This week, our In Focus reviews the New Mexico Medicaid managed care request for proposals (RFP), released on September 30, 2022, by the New Mexico Human Services Department (HSD). The state will transition to a new program called Turquoise Care in 2024, which will build upon the current Centennial Care 2.0 program through a new Section 1115 waiver demonstration. Managed care organizations (MCOs) will provide physical health, behavioral health, and long-term care (LTC) services to approximately 800,000 Medicaid managed care members.

RFP

New Mexico plans to award Turquoise Care contracts to three MCOs. One of the selected MCOs will also be awarded a specialized foster care plan contract to provide services to Children in State Custody (CISC) on a statewide basis. CISC will be mandatorily enrolled and Native American CISC members will have the option to voluntarily enroll.

Turquoise Care will introduce new practices aimed at improving quality based on population health outcomes. The program will focus on three goals:

- Goal 1: Build a New Mexico health care delivery system where every Medicaid member has a dedicated health care team that is accessible for both preventive and emergency care that supports the whole person – their physical, behavioral, and social drivers of health.

- Goal 2: Strengthen the New Mexico health care delivery system through the expansion and implementation of innovative payment reforms and value-based initiatives.

- Goal 3: Identify groups that have been historically and intentionally disenfranchised and address health disparities through strategic program changes to enable an equitable chance at living healthy lives. The target populations will be:

- Prenatal, postpartum, and members parenting children, including children in state custody

- Seniors and members with long-term services and supports (LTSS) needs

- Members with behavioral health conditions

- Native American members

- Justice-involved individuals

Other changes for Turquoise Care include:

- 90 percent Medical Loss Ratio (MLR) aimed at improving quality of care

- Expanded MCO reporting and monetary penalties for non-compliance

- Minimum reimbursement rate for contract providers at or above the state plan approved fee schedule

- More stringent provider network requirements

- A single centralized vendor to process applications

- Enhanced MCO staffing requirements, including qualifications, staffing levels, and training

- Focus on social determinants of health

New Mexico will submit the Section 1115 demonstration waiver for Turquoise Health to the Centers for Medicare & Medicaid Services (CMS) for approval by December 2022. HSD will update the model contract to reflect the requirements related to the waiver renewal upon its approval.

During this procurement, the state will also be developing and implementing a new Medicaid Management Information System (MMIS).

Eligibility

Approximately 83 percent of the Medicaid population is in managed care.

Populations exempt from mandatory managed care enrollment are:

- Native American members not in need of LTC

- Individuals with Intellectual Disabilities (ICF-IID) in Intermediate Care Facilities

- Individuals enrolled in Qualified Medicare Beneficiary (QMB), Specified Low-Income Medicare Beneficiary (SLIMB), or Qualified Individuals program

- Individuals covered only under the Medicaid Family Planning program

- Individuals enrolled in the Program of All-Inclusive Care for the Elderly (PACE)

- Individuals covered pursuant to Emergency Medical Services for Non-Citizens (EMSNC)

Members in the Developmental Disabilities 1915(c) Waiver and in the Medically Fragile 1915(c) Waiver will continue to receive home and community-based services (HCBS) through that waiver but are required to enroll with an MCO for all non-HCBS.

Timeline

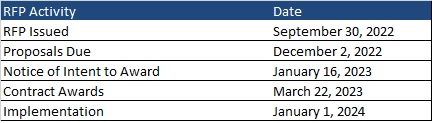

Proposals are due December 2, 2022. Contracts will run from January 1, 2024, through December 31, 2026, with optional one-year renewals, not to exceed eight years total.

Current Market

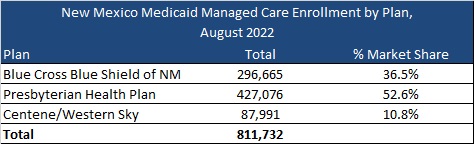

New Mexico had 811,732 Medicaid managed care as of August 2022, served by Blue Cross Blue Shield of New Mexico, Presbyterian Health Plan, and Centene/Western Sky. The state also had an additional 163,361 fee-for-service members.

Evaluation

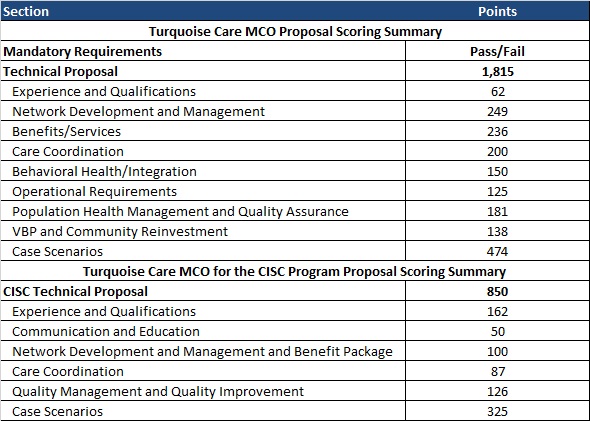

The evaluation process will consist of three phases: review of mandatory requirements, review and scoring of the technical proposals, and review and scoring of the CISC technical proposals.