billion in FY 2026.

HMA Analysis: CMS’s proposal will increase uncompensated care payments to hospitals by 26 percent. This increase is driven by CMS’s assumption that the rate of uninsured people will increase to 8.7 percent of the population in 2026 from 7.7 percent in 2025.

Stakeholder comments on the IPPS proposed rule are due no later than June 10, 2025.

Connect With Us

The Health Management Associates, Inc. (HMA), Medicare Practice Group monitors federal regulatory and legislative developments in the inpatient setting and assesses the impact on hospitals, life science companies, and other stakeholders. Our experts interpret and model hospital payment policies and assist clients in developing CMS comment letters and long-term strategic plans. Our team replicates CMS payment methodologies and model alternative policies using the most current Medicare fee-for-service and Medicare Advantage (100%) claims data. We also support clients with DRG reassignment requests, NTAP applications, and analyses of Innovation Center alternative payment models.

For more information about the proposed policies, please contact our expert below.

[1] U.S. Bureau of Labor Statistics. Table 1. Consumer Price Index for All Urban Consumers (CPI-U): U.S. City Average, by Expenditure Category. Modified April 10, 2025. Available at.

[2] Centers for Medicare & Medicaid Services. 2026 Medicare Advantage and Part D Rate Announcement. April 7, 2025.

Webinar Replay – Medicare Town Hall with HMA Experts

This webinar was held on April 30, 2025.

Whether you’re navigating Medicare Advantage policy changes, seeking actuarial insights, analyzing risk-based payment structures, or working to improve integration for Dual Eligibles and align D-SNPs, our team is here to provide actionable insights and answers. We had HMA professionals from across the country share their perspectives and help navigate the complexities of Medicare during this town hall style webinar.

Webinar Replay: PACE Development Best Practices for Policy Makers and Program Sponsors

This webinar was held on May 15, 2025.

Health Management Associates (HMA) conducted a multi-state study to examine the policy decisions influencing the operation and expansion of Programs of All-Inclusive Care for the Elderly (PACE). It explored different program structures, associated advantages and challenges, and strategies to enhance efficiency while meeting regulatory requirements.

This webinar summarized our research on 10 active PACE states (CA, FL, IL, KY, LA, MA, NJ, NY, OH, and WA) that have either implemented or expanded their PACE programs between 2020 and 2024. Using state survey responses and credible third-party, publicly available data, we showcased the outcomes of PACE program development through open and competitive RFP processes. We also outlined development timelines to demonstrate the effectiveness of each approach and highlight key insights gained during the discovery and research phase of the study.

Learning Objectives:

- Comparing the Open versus Competitive RFP approach

- Understanding state-level practices, challenges, and opportunities for improvement

- Review state profiles highlighting: Program development outcomes; Building PACE program capacity; Program development timelines; Fostering PACE growth

Amber ground ambulance dataset reflects complexity and challenges of the industry, highlights the need to improve and continue cost data collection

The Centers for Medicare & Medicaid Services (CMS) is on the cusp of possessing the data needed to make long anticipated changes to the Medicare fee-for-service (FFS) ground ambulance payment system. It has been more than two decades since CMS revised these payment rates through a negotiated rulemaking process that was exclusive of actual cost data or inflationary considerations. Since then, the cost structure of ground ambulance entities has changed. CMS is now using the Ground Ambulance Data Collection System (GADCS) to gather ambulance cost data, as required by Congress, to offer an improved understanding of the costs of delivering ground ambulance services. Given the potential of GADCS data to improve the adequacy of Medicare FFS reimbursement rates, the American Ambulance Association developed a similar data collection device, referred to as Amber, to test these data with its membership of ground ambulance entities. Amber offers a glimpse into the current challenges of the ground ambulance industry.[i]

Health Management Associates, Inc. (HMA) assessed the Amber dataset for response rates and data quality, along with responses containing calendar year 2022 financial data. Amber response rates were low, but sample volumes were on par with prior industry surveys conducted in the past by federal agencies. The Amber sample is representative of the industry’s wide variation in entity size and geographic service area. Amber data are reliable for calculating margins, but some aspects of these data also signal that ground ambulance entities, particularly smaller entities, may have had difficulty with variable definitions or the submission process. We observe that Amber would be improved by including information on uncompensated care and more details on medication supply costs.

The 2022 financial data from Amber suggest that Medicare FFS margins, at -6 percent, had declined since GAO’s 2010 assessment and that the share of costs associated with labor has increased. Amber data also suggest that the cost structure of smaller ground ambulance entities and rural and super-rural entities differs from that of larger and more urban entities. Margins for small and rural entities are lower.

Based on our assessment of the Amber dataset and its 2022 financial, we offer several recommendations to policymakers and stakeholders. These recommendations are intended to improve future cost collection efforts that may inform payment reforms to enhance the payment accuracy of the Medicare FFS payment system for ground ambulance services.

- Provide additional educational support to respondents to improve consistency of data reporting

- Streamline and modify data collection devices to adhere to industry trends and challenges

- Develop a standardized method for assigning ground ambulance entities to geographic service area for research purposes

- Collect data on ground ambulance uncompensated care and bad debt

- Collect payer level data for cases involving treatment without transport

- Collect targeted data on top 10 medications by cost to accurately reflect costs in payment rates

- CMS should consider collecting ground ambulance cost data on a semi-regular basis

- CMS should consider phasing in the use of GADCS data to ensure that the data reflect the diversity of ambulance entities and consistent reporting of key financial variables

[i] American Ambulance Association. Ambulance Cost Collection. 2023.

Medicaid Managed Care Enrollment Update: Q4 2024

Our second In Focus section reviews the most recent Medicaid enrollment trends in capitated risk-based managed care programs in 29 states.[1] Health Management Associates Information Services (HMAIS) collected and analyzed monthly Medicaid enrollment data from the fourth quarter (Q4) of 2024.

The data offer a timely overview of trends in Medicaid managed care enrollment and valuable insights into state-level and managed care organization (MCO)-specific enrollment patterns. This information allows state governments, their partners, and other organizations interested in Medicaid to track enrollment shifts. Understanding the underlying drivers of enrollment shifts is critical for shaping future Medicaid policies and adjusting program strategies amid a dynamic healthcare landscape.

Overview of the Data

The 29 states included in our review have released monthly Medicaid managed care enrollment data via a public website or in response to a public records request from Health Management Associates (HMA). This report reflects the most recent data posted or obtained. HMA has made the following observations related to the enrollment data (see Table 1):

- As of December 2024, across the 29 states tracked in this report, Medicaid managed care enrollment was 61.7 million, down by 3.6 million (-5.5%) year-over-year.

- Though most states experienced declines in enrollment, six states saw enrollment increases as of December 2024—double the number of states from the previous year.

Figure 1. Year-Over-Year Medicaid Managed Care Enrollment Percent Change in Select States, 2020−24

- Among the 22 expansion states included in this report, net Medicaid managed care enrollment has decreased by 2.1 million (-4%) to 49.5 million members at the end of Q4 2024, compared with the same period in 2023.[2]

- Among the seven states included in this report that had not expanded Medicaid as of December 2024, net Medicaid managed care enrollment decreased by 1.5 million, or 1 percent, to 12.3 million members at the end of Q4 2024 compared with to the same period in 2023.

Table 1. Monthly MCO Enrollment by State—October through December 2024

It is important to note the limitations of the data presented. First, not all states report the data at the same time during the month. Some of these figures reflect beginning of the month totals, whereas others reflect an end of the month snapshot. Second, in some cases the data are comprehensive in that they cover all state-sponsored health programs that offer managed care options; in other cases, the data reflect only a subset of the broader managed Medicaid population. This limitation complicates comparison of the data described above with figures reported by publicly traded Medicaid MCOs. Hence, the data in Table 1 should be viewed as a sampling of enrollment trends across these states rather than as a comprehensive comparison, which cannot be established based solely on publicly available monthly enrollment data.

HMAIS also compiles a more detailed quarterly Medicaid managed care enrollment report representing nearly 300 health plans in 41 states. The report provides by plan enrollment plus corporate ownership, program inclusion, and for-profit vs. not-for-profit status, with breakout tabs for publicly traded plans. Table 2 shows a sampling of plans and their national market share of Medicaid managed care beneficiaries based on a total of 66.3 million enrollees. These data too should be viewed as a broader representation of enrollment trends rather than as a comprehensive comparison.

Table 2. National Medicaid Managed Care Market Share by Number of Beneficiaries for Sample of Publicly Traded Plans, 2024

What to Watch

Enrollment in Medicaid MCOs has experienced significant fluctuations recently, influenced both by policy changes and economic factors. Since April 2023, Medicaid enrollment has been on a downward trajectory as states complete eligibility redeterminations after the end of the COVID-19 public health emergency. This trend, coupled with financial and political challenges, necessitates strategic planning for stakeholders to navigate the evolving Medicaid landscape effectively.

Potential changes that may affect enrollment and require scenario and readiness planning include:

- Federal requirement, or a new state option, to implement Medicaid work requirements for at least some categories of enrollees

- Changes to the federal financial match policy, which may cause some states to make different decisions about their Affordable Care Act expansion program for adults

- Modifications in requirements and expectations for more efficient eligibility processes to improve the accuracy of determinations and assignment to eligibility categories

Connect with Us

HMA is home to experts who know the Medicaid managed care landscape at the federal and state levels. The HMAIS subscription provides point-in-time and longitudinal Medicaid enrollment data, health plan financials, and additional actionable information about eligibility expansions, demonstration and waiver initiatives, as well as population- and service-specific information. HMAIS also includes a comprehensive public documents library containing Medicaid requests for proposals and responses, model contracts, scoring sheets, and protests.

For detail about the HMAIS enrollment report and subscription service, contact our experts below.

[1] Arizona, California, Florida, Georgia, Illinois, Indiana, Iowa, Kentucky, Louisiana, Maryland, Michigan, Minnesota, Mississippi, Missouri, Nevada, New Jersey, New Mexico, New York, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Tennessee, Texas, Virginia, Washington, West Virginia, Wisconsin.

[2] Health Management Associates, Inc. Medicaid Managed Care Enrollment Update—Q4 2023. HMA Weekly Roundup. April 17, 2024.

CMS Finalizes 2026 Payment and Policy Updates for Medicare Advantage and Part D

CMS approves average increase of 5.06 percent for MA plans while deferring major policy changes in MA and Part D programs

The Centers for Medicare & Medicaid Services (CMS) released the 2026 Medicare Advantage (MA) and Part D Rate Announcement on April 7, 2025, finalizing payment updates for calendar year (CY) 2026. This announcement came shortly after the release of the Contract Year 2026 MA, Part D, and PACE Policy and Technical Changes Final Rule, on April 4, 2025. Together, these updates mark the conclusion of CMS’s annual rulemaking cycle for Medicare Advantage, ahead of the June 2, 2025, deadline for 2026 MA plan bids.

Notably, because of the timing of the draft notices and proposed rule, Trump Administration officials ultimately had more input into policies omitted from the rate notice and final policy rule than on policies that were finalized. For example, the final rule is exclusive of proposals to expand coverage for anti-obesity medications, guardrails for artificial intelligence (AI), and new requirements related to utilization management and prior authorization procedures.

In his confirmation hearing, CMS Administrator Mehmet Oz, MD, cited Medicare Advantage prior authorization practices and health risk assessments that lead to upcoding as areas that deserve further consideration and scrutiny, raising the potential for future regulatory shifts and even legislative reform. With the possibility of Medicare, including MA, facing cuts as part of broader budget negotiations in Congress, the rate notice and policy rule offer program stability counterbalancing the political and fiscal pressures that may emerge this year.

CMS has sought to stabilize MA and Part D programs into 2026, and stakeholders can benefit from understanding the impact in markets for 2026 and the signals of potential regulatory changes to come. For more in-depth analysis and insights on the rate notice, look for our policy and actuarial experts’ brief due out next week.

The remainder of this In Focus article reviews CMS’s decisions on major payment and policy proposals in the Rate Announcement and Final Rule and examines key considerations for healthcare stakeholders.

Payment Impact on Medicare Advantage Organizations

In the CY 2026 Rate Announcement, CMS projects that federal payments to MA plans will increase by 5.06 percent from 2025 to 2026, which represents a $25 billion increase in expected payments to MA plans next year. According to CMS, this represents an increase of 2.83 percentage points compared with the CY 2026 Advance Notice that is largely attributable to an increase in the effective growth rate. The increase in the effective growth rate—increasing to 9.04 percent in the Rate Announcement from 5.93 percent in the Advance Notice—is primarily the result of the inclusion of additional data on Medicare fee-for-service (FFS) expenditures, including payment data through the fourth quarter of 2024.

The Rate Announcement estimates represent the average increase in payments to MA plans and actual payments will vary from plan to plan. Below, Table 1 provides CMS estimates of the impact of finalized payment changes on net MA plan payments.

MA Risk Adjustment Changes

As expected, CMS finalized the last year of the three-year phase-in of the MA risk adjustment model, which requires calculating 100 percent of the risk scores using only the 2024 CMS-HCC (Hierarchical Condition Category) model in 2026. CMS also addressed stakeholder concerns with the planned transition toward a risk adjustment model based on MA encounter data, as previewed in the CMS CY 2026 Advance Notice. CMS pledged to engage stakeholders in this model development process while continuing to evaluate the feasibility, transparency, and timing of a future transition to an encounter-based risk adjustment model.

CMS also finalized the MA coding pattern adjustment factor of 5.9 percent for CY 2026, which is the statutory minimum adjustment factor to account for differences in coding patterns between MA plans and providers under Medicare FFS Parts A and B.

Part D Risk Adjustment

For CY 2026, CMS finalized the revised 2026 RxHCC model with adjustments for maximum fair price drugs. Importantly, CMS also finalized using separate FFS normalization factors for MA-Prescription Drug (MA-PD) plans and Prescription Drug Plans (PDPs), making 2026 the second year CMS will vary normalization for these two markets. The calculation of the factors for CY 2026 is different, however, and will have substantially greater impact than the method used previously. It also will reduce Part D risk scores significantly for MA-PD plans while increasing scores for PDPs.

MA Star Ratings

CMS continues to solicit feedback from stakeholders on ways to simplify and refocus MA Star Ratings measures to focus more on clinical care, outcomes, and patient experience of care measures. Also included in the CY 2026 Rate Announcement are non-substantive measure specification updates and a list of measures included in the Part C and Part D improvement measures and categorical adjustment index for the 2026 Star Ratings.

Separately, in the policy and technical changes rule, CMS finalized new regulatory requirements designed to enhance MA beneficiary protections in an inpatient setting, provisions related to allowable special supplemental benefits for the chronically ill (SSBCI), and the care experience for dually eligible beneficiaries enrolled in MA special needs plans.

Enhancing MA Beneficiary Appeal Rights and Notification Requirements

CMS is finalizing provisions that limit the ability of MA plans to reopen and modify a previously approved inpatient hospital decision on the basis of information gathered after the approval. Under the final rule, MA plans will be able to reopen an approved hospital admission only due to error or fraud. In addition, CMS finalized several provisions to enhance beneficiary appeal rights and new reporting and notice requirements, including:

- Ensuring that MA appeals rules apply to adverse plan decisions, regardless of whether the decision was made before, during, or after the receipt of such services

- Codifying existing guidance that requires plans to give a provider notice of a coverage decision

- Ensuring enrollees have a right to appeal MA plan coverage denials that affect their ongoing source of treatment

Non-Allowable Special Supplemental Benefits for the Chronically Ill

The final rule establishes guardrails for SSBCI benefits by codifying a list of non-allowable examples (e.g., unhealthy food, alcohol, tobacco, life insurance). CMS did not finalize proposals that were designed to improve administration of supplemental benefits and enhance transparency of the availability of such benefits.

Improving Care Experience for Dual Eligibles

CMS finalized new requirements for dual eligible special needs plans (D-SNPS) that are applicable integrated plans (AIPs) as follows:

- D-SNPs will be required to have integrated member ID cards for their Medicare and Medicaid plans

- D-SNPs will be required to conduct an integrated health risk assessment for Medicare and Medicaid, rather than separate ones for each program.

These provisions affecting certain D-SNPS plans will be effective for the 2027 plan year.

Provisions Pertaining to the Medicare Part D Inflation Reduction Act

CMS is finalizing proposals to codify existing requirements related to key provisions of the Inflation Reduction Act, including no cost sharing for adult vaccines and capping monthly copayments for insulin at $35. In addition, CMS is codifying existing guidance related to the implementation of the Medicare Prescription Payment Plan, which is also part of the Inflation Reduction Act.

Key Proposals CMS Has Yet to Finalize

As noted earlier, CMS finalized a streamlined rule that excluded several regulatory changes identified in the November 2024 proposed rule. In addition to provisions related to coverage of anti-obesity medications, guardrails for AI, and mandatory analysis of the health equity impact of MA plans utilization management practices, the following proposals were not finalized. CMS notes that these proposals might be finalized in future rulemaking.

- Expanding Medicare Part D Medication Therapy Management (MTM) eligibility criteria

- Ensuring equitable access to behavioral health services by applying MA cost-sharing limits

- Enhancing the Medicare Plan Finder to include information on plan provider directories

- Promoting informed choice by enhancing CMS review of MA marketing and communication materials

- Enhancing rules on MA plans’ use of internal coverage criteria

Key Considerations

The policies finalized in the CY 2026 Rate Announcement are projected to increase average Part C payments to MA plans by 5.06 percent in CY 2026—a significant uptick from the payment updates originally proposed in the CY 2026 Advance Notice. Nonetheless, the final rate increase will have varying effects across MA plans, with some experiencing larger or smaller impacts in CY 2026. MA plans should assess these outcomes as they prepare their bid submissions for 2026.

According to the CY 2026 Rate Announcement, CMS expects that the 5.06 percent increase will provide continued stability for the MA program and its beneficiaries while ensuring accurate and appropriate payments to Medicare Advantage organizations.

In the CY 2026 MA and Part D Final Rule, CMS adopted a significantly scaled-back final rule, which omitted some of the more far-reaching proposals for MA and Part D that were originally proposed in November 2024. CMS, however, could potentially revisit and finalize some of these proposals in future rulemaking. Moreover, new regulatory requirements that enhance enrollee protections in inpatient care settings and improving the care experience for dual eligibles signal CMS’s continued interest in improving program oversight and enhancing consumer protections for MA beneficiaries.

Connect With Us

MA stakeholders need to undertake scenario planning and be prepared to adapt to a rapidly evolving federal policy environment. From modeling and impact assessments of specific policy changes to strategy development and implementation, HMA is home to experts with diverse skill sets. Our team can help stakeholders assess and prepare for potential changes to prior authorization, looking holistically at their organization’s operations, patient care models, and reimbursement strategies. Our team also provides detailed modeling and assessments to ensure health plans are prepared for changes in risk adjustment and coding policies, supplemental benefits, and other key issues affecting capitation payment, bids, and care delivery models.

For details about the finalized payment and policy rules contact our featured experts below.

HHS Begins Reorganization: Actions Focus on Efficiency, Establishment of Administration for a Healthy America

On March 27, 2025, the US Department of Health and Human Services (HHS) Secretary Robert F. Kennedy, Jr. announced significant changes in the department with respect to staffing and organizational restructuring. This reorganization is consistent with President Trump’s February 11, 2025, Executive Order (EO) 14210, “Implementing the President’s Department of Government Efficiency Workforce Optimization Initiative.”

HHS is moving rapidly to implement its plans. On April 1, 2025, HHS initiated actions to reduce the federal workforce across the agencies and remake the department. In addition, the Senate is expected to vote on a budget resolution this week, which could have significant impacts on federal healthcare spending, including for the Medicaid and Medicare programs.

In the coming weeks and months, HHS intends to make additional announcements about how the department will be restructured. It will be critical that healthcare organizations and stakeholders track these developments closely. Organizations seeking to participate in the development of new federal policies and initiatives must know which offices within HHS will maintain authority over key policy areas. Further, to adapt to changes in funding and policies, it is vital that healthcare leaders remain informed.

Because many changes have already begun, the remainder of this article explains what is known to date about the HHS restructuring and other developments and actions relevant to providers, life sciences firms, insurers, safety net clinics, state and local agencies, and other interested stakeholders. This information can help stakeholders consider how best to proceed.

The Reorganization Plan

EO 14210 required agencies to develop reorganization plans and submit them to the Director of the Office of Management and Budget within 30 days and to “promptly undertake preparations to initiate large-scale reductions in force.” The broader HHS reorganization plan seeks to implement a new departmental focus on “ending America’s epidemic of chronic illness by focusing on safe, wholesome food, clean water, and the elimination of environmental toxins.”

The reorganization calls for the following:

- Consolidating the 28 HHS divisions into 15

- Reducing the HHS regional offices from 10 to five

- Centralizing the human resources, information technology, procurement, external affairs, and policy functions of the department

- Reducing the full-time staff at HHS by 10,000

When combined with other efforts, including early retirement and pre-reduction in force (RIF), HHS’s staffing levels of 82,000 full-time will be reduced to 62,000. The announcement listed specific workforce reduction plans for the Food and Drug Administration (FDA), the Centers for Disease Control and Prevention (CDC), the National Institutes of Health, and the Centers for Medicare & Medicaid Services (CMS).

Following the March 27 announcement, additional details regarding the restructuring have continued to emerge, including:

- The Biomedical Advanced Research and Development Authority (BARDA) reportedly will be combined with Advanced Research Projects Agency for Health (ARPA-H) under a new Office of Healthy Futures.

- The Administration for Strategic Preparedness and Response (ASPR) will be reorganized as a part of CDC.

- Programs currently under the Administration for Community Living (ACL) are slated to be reassigned to other agencies; for example, programs that support older adults and people with disabilities will move to the Administration for Children and Families (ACF), Assistant Secretary for Planning and Evaluation (ASPE), and CMS.

HHS Plans for New Agencies that Mirror Policy Priorities

The reorganization includes the establishment of a new Administration for a Healthy America (AHA), which will combine the following offices and agencies:

- Office of the Assistant Secretary for Health, which includes the Office of the Surgeon General, the Office of Women’s Health, and several programs focused on health promotion, chronic disease prevention, and vaccines

- Health Resources and Services Administration (HRSA)

- Substance Abuse and Mental Health Services Administration (SAMHSA)

- Agency for Toxic Substances and Disease Registry (ATSDR)

- National Institute for Occupational Safety and Health (NIOSH)

According to HHS, the changes are intended to “improve coordination of health resources for low-income Americans and will focus on areas including, Primary Care, Maternal and Child Health, Mental Health, Environmental Health, HIV/AIDS, and Workforce development.” The department also noted that transfer of SAMHSA to the new AHA will “break down artificial divisions between similar programs” and improve operational efficiency.

HHS also intends to establish a new Assistant Secretary for Enforcement position, which will be responsible for leading efforts to address waste, fraud, and abuse at the Departmental Appeals Board, Office of Medicare Hearings and Appeal, and the Office for Civil Rights.

HHS will merge the ASPE and Agency for Healthcare Research and Quality (AHRQ) to establish a new Office of Strategy. The new office will support research “that informs the Secretary’s policies and evaluates the effectiveness of federal health programs.” This office will also include some of the “critical programs that support older adults and people with disabilities” that are currently within the Administration for Community Living.

Developments on Workforce Reduction Plans

On April 1, 2025, HHS began issuing formal termination notices to a significant number of federal employees across several agencies, including the FDA, SAMHSA, and CDC. The workforce actions reportedly include a full dissolution of some offices, for example, SAMHSA’s Office of the Director for Centers for Mental Health Services, Office of Behavioral Health Equity, The Policy Lab, among others, and CMS’s Medicare Medicaid Coordination Office.

What’s Next

In the coming weeks HHS will put in place a structure for the new AHA and other planned new entities. Many questions remain about the impact on specific agencies and authorities as well as reassignment of responsibilities for programs and functions that were carried about by affected federal employees and offices.

Congressional committees are seeking additional information about the HHS restructuring. The US Senate Committee on Health, Education, Labor, and Pensions (HELP) requested that Secretary Kennedy testify at a hearing on April 10, 2025, to discuss the proposed reorganization plan. Providers, health centers, life sciences firms, insurers, health systems, state and local agencies and other healthcare stakeholders and partners should take steps to work through challenges and avail themselves of opportunities to strengthen healthcare systems and improve health. Examples include:

- Identify the HHS agencies and offices that are now responsible for policies and procedures that impact your business.

- Establish a plan for tracking developments—including litigation—and processes to brief key organizational leaders and act on information, when needed. Healthcare providers, insurers, community groups, and state and local governments will benefit from information as it becomes available regarding changes to agencies and their portfolios and decision makers for policies governing Medicare, Medicaid, child-specific programs, aging and disability programs, mental health and substance use programs, among many others.

- Immediately assess current federal discretionary funding and reimbursement policies that may be at risk for your organization, your key partners, and collaborators. Consider potential impact of the policy changes that Congress is separately negotiating, which would significantly affect Medicare and Medicaid. Identify changes that may minimize risk for your organization and position it to engage in new initiatives.

- Familiarize your organization with federal oversight and enforcement priorities and incorporate flexibility into compliance plans. Identify opportunities to mitigate vulnerabilities going forward.

- Engage now—with your community, your peers, and other experts—to identify opportunities for improvement and plan to build out the strategy, infrastructure and funding to support this work. Think creatively, act decisively.

Connect with Us

Health Management Associates, Inc., experts know the federal landscape and have an intimate knowledge of the dynamics in states and communities. Our policy team is working with clients to help them understand what is happening within HHS and Congress that is ushering in significant policy and funding changes. Our teams are advising stakeholders on the implications for Medicare, Medicaid, and other public programs; strategies to advance their objectives in this new environment; and working with healthcare organizations and state and local government to understand immediate impacts on local financing.

For details about these federal level developments contact one of our featured federal policy experts listed below.

What to Watch: Medicare Payment Rules

Medicare stakeholders are awaiting the imminent release of the Centers for Medicare & Medicaid Services (CMS) final Medicare Advantage and Part D rate notice and technical updates, as well as a final policy rule that establishes a significantly new direction for Medicare Advantage (MA) stakeholders. These final rules typically are released in April of each year.

In addition, the agency kicks off the annual cycle of payment rules for traditional fee-for-service Medicare, including the first wave of proposed rules that typically are released in April for the forthcoming payment year. These proposed rules for 2026 pertain to the following: Hospital Inpatient Prospective Payment System for Acute Care Hospitals, the Inpatient Rehabilitation Facility Payment System, the Home Health Payment System, and the Inpatient Psychiatric Facility Payment System. A second wave of 2026 proposed rules are typically released in July, including the Medicare Physician Fee Schedule and the Hospital Outpatient Prospective Payment System.

The MA rules and the first wave of Medicare Part A and Part B rules are highly anticipated regulations and now under review at the Office of Management and Budget. These rules are expected to be released in the coming days and weeks.

Why These Rules Matter

The rules set the rates for MA and reimbursement for a significant number of healthcare providers and facilities that serve Medicare beneficiaries. The rules also contain important information about CMS’s quality reporting programs and bonus payments and other changes required for Medicare stakeholders to ensure compliance.

What’s Different About 2025 Proposals

In the first year of a new presidential administration, CMS leaders have a limited window to include their policy priorities in the MA and Part D Final Rate Notice. CMS may, however, decline to finalize some or all of the prior administration’s proposals. Key issues that Health Management Associates (HMA), experts are watching for in the final rules include:

- Whether CMS chooses to delay or not finalize significant policy changes proposed by the Biden Administration, including new requirements and guardrails around the use of prior authorization

- Potential finalization of improvements to the Medicare plan finder

- Direction on oversight of MA plan marketing activities

- CMS decision and response to the proposal to expand coverage of anti-obesity medications under Medicare Part D and Medicaid

Stakeholders can access HMA’s review of the contract year (CY) 2026 MA and Part D proposed rule and key considerations and our review of the 2026 Advance Notice for the Medicare Advantage and Medicare Part D programs.

Similarly, in the first year of a presidential transition, CMS has a narrower opportunity to shape Medicare’s first set of proposed payment and policy rules. The agency may, however, begin to signal important policy direction on a global level and technical issues that can have an impact on Medicare stakeholders. HMA experts are watching in particular for requests for information and other signals of CMS’s Medicare priorities, including reforms in quality reporting, value-based contracting, pricing and contract transparency, among others.

Connect with Us

HMA’s expert consultants provide the advanced policy, tailored analysis, and operational skills you need to navigate today’s rapidly evolving regulatory landscape and to support implementation of final policies. Don’t let the uncertainty of future policies derail your strategic plans or burden your teams.

For details about the forthcoming Medicare Advantage and traditional Medicare regulations, contact one of our featured experts below.

Navigating Uncertainty in Medicare and other Federal Health Programs

As we approach Medicare’s 60th Anniversary this July, the program again finds itself at a critical crossroads, facing demands for higher quality care, expanded access to transformative treatments, and streamlined patient access to their medical information. Decision makers also must integrate digital tools into clinical models, address mounting scrutiny of costs, and ensure accountability for outcomes influenced by social determinants of health.

This period of transition at the Federal level is bringing new scrutiny and pressure for efficiency. With more than 68 million beneficiaries, nearly half of whom are enrolled in Medicare Advantage, the Medicare program is continually evolving to respond to shifting policies and priorities. Organizations that stay ahead of policy changes will be best positioned for success and drive meaningful improvements for Medicare beneficiaries.

When you work with HMA’s federal policy experts, you get access to former CMS officials and plan executives, payment system and coding experts, and policy analysts to support your efforts. HMA’s Medicare team includes experts specializing in Medicare Advantage, dual eligibles, Medicare stars, value-based care, rural health, PACE, actuarial support, and data and quality. We draw on the resources of experts from our HMA companies to provide comprehensive and end-to-end solutions. Read some of our insights in the links below.

Here’s how HMA is helping clients navigate this dynamic landscape:

- Our policy team is working with clients to understand what is happening right now in Congress and in the US Department of Health and Human Services that will usher in significant policy and funding changes. Our teams are advising stakeholders on the short- and long-term implications, strategies to advance their objectives in this new environment, and working with states to understand immediate impacts on local financing.

- Our clinicians are working closely with insurers, providers, and health systems to strengthen models of care that address complex conditions, behavioral health issues, long-term services and supports and unique needs of special Medicare populations.

- Our actuaries are conducting financial modeling and analysis to forecast costs, revenues, and potential outcomes to help navigate financial uncertainties in Medicare Advantage bids, Medicare payment models, and emerging environmental and regulatory issues, including digital quality measure collection, increased focused on dual integration, supplemental benefits, and drug price negotiations.

- Our digital quality experts are working with healthcare organizations to prepare for rapid changes that digital health quality measurement will bring to reimbursement models. Our teams are advising on the influx of newly accessible clinical data to ensure it is properly validated and interpreted and working with insurers and providers to develop strategies allowing them to be more agile in contract negotiations.

To talk to an expert to help support and improve your Medicare programs, contact Greg Gierer with the HMA DC office ( [email protected]) or Josh Trent with the Leavitt Partners DC office ([email protected]).

For more cutting-edge information check out some of our recent insights:

Policy & Regulatory Strategies: Legislative, regulatory, reimbursement, and budget analysis from experienced former staffers from CMS and various legislative committees. The HMA policy team includes past HHS officials like Amy Bassano and Monica Johnson, as well as the team at Leavitt Partners.

- Webinar Replay — Legislative Reconciliation in a New Era: Understanding Its Role and Impact in the 119th Congress

- Podcast — Has Medicare’s Drug Policy Struck the Right Balance Between Access and Cost?

- Webinar Replay — 2024 Political Checkpoint

- Webinar Replay — The 2024 Election: What It Could Mean for Health Policy

- Report — On Rare Disease Day, HMA releases new report analyzing federal spending on Orphan Drugs

Actuarial & Financial Analytics: Leading actuaries with deep MA experience and robust tools to support innovative benefit and pricing strategies. Encounter data audits to improve risk scores. The HMA Actuarial team includes Wakely Consulting Group and Cirdan Health Systems and Consulting.

- PACE Plans and The Changing Risk Environment

- Webinar Replay — 2025 Medicare Advantage Bids Are Over. Now What?

- Project Spotlight — CMS Encounter Data Quality Review for an I-SNP Plan

Communications & Engagement: Creative campaigns to inform, persuade, and engage providers and payers. The HMA team includes 720 Strategies and Lovell Communications.

- Web campaign — American Association of Nurse Practitioners

- Website — Five Paid Digital Tactics You Need for Advocacy

Strategy & Transformation: Strategy & analytic fundamentals informed by variety of experts in Medicare, health insurance, care delivery for older and vulnerable populations, and value-based payment and delivery innovations.

- Podcast — Can data shape the future of Medicare’s value proposition?[TM6]

- Using Virtual Research Data Center (VRDC) Data to Answer Big Questions

- Report — Analyzing the Expanded Landscape of Value-Based Entities: Implications and Opportunities of Enablers for the CMS Innovation Center and the Broader Value Movement

Operations & Implementation: Clinical and administrative operations building care models, implementing value-based payment incentives, technology, and compliance. The HMA Managed Care team is led by Holly Michaels Fisher.

Quality Outcomes & Research: Integrated approach to STARS ratings, building digital quality management tools and strategies for compliance and accreditation. The HMA team includes Caprice Knapp and Sarah Scholle.

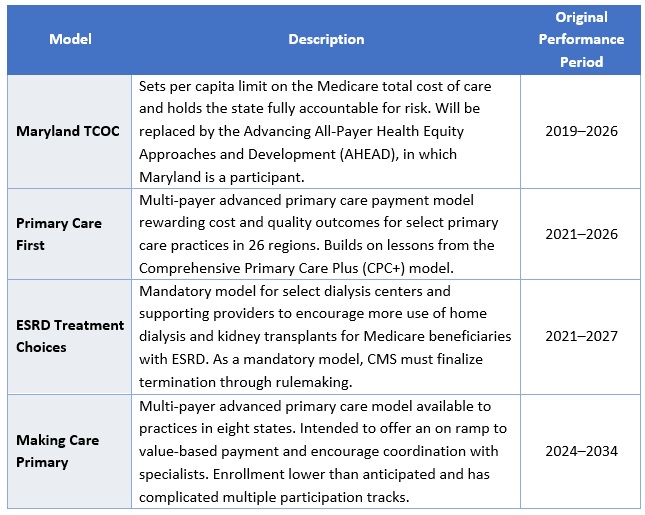

CMS Shakes Up the Innovation Center Model Landscape: What Comes Next?

This week, our In Focus section focuses on a March 12, 2025, announcement from the Centers for Medicare & Medicaid Services (CMS) regarding CMS Innovation Center programs under the new Administration. After reviewing the Innovation Center’s model portfolio, CMS has elected to discontinue four models ahead of their original end dates: Maryland Total Cost of Care (TCOC), Primary Care First (PCF), End-Stage Renal Disease (ESRD) Treatment Choices (ETC), and Making Care Primary (MCP). The agency also intends to downsize the Integrated Care for Kids Model (InCK) and forgo the launch of two drug pricing initiatives. According to the announcement, CMS appears to be moving forward with other Innovation Center models, but signaled upcoming modifications to models to align with Administration priorities as well as new model announcements.

The following is a discussion of CMS’s announcement and what it may signal about the agency’s commitment to value-based care, key takeaways regarding the four terminated models, and how stakeholders should be preparing to engage with the Innovation Center on current or future models while we await additional details.

CMS’s Strategic Decision

As part of CMS’s recent announcement about the model terminations, the agency reaffirmed its support for testing models that reduce program spending while maintaining or improving quality of care. Furthermore, the Innovation Center “plans to announce a new strategy based on guiding principles to make Americans healthier by preventing disease through evidence-based practices, empowering people with information to make better decisions, and driving choice and competition.” These statements should be seen as a commitment to using the Innovation Center to test new approaches to delivering care but with an expectation that the models will need to demonstrate significant cost and quality improvements as outlined in its statutory authority. According to CMS, the cancellation of these models is projected to save an estimated $750 million.

Because CMS said it may modify additional models in the future, it is reasonable to expect those changes will focus on achieving a higher level of savings or to see savings earlier in the demonstration, as well as aligning model design with the priorities of this Administration. The potential modifications could have an impact on the number of model participants, length of model testing, and financial arrangements, especially with regard to risk and quality improvement approaches.

Models Ending

CMS Innovation Center models are time-limited pilots meant to help the agency test which types of interventions lead to cost savings and improved quality and, if successful, can be scaled on a nationwide basis. These models are evaluated regularly, and CMS has the authority to modify or terminate models if they fall short of the statutory criteria.

The four models the agency plans to terminate are ending for various reasons (e.g., underwhelming performance, forthcoming replacement by successor model, etc.) and, as stated above, the decision should not be seen as a retreat from value-based care, but rather as a signal regarding Administration priorities for Innovation Center models. For example, despite terminating PCF and MCP prior to their original end dates, CMS reaffirmed its support for primary care as a “foundational component of the Center’s strategy” and that future primary care payment reforms will focus on approaches that produce savings. CMS also noted that ending these models early offers an opportunity to move beneficiaries into more permanent programs, such as the Medicare Shared Savings Program (MSSP)—CMS’ flagship accountable care initiative—even going so far as to direct readers to the MSSP’s calendar year 2026 application.

CMS plans to advise current model participants of other options for advanced primary care payment before the models conclude by December 31, 2025. Table 1 presents information on the models scheduled for early termination.

Table 1: Models Ending by December 31, 2025

In addition, the agency is considering options to reduce the size of the InCK model and will no longer pursue the Medicare Two Dollar Drug List and Accelerating Clinical Evidence models. The latter two initiatives were included in a Biden Executive Order on drug pricing and were not implemented. Notably, CMS did not end another drug pricing Innovation Center model, Cell and Gene Therapy Access (CGT) Model.

Innovation Center’s New Strategic Plan

CMS also announced that it will soon release its new vision for the Innovation Center, based on principles designed to improve Americans’ health through evidence-based practices, empower individuals with decision-making information, and drive competition.

This vision will set the direction for future value-based care initiatives and reflect the leadership changes within CMS, including the anticipated confirmation of Mehmet Oz, MD, as CMS Administrator and the appointment of Abe Sutton, as the new Director of the Innovation Center. Mr. Sutton’s experience with value-based care—especially during his time as an advisor to then Department of Health and Services Secretary Alex Azar under the first Trump Administration and his subsequent private sector leadership of value-based companies—positions him to play a key role in shaping CMS’s future efforts.

Stakeholder Considerations

Stakeholders have several critical operational decisions and strategic considerations to address, including:

- Transition Support. Participants in the models scheduled to end must assess their options for sustaining certain components of the payment models without Innovation Center support. This effort will require strategic, operational, and financial analyses to make informed decisions.

- Evaluation of Other Programs. While the Innovation Center has signaled its intentions of announcing new models, participants should not wait to evaluate options. The Administration plans to prioritize permanent payment programs and will continue to support the MSSP as CMS’s permanent model for accountable care organizations (ACOs). Stakeholders interested in participating in the MSSP in 2026 must act quickly to assess their organizational readiness, conduct financial modeling of their potential benchmark and performance, evaluate potential partners, and prepare for the application process. Both existing and new ACOs should be exploring their strategies and infrastructures to optimize performance.

- Adapting to Changes in Existing Models. While CMS discontinued select models, it is likely the agency will make additional changes to the Center’s continuing models. These revisions likely will reflect President Trump’s executive actions and policy priorities. With the increased focus on cost savings, CMS may choose to spend fewer resources on model implementation, including participant support and model engagement.

- Policy and Market Intelligence. Monitoring the dynamic federal policy landscape and seeking strategic advisory support can help stakeholders navigate and inform potential future federal and state alternative payment model opportunities. Stakeholders should expect that existing and potential new models may have stricter requirements and higher expectations for financial risk. Providers, states, insurers, and other interested stakeholders should monitor public and private sector developments to understand the landscape and evolving opportunities.

Connect with Us

Health Management Associates, Inc. (HMA), is home to alternative payment model experts that can assist stakeholders in responding to changes in Innovation Center models and the agency’s approaches and to help prepare for participation in future model opportunities. Additionally, HMA produces a weekly briefing focused on public and private sector VBP-related news. To learn more about how HMA can support your organization’s federal engagement and innovation strategy, contact our experts below.